ssuaphoto

Since my preliminary bullish write-up on Crestwood Fairness (NYSE:CEQP) again in mid-February, the inventory hasn’t executed a lot of something. Let’s take a better take a look at what’s been happening with the title.

Q1 Outcomes

CEQP reported its Q1 outcomes again in early Might. The midstream operator noticed an 11% enhance in adjusted EBITDA to $192.6 million from $172.8 million a 12 months earlier.

Its distributable money stream for the quarter got here in at $103.6 million. It paid out a quarterly distribution of 65.5 cents, leading to a protection ratio of 1.5x.

Free money stream was $45.7 million after it spent $57.9 million on development Capex within the quarter. FCF after distribution was an outflow of -$23.3 million.

The corporate ended the quarter with 4.2x leverage, or 4.0x after the sale of its 50% stake in Tres Palacios to Brookfield Infrastructure for $178 million.

Taking a look at its segments, Gathering and Processing North recorded EBITDA of $132.8 million versus $133.3 million a 12 months in the past. The corporate noticed a 1% enhance in crude gathering on its techniques. Nevertheless, pure fuel gathering volumes fell -7%, pure fuel processing quantity slipped -8%, and produced water gathering volumes edged -1% decrease. Powder River Basin pure fuel collect volumes fell -2%, whereas processing volumes have been 1% decrease.

On its Q1 name, CEO Robert Phillips mentioned:

“Within the Williston. We’re seeing the Arrow system slowly catch up the final 12 months’s volumes as we count on to attach greater than double the brand new wells in 2023 than we linked final 12 months. Our key producers, Devon, Exxon and Enerplus are sustaining lively new drilling or DUC completion packages, and so they have numerous work-over rigs coming again within the subject, bringing weather-related shut-in manufacturing again on-line. So lots of exercise round Arrow. On the Tough Rider system, Chord is spot on their 2023 growth schedule, and we simply positioned the essential metropolis of Williston 3-product gathering venture in service final week and that is crucial infrastructure to assist Chord’s 2023 and ’24 drilling program within the Western acreage devoted to us. And let me lastly say that our Williston operations crew continues to do a fantastic job in decreasing working prices, persevering with to seek out integration synergies and mitigating winter climate disruptions that we have skilled within the fourth quarter and the primary quarter of this 12 months.”

Gathering & Processing South EBITDA climbed 50% 12 months over 12 months to $41.0 million from $27.4 million a 12 months in the past. Pure fuel gathering and pure fuel processing volumes elevated surged by 111% and 244%, respectively, because of the acquisition of Sendero Midstream and important quantity development on its Willow Lake system. Crude volumes rose 11%, whereas produced water volumes climbed 36%.

CEQP Storage & Logistics segments noticed its EBITDA climb 55% to $32.8 million from $21.2 million a 12 months earlier. The section benefited from elevated demand as a result of winter climate within the Midwest and East Coast.

One of many larger dangers I talked about when first taking a look at CEQP was its ties to the Bakken, and the extreme winters the realm typically sees. This previous winter was notably harsh, which disrupted drilling and properly connections within the basin. Whereas E&Ps will ultimately meet up with their drilling plans, and plenty of want to join nearly all of their wells in Q2 and Q3, this does have a stream via impression relating to volumes.

Oil wells decline, and the most important declines come from new wells. CEQP and its producer clients want a sure variety of new wells to return on-line annually simply to keep up volumes, then something above that’s development. Whereas the long-term attractiveness of CEQP’s place is unchanged, the shortage of quantity development within the Bakken shouldn’t be stunning given the previous winter climate.

CEQP’s Permian property, in the meantime, carried out properly, and its logistics unit took benefit of some arbitrage alternatives from the climate within the quarter.

Outlook

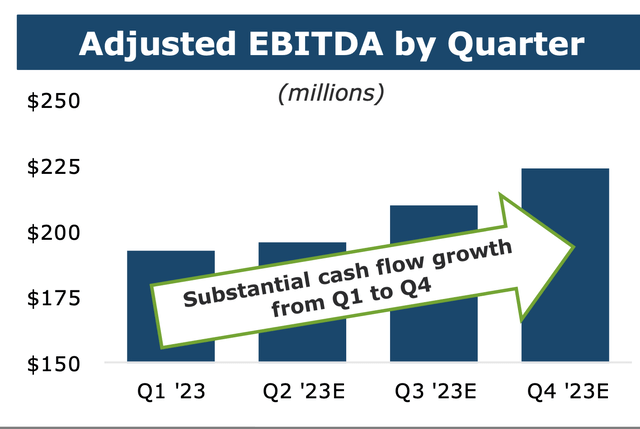

For 2023, CEQP is searching for adjusted EBITDA of between $780-860 million. That’s an 8% year-over-year enhance on the midpoint.

Firm Presentation

DCF is projected to return in at between $430-510 million. The corporate expects to spend between $135-155 million on development Capex and $25-30 million on upkeep Capex.

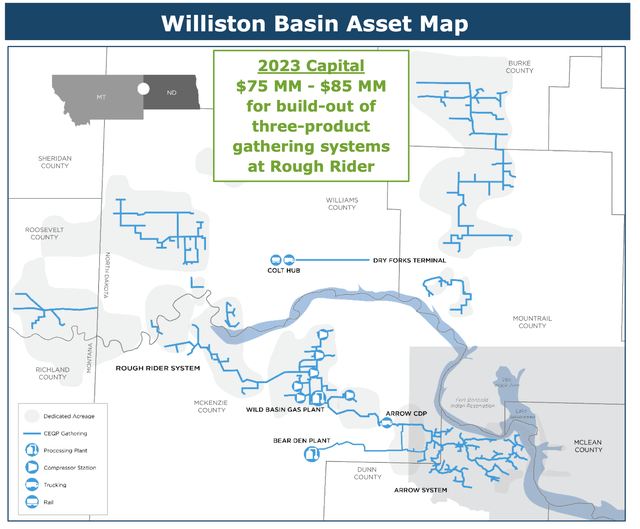

Half of its development Capex is centered on the western growth of its Tough Rider system, together with some incremental expansions on its Arrow system. CEQP is projecting between 115-125 properly connects this 12 months for its Bakken property.

Firm Presentation

Within the PRB, the corporate mentioned it has been in talks with Continental to assist their drilling within the space. The corporate notes that it has extra gathering, compression, and processing capability on the system.

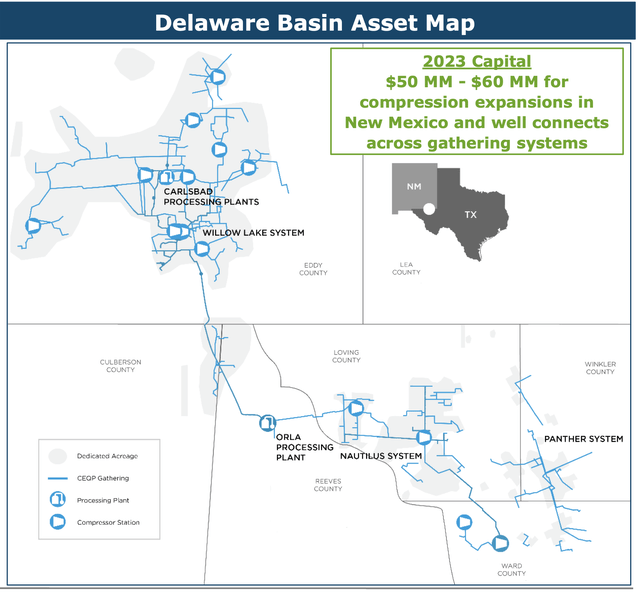

About 40% of its Capex will go in direction of the Delaware, with a concentrate on properly connects, system expansions and compression additions in New Mexico. It expects 120-130 properly connects for the 12 months.

Firm Presentation

FCF after distributions is forecast to be between $10-90 million, with year-end leverage of between 3.7-4.1x. It expects its distribution to stay flat this 12 months at $2.62, with a protection ratio of between 1.6-1.8x.

CEQP’s 2023 outlook remained unchanged, and with producers like Chord (CHRD) trying to do the majority of their Bakken completions in Q2 and Q3, the corporate ought to have a reasonably clear sight. The corporate ought to see some good development within the basin after it completes its growth to assist CHRD, whereas the PRB additionally affords some upside as Continental seems to develop within the space. The Permian, in the meantime, stays the premier oil basin within the U.S., and all gamers ought to profit when the basin sees elevated fuel takeaway come on-line later this 12 months.

Valuation

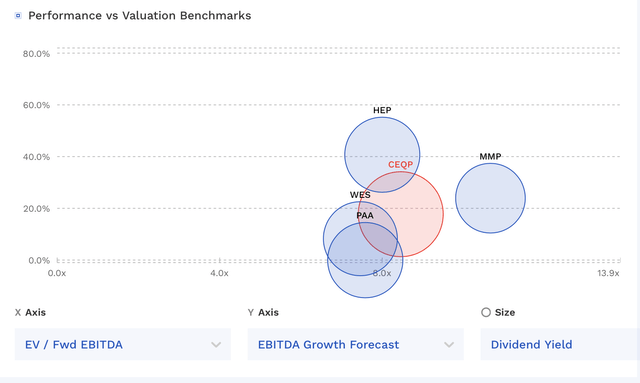

CEQP trades at 8.4x the 2023 EBITDA consensus of $823.1 million. For 2024, it trades at 7.8x the 2024 EBITDA consensus of $883.1 million.

It trades at about 5.7x P/DCF of $470 million, and has a 2023 FCF yield of over 12%.

The inventory at present yields 10.4% with a strong 1.7x protection ratio projected for the 12 months.

The inventory trades at an analogous valuation to different midstream corporations, though it has one of many highest yields.

CEQP Valuation Vs Friends (FinBox)

Conclusion

There most likely isn’t a inventory I do know higher than CEQP. At my previous agency, CEQP was twice the top-contributing place for the fund, and I used to be the lead analyst on the corporate. Once we initially took a place, it was one of the vital reviled shares on the market, and nobody wished to the touch it’s going to a 10-foot ballot. I later helped writer a presentation known as the Crestwood Comeback that we despatched to administration and made public.

The place CEQP stands right this moment versus when my previous agency took that place is sort of outstanding, and lots of credit score as to go to Bob Phillips and Robert Halpin and the CEQP crew. When my previous agency owned it, the corporate went from CEQP 1.0 to CEQP 2.0, because it mounted its steadiness sheet, proper sized its distribution, and bought some non-core property. Immediately, that is CEQP model 3.0, the place the corporate has gotten rid of most of its legacy property to focus on its core Bakken and Permian midstream property.

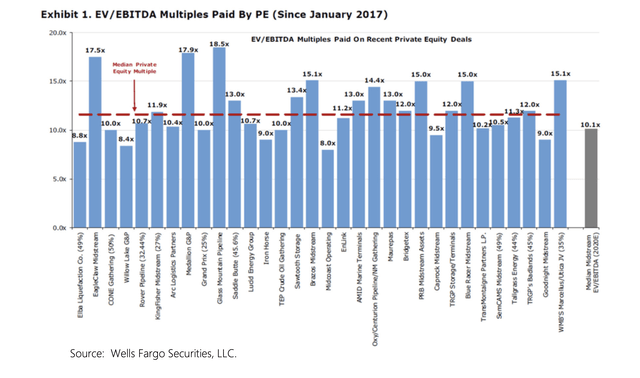

Whereas there could also be some noise as a result of earlier Bakken climate, CEQP stays in good condition and the inventory seems undervalued at present ranges. On the whole, I feel a lot of the midstream area is undervalued. Sometimes, earlier than the pandemic, midstream corporations could be valued round 12x within the personal markets and over 10x within the public markets. Valuations have been even larger a number of years again. Notably, most of those corporations are in higher monetary form right this moment (higher steadiness sheets, no IDRs), however commerce at decrease valuations than they did a number of years in the past.

Wells Fargo

The over 10% yield is enticing for revenue buyers, and its protection is robust. buyers can even take a look at its most popular shares (CEQP.P), which additionally supply a superb worth. The popular shares yield 9.4% and have a lot much less volatility in comparison with the frequent.

I proceed to price the inventory a “Purchase.”

{kind=link}