miromiro

Earnings of Bankwell Monetary Group, Inc. (NASDAQ:BWFG) will possible stay flattish subsequent yr. Mortgage progress will proceed to help earnings by means of the tip of 2023. Nevertheless, slight margin compression, above-average provisioning, and inflation-driven progress in working bills will pressurize earnings. General, I am anticipating Bankwell Monetary to report earnings of $4.86 per share for 2022 and $4.81 per share for 2023. In comparison with my final report on the corporate, I’ve raised my earnings estimates largely as a result of I’ve elevated my mortgage stability estimates. Subsequent yr’s goal value suggests a excessive upside from the present market value. Due to this fact, I am sustaining a purchase ranking on Bankwell Monetary Group.

After 3Q’s Wonderful Efficiency, Mortgage Development to Sluggish Down

Bankwell Monetary’s mortgage portfolio surged by an distinctive 11% through the third quarter, or 44.5% annualized, which not solely beat my expectations but in addition smashed historic data. Going ahead, mortgage progress will average due to the excessive interest-rate surroundings which ought to dampen the credit score urge for food of debtors. Additional, Bankwell Monetary closed a department efficient October 7, 2022. The financial institution now has solely 9 branches operational. The department closure also needs to have some detrimental results on mortgage originations.

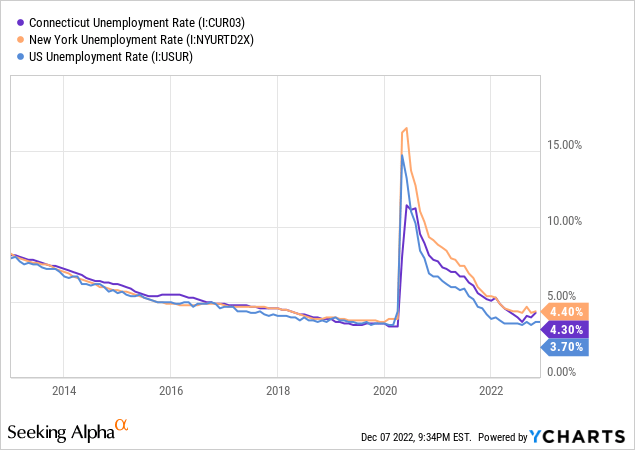

In the meantime, financial elements may have a blended influence on mortgage progress. Bankwell Monetary is predicated in Connecticut, with a majority of its loans in Connecticut and New York. The corporate additionally has some publicity to Florida, Texas, New Jersey, and Ohio. At the moment, each Connecticut and New York have excessive unemployment charges in comparison with different states. Nevertheless, in comparison with their historic developments, the unemployment charges have remained very low this yr. Sturdy job markets present a optimistic sign for mortgage progress within the business enterprise section, which makes up round 19% of whole loans. Business actual property loans make up an extra 72% of whole loans; nevertheless, this section is much less intently associated to the employment state of affairs.

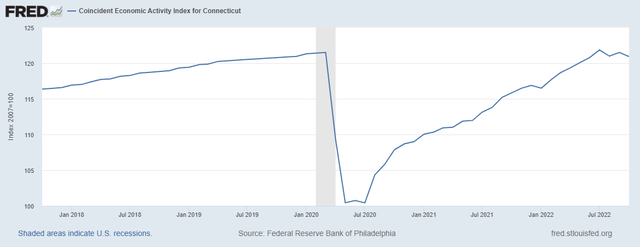

Connecticut’s coincident financial exercise index is one other good gauge of demand for business loans. The index under exhibits that financial exercise has been faltering recently.

The Federal Reserve Financial institution of Philadelphia

Contemplating these elements, I am anticipating the mortgage portfolio to develop by 3% within the final quarter of 2022, taking full-year mortgage progress to 24%. For 2023, I am anticipating the portfolio to develop by 10%. In comparison with my final report on the corporate, I’ve lowered my mortgage progress estimates for subsequent yr. However, my mortgage stability estimate is greater than earlier than. That is due to the surprisingly excessive mortgage progress through the third quarter, which has raised the bottom for the proportion.

The next desk exhibits my stability sheet estimates.

| Monetary Place | FY18 | FY19 | FY20 | FY21 | FY22E | FY23E |

| Internet Loans | 1,587 | 1,589 | 1,602 | 1,875 | 2,331 | 2,573 |

| Development of Internet Loans | 4.3% | 0.1% | 0.8% | 17.1% | 24.3% | 10.4% |

| Different Incomes Belongings | 119 | 101 | 111 | 161 | 125 | 130 |

| Deposits | 1,502 | 1,492 | 1,827 | 2,124 | 2,355 | 2,600 |

| Borrowings and Sub-Debt | 185 | 175 | 200 | 84 | 160 | 167 |

| Widespread fairness | 174 | 182 | 177 | 202 | 236 | 257 |

| Ebook Worth Per Share ($) | 22.4 | 23.4 | 22.8 | 26.0 | 31.0 | 33.8 |

| Tangible BVPS ($) | 22.1 | 23.1 | 22.5 | 25.7 | 30.7 | 33.4 |

| Supply: SEC Filings, Earnings Releases, Writer’s Estimates (In USD million except in any other case specified) | ||||||

Additional Margin Contraction Forward

Bankwell Monetary’s web curiosity margin grew by eleven foundation factors within the third quarter because of the giant mortgage addition at greater charges. Going ahead, the anticipated mortgage additions will proceed to help the margin. Nevertheless, the repricing of present loans and deposits will pressurize the margin. On account of a big stability of adjustable charge deposits, the common deposit price reprices sooner than asset yields. These adjustable-rate deposits, particularly NOW, financial savings, and cash market accounts, altogether made up 60% of whole deposits on the finish of September 2022. Additional, certificates of deposits representing 13% of whole deposits are scheduled to mature earlier than year-end. Compared, solely $500 million of loans are floating or set to re-price within the subsequent twelve months, representing simply 22% of whole loans, as talked about within the earnings presentation.

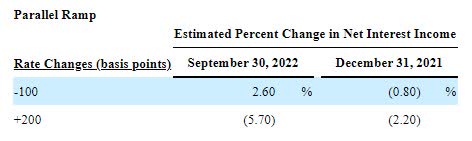

Based on the outcomes of the administration’s interest-rate sensitivity evaluation given within the 10-Q submitting, a 200-basis factors hike in rates of interest may scale back the online curiosity revenue by 5.7% over twelve months.

3Q 2022 10-Q Submitting

The administration expects the margin to contract within the fourth quarter of 2022 and the complete yr of 2023. Contemplating these elements, I am anticipating the margin to say no by 15 foundation factors within the final quarter of 2022 and 20 foundation factors in 2023.

Provisioning Prone to Stay Above Regular

Bankwell Monetary Group reported an above-average provisioning for the third quarter of 2022, which beat my expectations. That is pure contemplating mortgage progress was additionally surprisingly excessive through the quarter. Non-performing loans had been 0.73% of whole loans, whereas allowances had been 0.80% of whole loans on the finish of September 2022. This allowance protection appears uncomfortable to me forward of a doable recession. Due to this fact, I consider Bankwell Monetary might want to make above-average contributions to allowances for mortgage losses. The corporate just isn’t but subjected to the Present Anticipated Credit score Losses (“CECL”) accounting customary, which makes it extra susceptible to credit score shocks.

General, I am anticipating the online provision expense to make up 0.23% of whole loans in 2023, which is way greater than the common of 0.16% for the final 5 years.

Anticipating Earnings to be Flattish Subsequent Yr

The anticipated mortgage progress will possible help earnings by means of the tip of 2023. However, slight margin compression and above-average provisioning will drag earnings. Additional, working bills will rise as a result of stability sheet progress in addition to persistent inflation.

General, I am anticipating Bankwell Monetary to report earnings of $4.86 per share for 2022, up 45% year-over-year. For 2023, I am anticipating earnings to dip by 1% to $4.81 per share. The next desk exhibits my revenue assertion estimates.

| Earnings Assertion | FY18 | FY19 | FY20 | FY21 | FY22E | FY23E |

| Internet curiosity revenue | 56 | 54 | 55 | 68 | 93 | 103 |

| Provision for mortgage losses | 3 | 0 | 8 | (0) | 4 | 6 |

| Non-interest revenue | 4 | 5 | 3 | 6 | 3 | 3 |

| Non-interest expense | 36 | 36 | 43 | 40 | 44 | 52 |

| Internet revenue – Widespread Sh. | 17 | 18 | 6 | 26 | 37 | 37 |

| EPS – Diluted ($) | 2.21 | 2.31 | 0.75 | 3.36 | 4.86 | 4.81 |

| Supply: SEC Filings, Earnings Releases, Writer’s Estimates(In USD million except in any other case specified) | ||||||

In my final report on Bankwell Monetary, I estimated earnings of $4.60 per share for 2022 and $4.57 per share for 2023. I’ve revised upwards my earnings estimates largely as a result of I’ve raised my estimates for the mortgage stability following the third quarter’s efficiency.

My estimates are primarily based on sure macroeconomic assumptions that will not come to go. Due to this fact, precise earnings can differ materially from my estimates.

BWFG is Buying and selling at a Large Low cost to its Goal Value

Bankwell Monetary has a long-standing custom of accelerating its dividend yearly. Given the earnings outlook, I’m anticipating the corporate to extend its dividend by $0.02 per share to $0.22 per share within the first quarter of 2023. The earnings and dividend estimates counsel a payout ratio of 18% for 2023, which is near the 2017-2021 (ex-2020) common of 20%. Primarily based on my dividend estimate, Bankwell Monetary is providing a ahead dividend yield of three.0%.

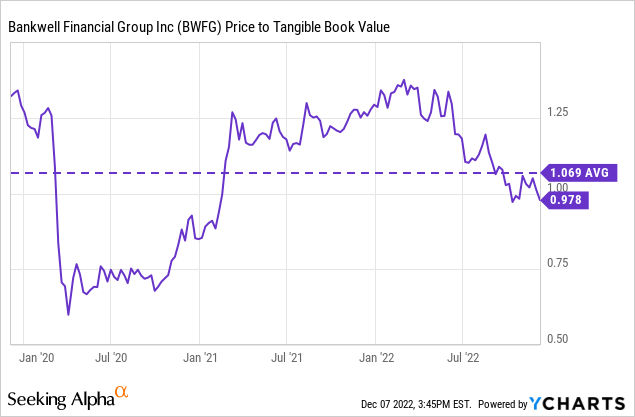

I’m utilizing the historic price-to-tangible guide (“P/TB”) and price-to-earnings (“P/E”) multiples to worth Bankwell Monetary Group. The inventory has traded at a mean P/TB ratio of 1.069 prior to now, as proven under.

Multiplying the common P/TB a number of with the forecast tangible guide worth per share of $33.4 offers a goal value of $35.7 for the tip of 2023. This value goal implies a 22.9% upside from the December 7 closing value. The next desk exhibits the sensitivity of the goal value to the P/TB ratio.

| P/TB A number of | 0.87x | 0.97x | 1.07x | 1.17x | 1.27x |

| TBVPS – Dec 2023 ($) | 33.4 | 33.4 | 33.4 | 33.4 | 33.4 |

| Goal Value ($) | 29.1 | 32.4 | 35.7 | 39.1 | 42.4 |

| Market Value ($) | 29.1 | 29.1 | 29.1 | 29.1 | 29.1 |

| Upside/(Draw back) | (0.1)% | 11.4% | 22.9% | 34.4% | 45.9% |

| Supply: Writer’s Estimates |

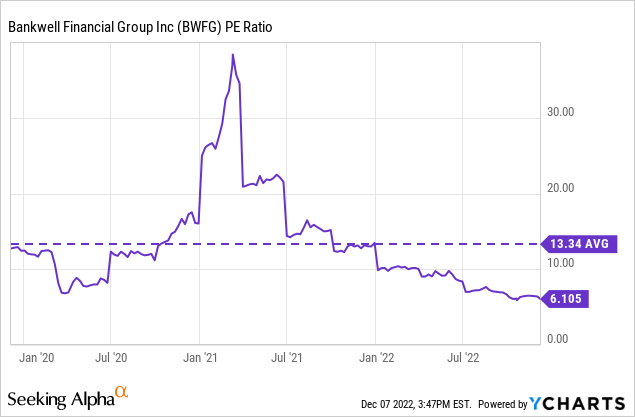

The inventory has traded at a mean P/E ratio of round 13.34x prior to now, as proven under. Excluding the anomaly within the first half of 2021, the P/E a number of has tended in the direction of 10.0x.

Multiplying the P/E a number of of 10.0x with the forecast earnings per share of $4.81 offers a goal value of $48.1 for the tip of 2023. This value goal implies a 65.4% upside from the December 7 closing value. The next desk exhibits the sensitivity of the goal value to the P/E ratio.

| P/E A number of | 8.0x | 9.0x | 10.0x | 11.0x | 12.0x |

| EPS 2023 ($) | 4.81 | 4.81 | 4.81 | 4.81 | 4.81 |

| Goal Value ($) | 38.5 | 43.3 | 48.1 | 52.9 | 57.7 |

| Market Value ($) | 29.1 | 29.1 | 29.1 | 29.1 | 29.1 |

| Upside/(Draw back) | 32.3% | 48.8% | 65.4% | 81.9% | 98.4% |

| Supply: Writer’s Estimates |

Equally weighting the goal costs from the 2 valuation strategies offers a mixed goal value of $41.9, which suggests a 44.1% upside from the present market value. Including the ahead dividend yield offers a complete anticipated return of 47.2%. Therefore, I’m sustaining a purchase ranking on Bankwell Monetary Group.

{kind=link}