muhammet sager

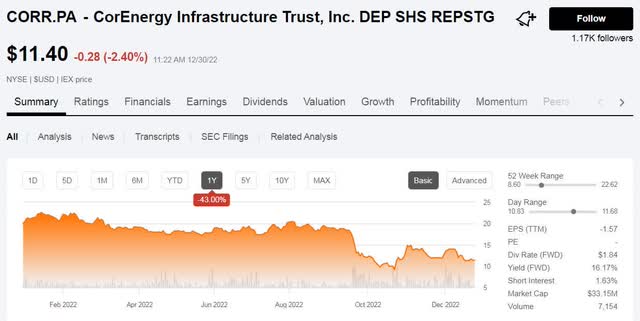

CorEnergy Infrastructure Belief (NYSE:CORR) is a REIT that owns and leases pipeline property for the transport of crude oil and pure gasoline on the west coast of the US. The corporate has a Collection A Cumulative Most well-liked share (NYSE:CORR.PA) that’s presently buying and selling at 46% of par worth ($11.40/$25) producing a dividend yield of over 16%. After weighing the dangers concerned within the enterprise, I imagine the popular shares are nonetheless a very good funding for earnings traders.

In search of Alpha

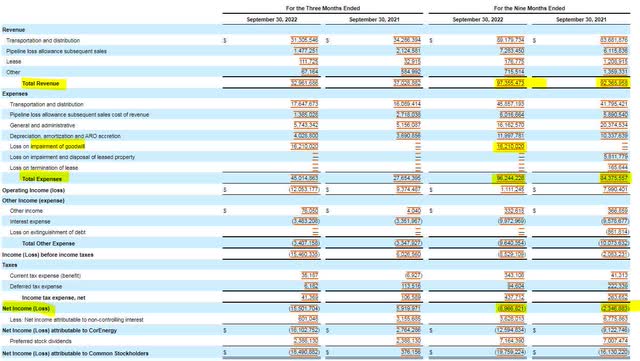

CorEnergy’s earnings assertion reveals that the corporate has grown income within the first 9 months of 2022 by $5 million in comparison with the identical interval in 2021. Whereas bills have grown by greater than income, this improve, and subsequent internet loss was brought on by the impairment of goodwill (a noncash expense). If we take away the impairment prices (from each 2021 and 2022), we’ll discover that working bills grew by solely $2 million and working earnings in 2022 primarily based on this adjustment can be $17 million, almost double the corporate’s curiosity expense.

SEC 10-Q

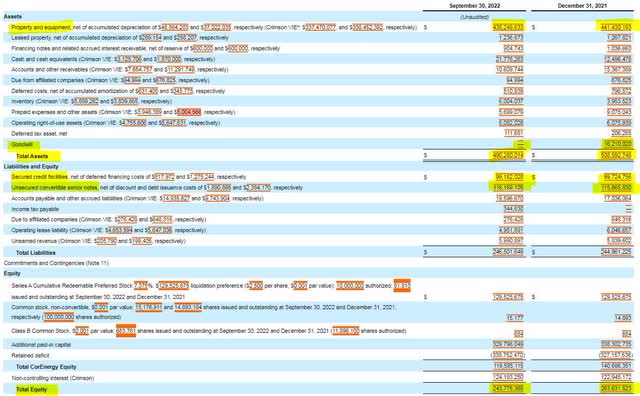

CorEnergy’s steadiness sheet is a consolidated, reduce and dry doc. The corporate’s property are primarily comprised of the pipelines, listed as property and gear. The legal responsibility facet is comprised largely of secured credit score amenities and convertible senior notes. The one vital change to the steadiness sheet in 2022 has been the impairment of goodwill, which led to the lower of the corporate’s complete fairness. Total, CorEnergy has maintained a steady capital place all year long.

SEC 10-Q

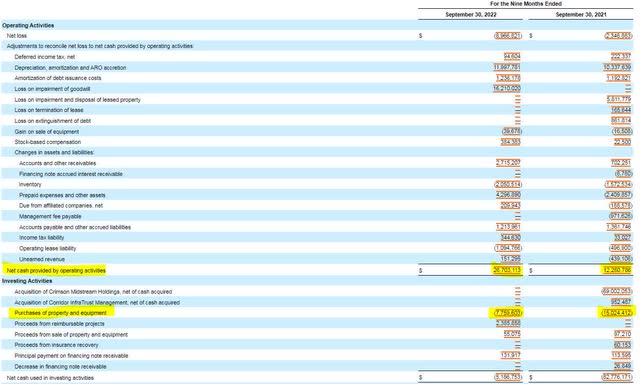

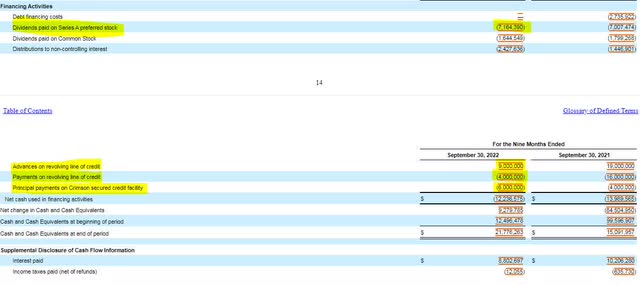

When it comes to money move, CorEnergy has doubled its working money move within the first 9 months of 2022 in comparison with 2021. After capital expenditures, the corporate has free money move of $19 million, which is sufficient to cowl its most popular dividend obligation of simply over $7 million. It is also essential to notice that CorEnergy didn’t add debt in 2022 and was capable of improve its money place from $12 million to $21 million.

SEC 10-Q SEC 10-Q

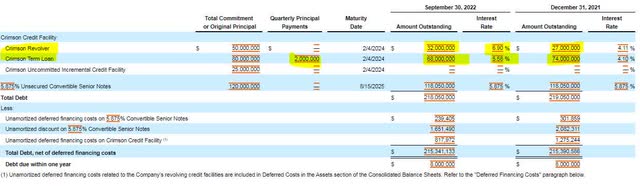

One concern relating to CorEnergy lies in all its debt maturing in 2024 and 2025. The corporate has $100 million in revolver and time period mortgage debt that has already seen a rise in curiosity expense in comparison with final 12 months. CorEnergy does appear to be making ready for a capital increase ought to the corporate want it. They’ve a shelf registration on file that permits it to lift as much as $600 million in capital by way of both inventory or debt choices. The refinancing want mixed with the shelf registration is why I’m not advocating for funding within the firm’s widespread shares, as a result of I imagine they stand to be diluted by any capital increase.

SEC 10-Q SEC 10-Q

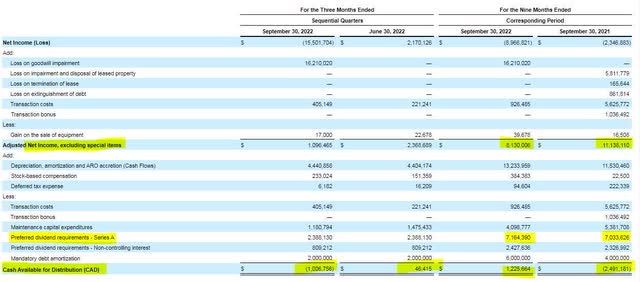

One other concern that traders have to weigh is the money obtainable for distribution evaluation. That is an inner calculation used to find out the viability of the corporate’s dividend. CorEnergy’s third quarter efficiency did push the money obtainable for distribution downward, however the firm nonetheless has money obtainable for distribution after taking the popular dividends into consideration and the necessary principal funds on the corporate’s time period mortgage. It is also essential to notice that the corporate maintained widespread and most popular dividends in 2021 regardless of a destructive money obtainable for distribution.

SEC 10-Q

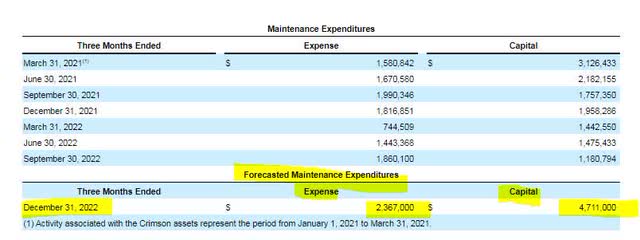

Probably probably the most tangible risk to the corporate’s money move capabilities lies in its capital expenditures forecast. In a single part of its most up-to-date 10-Q, CorEnergy disclosed a large anticipated improve to capex within the fourth quarter of 2022. When earnings are launched, traders ought to count on money obtainable for distribution to be destructive for the 12 months. Wanting additional into the long run, the corporate is predicted to make extra investments to its property in late 2023 and early 2024 associated to laws in California.

SEC 10-Q SEC 10-Q

CorEnergy is implementing a surcharge that will likely be used its late 2023/early 2024 capital obligations, so traders ought to count on these to not be financed from present working money flows. Moreover, the shelf registration might simply fund these anticipated will increase.

Ought to CorEnergy select to remove its dividends, the execution of a capital increase would grow to be tougher and the sorts of choices would grow to be extra restricted. Total, whereas the corporate is going through headwinds within the type of capital commitments and debt refinancing, I imagine that CorEnergy has positioned itself to face these challenges with out the sacrifice of its dividends.

Editor’s Be aware: This text covers a number of microcap shares. Please concentrate on the dangers related to these shares.

{kind=link}