mrPliskin/E+ by way of Getty Photographs

We’re beginning to see the foundations of the tech rally start to crack. Earnings season is properly underway, and although most corporations have reported large beats to steerage and expectations, Wall Road’s reactions have been comparatively muted. The trigger right here: with valuations having soared for the reason that begin of the 12 months, most shares had been already priced for perfection – and something lower than good acquired walloped post-earnings.

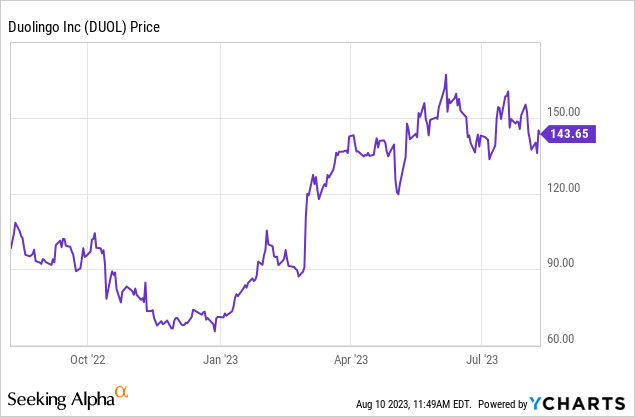

Duolingo (NASDAQ:DUOL) is a good instance right here. The language-learning app posted an admirable beat-and-raise quarter that noticed acceleration in top-line metrics plus beneficiant margin will increase. Nonetheless, the inventory is under June highs – although we won’t low cost the truth that it has greater than doubled 12 months up to now.

My outlook on Duolingo all through the remainder of the 12 months stays bearish. In my private view, the corporate has executed tremendously properly towards a tricky backdrop. Even amongst normal malaise within the subscription-services trade (with Netflix (NFLX) ending password-sharing and Disney (DIS) elevating the costs of each Disney+ and Hulu), Duolingo has thus far averted any destructive penalties (many together with myself had feared that if shoppers allotted extra money towards streaming companies, they’d overview their month-to-month bills extra fastidiously and reduce out apps like Duolingo if not closely used).

However wanting forward, I nonetheless have two main considerations: a scarcity of actual progress drivers plus an enormous valuation.

Duolingo has succeeded not too long ago in changing a number of customers into paid subscribers. It has put a number of advertising behind the branding of its new subscription product, Tremendous Duolingo, with a number of new options like Clarify My Reply which might be supposed to copy what a human language tutor would possibly be capable of present. However on the identical time, will these AI options actually drive non-subscribers off the proverbial sofa? Can Duolingo achieve continued subscriber retention as soon as this sizzling summer season journey season ends? The corporate has, to its credit score, spent little or no on consumer acquisition, preferring restricted social media campaigns with tie-ins to present trending matters reminiscent of Barbie. It may re-allocate a few of its margin positive factors again into consumer acquisition if progress slows down, however I’m involved that its interval of natural progress will enter right into a deceleration part because it begins to lap more durable comps.

Second – we won’t ignore Duolingo’s ultra-premium valuation. At present share costs close to $144, Duolingo trades at a market cap of $5.90 billion. After we internet off the $678.7 million of money on Duolingo’s most up-to-date steadiness sheet, the corporate’s ensuing enterprise worth is $5.22 billion.

For the present fiscal 12 months, Duolingo has boosted its full-year outlook to $510-$516 million (38-40% y/y progress), versus a previous outlook of 35-38% y/y progress – successfully making the outdated excessive finish of its vary its new low finish.

Duolingo outlook (Duolingo Q2 earnings deck)

To what extent, nevertheless, is power already priced into Duolingo’s inventory? It sits at 10.2x EV/FY24 income primarily based on the midpoint of its new steerage vary, and if we play ahead its multiples to FY24 the place consensus is anticipating $653.0 million in income (+27% y/y), its valuation nonetheless stands at 8.0x EV/FY24 income.

In my opinion, Duolingo will steadily see a number of factors of income and bookings deceleration per quarter (as implied in its steerage), with danger of subscriber churn within the again half of the 12 months very prevalent as macro circumstances drag on and summer season journey ends. I count on Duolingo to get pushed all the way down to a ~7x FY24 income a number of by year-end, implying a $128 value goal and ~12% draw back from present ranges.

The underside line right here: I believe Duolingo has capped out its potential with its beneficiant YTD rally. From right here it is principally draw back, and there may be extra danger than reward in investing within the inventory at its present ranges. Steer clear and make investments elsewhere.

Q2 obtain

That being stated, we’ll acknowledge the power of Duolingo’s most up-to-date outcomes. The Q2 earnings abstract is proven under:

Duolingo Q2 outcomes (Duolingo Q2 earnings deck)

Income grew 43% y/y to $126.8 million, beating Wall Road’s expectations of $123.7 million (+40% y/y) by a three-point margin. Progress additionally accelerated one level versus 42% y/y in Q1, partly pushed by softening FX headwinds.

From a consumer standpoint, day by day energetic customers grew 62% y/y to 21.4 million, on the identical progress tempo as in Q1 and a 900k sequential add within the quarter. Paid subscribers, in the meantime, added 400k quarter-over-quarter and rose to five.2 million, up 59% y/y.

Duolingo consumer metrics (Duolingo Q2 earnings deck)

Platform bookings additionally grew 41% y/y to $137.5 million, eclipsing income on a nominal foundation. Additionally of notice is the truth that in-app purchases, although comparatively small (complete “different” income of $8.8 million represented solely 7% of the corporate complete), grew greater than 100% y/y.

Right here is commentary from CEO Luis Von Ahn’s remarks on the Q2 earnings name, detailing the corporate’s subscriber acquisition traits and technique:

We delight our learners who inform their family and friends about us, which drives our natural word-of-mouth progress. Add to that, our distinctive and environment friendly, although at instances unhinged, strategy to advertising, and also you get a model that has develop into synonymous with language studying. And that creates alternatives for us to be a part of cultural moments, such as you noticed this previous month, once we had been referenced within the Barbie film. I ought to point out that this was an inbound request to us. We did not search out being within the movie, which I believe is a mirrored image on the power of our model.

Over the previous 8 quarters, we have seen very robust DAU progress, and that progress has been high-quality and has been broad primarily based with customers coming from all areas of the world. The U.S. continues to develop properly, and a few of our quickest progress have come from the wealthier European nations. This progress not solely validates the massive addressable market of language learners, however due to the ability of our freemium enterprise mannequin, which I’ve mentioned in earlier shareholder letters, robust consumer progress drives robust monetary efficiency.

We entice free customers primarily by means of phrase of mouth. We delight them by means of product enhancements pushed by experimenting and optimizing the app, after which we convert them to paid subscribers. This playbook for rising subscribers has labored exceptionally properly.”

From a price perspective, Duolingo additionally managed to deliver down gross sales and advertising prices by 3 factors as a share of income, and generate and administrative prices by 5 factors:

Duolingo opex rends (Duolingo Q2 earnings deck)

Adjusted EBITDA grew considerably to $20.9 million, representing a 16.5% adjusted EBITDA margin and greater than ten factors of leverage y/y, whereas free money circulate in Q2 greater than tripled to $34.3 million.

Duolingo margins (Duolingo Q2 earnings deck)

Key takeaways

Prime quality at a excessive value – Duolingo has all the time been this model of funding, although I believe with markets shaking off all-time highs, the chance is now larger. Keep away from this inventory and make investments elsewhere.

{kind=link}