bin kontan

Nationwide Well being Buyers Inc. (NYSE:NHI) is a senior housing and expert nursing REIT. This sector, which was the fashion pre-COVID-19, obtained into lots of difficulties after March 2020. The sector confronted challenges from the excessive ranges of mortality inflicted by COVID-19 on its main customers. It additionally confronted elevated prices from sustaining a protected atmosphere. Labor prices then exploded in 2022 and that was one other drawback they wanted to cope with. As a REIT, the “sit again and accumulate lease” mannequin didn’t work for NHI or another REIT on this sector. In reality, in the event you return and see the final 10 years, this mannequin has not likely labored. The tenants have typically had poor lease protection and their low-margin enterprise required fixed subsidies and bailouts. However the REIT has stepped up and handled these headwinds. We have a look at the place NHI stands right this moment and whether or not one could make a great investing case for this 7% yielder.

Q3-2023

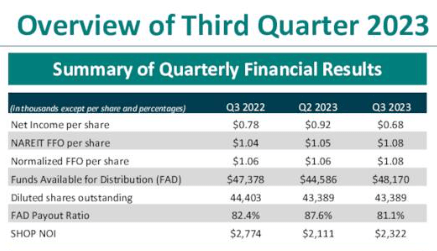

NHI simply launched its Q3-2023 outcomes and normalized funds from operations (FFO) improved modestly $1.08 per share. Funds obtainable for distribution, or FAD, improved as properly and the FAD payout ratio moved a smidge decrease to 81.1%.

NHI Q3-2023 Presentation

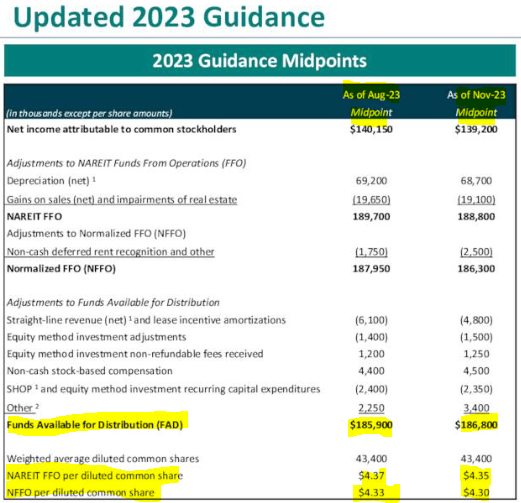

Regardless of a barely stronger Q3-2023 than anticipated, NHI trimmed its FFO and Normalized FFO steering. On account of a barely decrease quantity of lease incentives granted, FAD steering went up.

NHI Q3-2023 Presentation

The numbers do not materially change the story although. At $4.30 of NFFO, NHI is comfortably protecting the dividend. Extra importantly for traders, NHI claims to be on the opposite aspect of the “hump” so far as coping with its issues. In assessing the validity of the above assertion, is the place the investing case must be made. So let’s take a look at that.

Portfolio Optimization

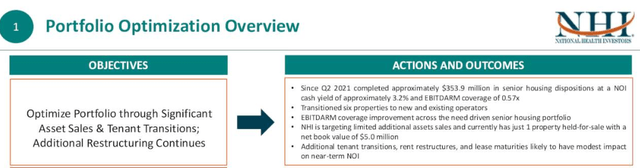

The very first thing that NHI has finished efficiently is promote deadbeat properties. You possibly can see that within the “money yield” 3.2% and the sale value of $353.9 million.

NHI Q3-2023 Presentation

In essence, NHI was in a position to promote properties at what could be known as very low cap charges. These properties typically had a tenant who was not even paying lease or paying a fraction of the lease. It was the most effective illustrations of actual property holding its worth. Even when the property had zero enchantment utilizing standard rent-generating metrics from present tenants, presumably different components like substitute price or different use worth, got here into play. After all, changing the tenant with a stronger one is also a motivating issue, but when it was really easy, NHI would have finished it, as a substitute of promoting the property. The underside line is that this obtained finished and NHI obtained beneficial money move when it wanted it probably the most.

Brickford and Vacation have been two different drawback youngsters they usually weren’t straightforward to place away. NHI granted Brickford a giant lease reset and in addition transitioned Vacation to a SHOP setting.

NHI Q3-2023 Presentation

For these unaware, SHOP signifies that it’s a Senior Housing Working Portfolio and NHI has upside and draw back on these properties. It’s now not simply amassing lease.

NHI did steps one and two in a way that they offset the leverage affect. The very low cap price gross sales offset the lease cuts and transfer to SHOP (which was instantly EBITDA adverse).

NHI Q3-2023 Presentation

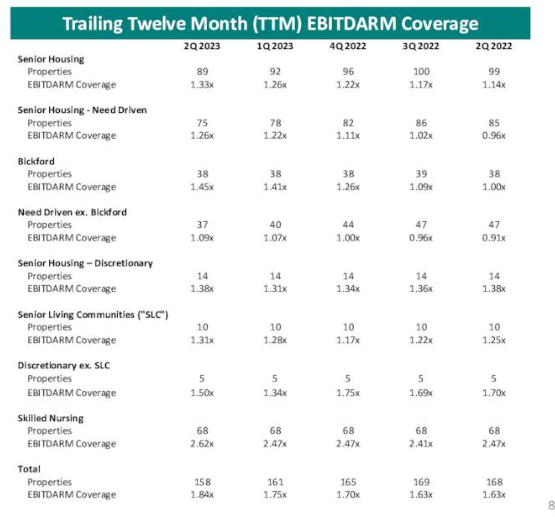

The top end result has been fairly spectacular and maybe the very best metric right here is the tenant well being as measured by EBITDARM (earnings earlier than curiosity, taxes, depreciation, amortization, lease and administration charges) metric. You possibly can see beneath that we’re seeing some constant trailing 12-month enchancment throughout each single class.

NHI Q3-2023 Presentation

Outlook & Verdict

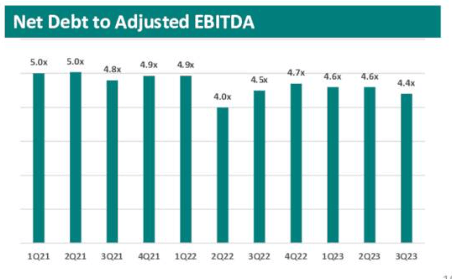

NHI’s steadiness sheet appears in fine condition with debt to adjusted EBITDA at simply 4.4X.

NHI Q3-2023 Presentation

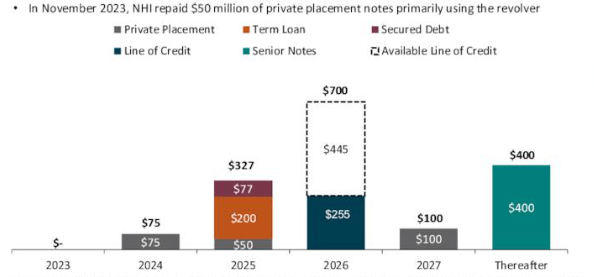

Some would possibly argue that that is very low for a REIT, however this isn’t a triple-net retail REIT. The tenants listed here are infamous for points and calls for for lease cuts. So 4.4X is sweet, however positively not one thing to put in writing house about. The maturities are properly spaced out as properly. Notice that the road of credit score has sufficient room to soak up the whole 2025 maturity schedule, although we doubt will probably be wanted.

NHI Q3-2023 Presentation

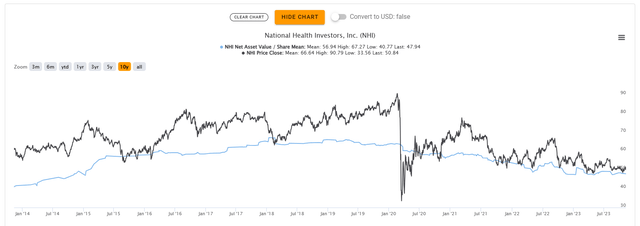

The inventory sports activities a 7% yield and an 80% payout ratio. Whereas it trades at a small premium to estimated NAV, that is decrease than what we now have seen over the past decade.

TIKR

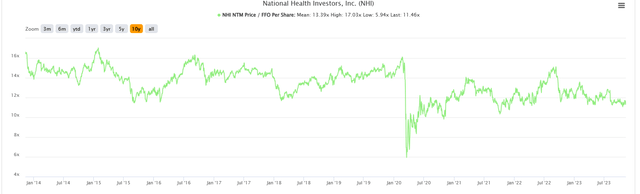

The 12X FFO a number of will not be too unhealthy both and displays the final apathy in direction of REITs.

TIKR

At current, we predict NHI is a worthy consideration for addition to any portfolio that lacks ample REITs. Whereas we’re warming as much as this one, we do not see a runaway bull market right here. Utilizing a conservative purchase level would most likely contain on the lookout for a sub $47.00 entry value. Alternatively, traders can juice their returns and cut back their threat utilizing the $50 lined calls. At current, the longest-dated ones obtainable are for April 2024. That coupled with the comparatively low implied volatilities signifies that we’re nonetheless staying on the sidelines. We price this a maintain whereas noting the potential for good returns from right here. We additionally assume the 2031 bonds with a 7.57% yield to maturity are price contemplating.

FINRA

If get an 8.0% plus yield to maturity on these in a meltdown, we would purchase these as properly.

{kind=link}