yangphoto/E+ through Getty Photographs

We proceed to be hold-rated on DoorDash (NASDAQ:DASH) regardless of administration’s better-than-expected steering. We predict the market has priced within the expectation of restoration after the inventory jumped greater than 15% on incomes outcomes. We predict the inventory’s increased valuation shouldn’t be justified for our expectations of DoorDash’s slower progress trajectory by means of 1H24. Per our expectations again in early August once we downgraded the inventory, the corporate’s complete order progress decelerated each QoQ and Y/Y this quarter. We predict macro headwinds will proceed to weigh on client spending within the again finish of the yr and see macro headwinds spilling into 1H24. Therefore, we predict it will be harder for DoorDash to reaccelerate order progress or market GOV below the present high-interest charge and tight finances surroundings.

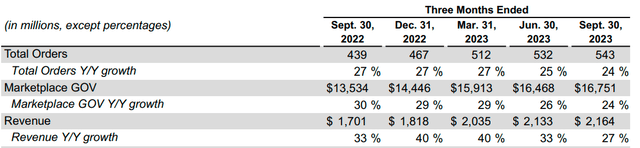

Complete order progress Y/Y has been slowing; this quarter, complete orders elevated 24% Y/Y versus 25% 1 / 4 in the past and 27% Y/Y in 3Q22. Market GOV additionally slowed to 24% in comparison with a better 26% in 2Q23 and 30% in 3Q22. We’re constructive on the uptick in client spending, particularly on meals supply, however we do not suppose it is going to be an in a single day sort of restoration. We now see a extra gradual progress tempo for DoorDash in 1H24 as a consequence of still-easing macro headwinds. We imagine the expansion for complete order, market GOV, and income will stay within the double-digit vary however see a slower progress runway as macro weak point spills into subsequent yr.

The next desk outlines the 3Q23 outcomes for DoorDash.

3Q23 earnings press launch

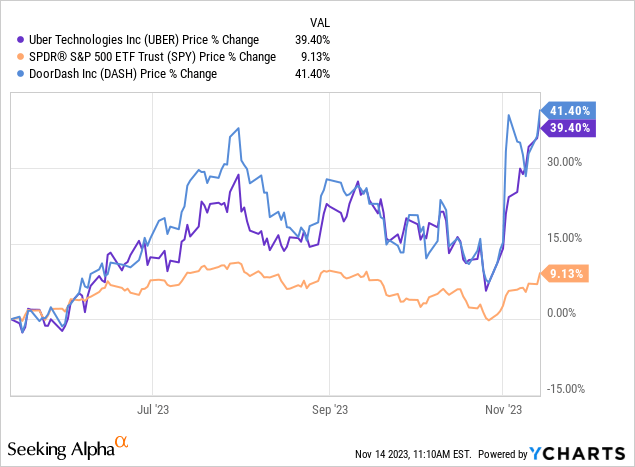

For the corporate to financially outperform, it must materially exceed the steering of 17-17.4B for market GOV, and we do not see this occurring within the near-term. Whereas we see indicators of client spending remaining resilient, we predict traders ought to be cautious about getting too excited too early. The CNBC/NRF Retail Monitor report for the month of October discovered retail gross sales fell 0.08% through the interval. We count on softer client spending to weigh on Market GOV progress subsequent quarter. We’re nearer to the restoration now, however we do not suppose we have hit the infliction level but. The inventory is up 41% over the previous 6M versus the S&P 500 up 9% throughout the identical interval, and Uber (UBER) up 39%. The next outlines the inventory’s six month efficiency towards Uber and S&P 500.

YCharts

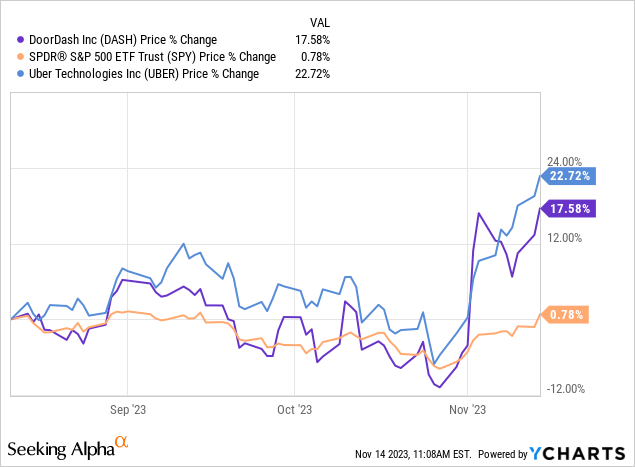

Nonetheless, we predict outperformance is moderating even with administration’s top-line beat and better-than-expected steering. Over the previous three months, Uber has outperformed each the S&P 500 and DoorDash by 22% and 5%, respectively. The next graph outlines Sprint’s efficiency towards Uber and the S&P 500 over the previous three months.

YCharts

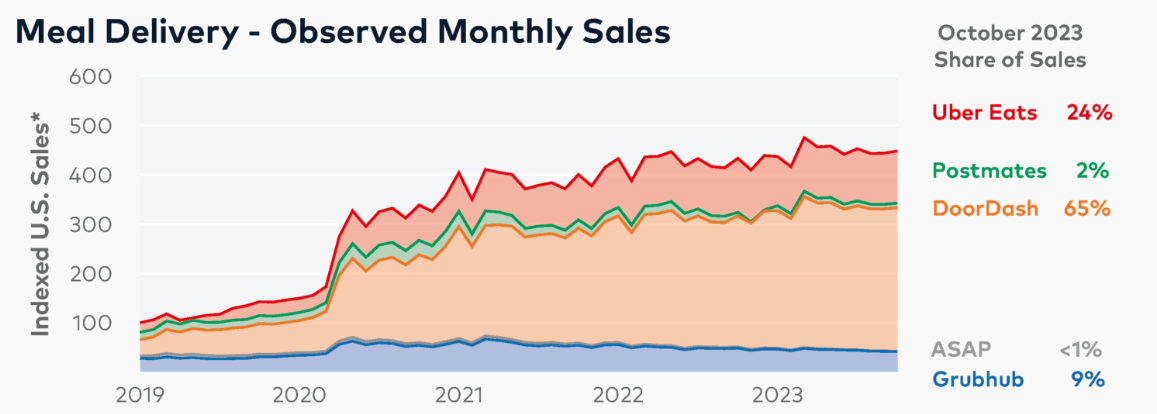

DoorDash nonetheless holds the vast majority of the meal supply market with a 65% share versus Uber at 24%. Whereas DoorDash has the higher hand on this market, we predict Uber’s diversified income throughout supply, mobility, and freight offers it a aggressive benefit over DoorDash on the supply entrance and Lyft (LYFT) on the mobility entrance throughout instances of macro uncertainty. We count on Uber’s supply enterprise to fare higher within the near-term than DoorDash’s enterprise.

The next graph outlines the meal supply market share for October 2023.

Bloomberg Second Measure October 2023

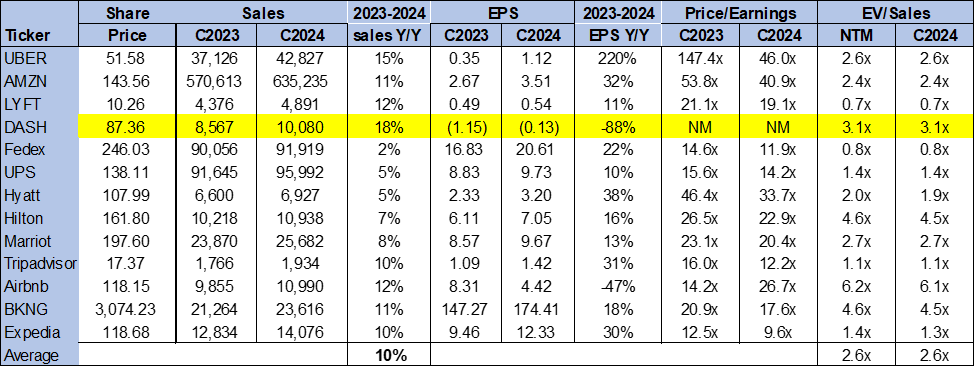

Valuation

We predict the inventory is overvalued for the near-term dangers current. The inventory is buying and selling at 3.1x EV/C2024 Gross sales versus the peer group common of two.6x. We do not suppose the upper valuation is justified as we count on Sprint’s progress charge to gradual into the primary half of subsequent yr. We suggest traders keep on the sidelines for the near-term as we do not see the inventory working.

The next chart outlines DASH’s valuation towards the peer group.

TSP

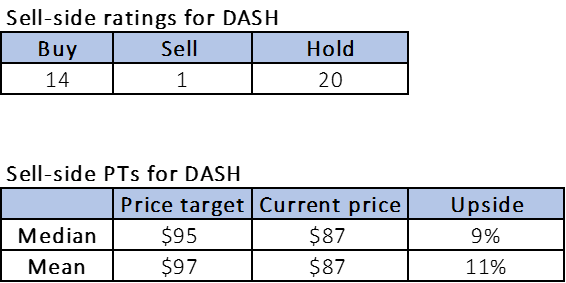

Phrase on Wall Avenue

Wall Avenue can be impartial on the inventory. Of the 35 analysts protecting the inventory, 14 are buy-rated, 20 are hold-rated, and the remaining is sell-rated. The inventory is at the moment priced at $87 per share. The median sell-side worth goal is $95, whereas the imply is $97, with a possible September 11% upside. We see minimal upside potential for the inventory within the near-term as a result of present macro backdrop; we predict there’s an upside threat if client spending rebounds materially subsequent yr or sees a seasonal uptick from the vacations.

The next charts define DASH’s sell-side scores and price-targets.

TSP

What to do with the inventory

We proceed to be hold-rated on DoorDash. We do not see the inventory materially outperforming within the near-term as macro headwinds spill into 1H24. We’re much less optimistic a few significant reacceleration of progress in complete orders and market GOV within the near-term. We predict DoorDash will likely be extra of an in-line performer within the near-term and therefore suggest traders keep on the sidelines.

{kind=link}