October 30, 2023 got here and handed — the date that marked the tip of Broadcom’s fiscal 12 months and the promised shut for its $61 billion VMware acquisition. In anticipation of that timing, VMware shareholders got till October 23 to determine whether or not to just accept Broadcom shares at $142.5 per share or money fee, of which 96% selected shares. However regardless of clearing a small hurdle with South Korea’s conditional approval, China delayed its approval till Tuesday, November 21. Causes for China’s stalling is speculated as a geopolitical transfer in response to the US authorities’s newest chip sanctions towards the nation.

The deal is now set to formally shut on November 22, 2023, simply earlier than the deal expiration date on Nov. 26. Now that the deal is formally closing, what ought to you recognize and anticipate?

What We Know So Far

Broadcom and VMware haven’t made a lot by way of official bulletins past three issues:

- VMware might be rebranded VMware by Broadcom.

- Broadcom’s CEO Hock Tan promised no worth will increase on VMware merchandise (although we now have already bore witness to VMware renewals which have gone up in multiples).

- Broadcom introduced at VMware Discover a $2 billion funding into VMware.

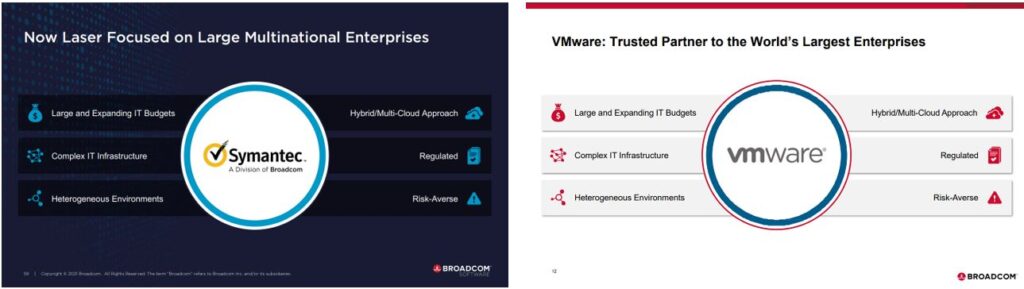

Past these, rumors abound, with leaked emails of recent job gives and anticipated large layoffs on the finish of October for VMware. However for a window into the longer term, merely look again to its earlier two main acquisitions, CA and Symantec. Between the 2 corporations, buyer assist diminished considerably, and innovation stunted from deprecated income funding in R&D (3% drop) and gross sales and advertising and marketing (22% drop). Broadcom claims that the VMware acquisition might be completely different, however its path appears to observe the identical as Symantec’s. Their paths are so related that they’ve the identical “reduce and paste” slideware (see the determine under).

(slides introduced to traders for the introduced Symantec acquisition [on left] and VMware acquisition announcement [on right])

What Ought to VMware Prospects Anticipate?

Over the subsequent few years:

- The VMware income stream will face challenges as clients go away in droves. Present and future clients cautious of the Broadcom model are alternate options, even when VMware is the clear market winner in capabilities for a given market. And in a number of product strains, fixed product reorganization and worker attrition means slower innovation with solely incremental updates at greatest. VMware’s income stream might be challenged as its enterprise clients finally escape the VMware stack. Anticipate large workforce discount to impression staff. This can additional impression assist high quality and jeopardize future roadmaps. However, a massively diminished workforce might very effectively counterbalance a few of its income losses.

- There might be vital streamlining and rebranding as VMware protects key property. As soon as the acquisition has closed, lesser-performing merchandise will doubtless sundown to fulfill Broadcom’s aggressive timeline of reaching an extra $3.8B in profitability in three years. Previous to Aria integrating beneath Tanzu, the Tanzu product line was ripe for selecting off. Poor market traction and its lack of ability to match market chief Crimson Hat OpenShift has led to its decline regardless of efforts to make it a key development initiative at VMware. As Aria and Tanzu now fall beneath one enterprise lead, Tanzu is beneath the protecting umbrella of its high-performing merchandise CloudHealth and Aria.

- vSAN will keep HCI dominance — however rivals will report growing curiosity. The newest launch, vSAN 8, is a rearchitected hyperconverged infrastructure (HCI) providing including options wanted to keep up VMware’s dominant market place for HCI. However regardless of creating a big community of cloud suppliers, system integrators, infrastructure distributors, and gross sales channels through which to embed vSAN, clients nonetheless entertain alternate options. Direct competitor Nutanix claims to be reaping the advantages of patrons who’re cautious of future excessive license prices and of merchandise with an unsure dedication to innovation. Nutanix CEO Rajiv Ramaswami said that “ […] the pending acquisition of our main competitor … has been serving to construct a robust pipeline that we anticipate will lengthen for years to return.”

- An unclear future for Horizon and Workspace ONE will make room for rivals. As we said beforehand, VMware’s worth proposition as a number one end-user computing vendor will lower its attractiveness beneath Broadcom’s file of poor buyer assist and slowed innovation. Whereas VMware’s end-user computing (EUC) portfolio continues to be robust, it has at all times taken a again seat to the corporate’s infrastructure merchandise. We wouldn’t be shocked to see VMware’s EUC enterprise spun out of Broadcom in consequence, but it surely’s too early to inform. Both method, the murkiness within the water creates extra room for rivals corresponding to Microsoft Intune and Home windows 365 to achieve market share.

- Carbon Black enhances Symantec on the endpoint facet however has plenty of catching as much as do. The corporate’s workload safety instruments are extensively used for hybrid cloud deployments and are thought of the de facto customary for cloud migrations. VMware lacks key elements, nonetheless: The endpoint safety instrument focuses on detection and response, leaving gaps in conventional endpoint safety. Within the endpoint safety platform market (however a lot much less robust within the endpoint detection and response/prolonged detection and response market), Carbon Black will complement its capabilities. Like Symantec, nonetheless, Carbon Black has fallen behind its rivals on the detection and response facet in recent times, leaving Broadcom with the most important hurdle of aggressive parity on either side of the coin. Past Carbon Black, the corporate lacks a real Zero Belief narrative to unify its disparate safety options, leaving questions round the way forward for NSX.

An Incoming Crash Touchdown

Whereas the deal has closed, don’t anticipate large disruption instantly. VMware’s software program is closely embedded in lots of mission-critical purposes in main enterprises. Plus, organizational change publish acquisitions takes some time to completely set in. The subsequent six months, nonetheless, might be telling about how Broadcom intends to navigate its newly discovered position within the cloud software program world. Don’t maintain your breath on a real success story through which VMware stays unaltered and its personal unbiased entity. Do anticipate worth hikes, degraded assist, and a VMware with a extra diluted worth prop.

{kind=link}