Let’s get one factor very clear, not each startup has to lift funding nor it’s the job of a startup to lift cash. Profitable founders usually are not very blissful once they elevate a brand new spherical of funding, as a result of they perceive that they didn’t really elevate any cash, they raised debt.

Rookie founders need to elevate to cut back their danger. Seasoned founders know that elevating cash on the fallacious time is only a expensive distraction.

It is best to solely think about elevating funding when your own home is so as. When every part goes actually, rather well.

There are two the explanation why. First, elevating funding received’t clear up any points {that a} startup has, even when that subject is that we’re working out of cash. Even when we elevate, we’ve simply delayed the inevitable. No quantity of capital will flip a nasty concept into a good suggestion. It is not going to assist with concept validation or reaching product-market match. It is not going to flip a fallacious group into a terrific group.

Traders hate chaos, and nice buyers can odor it from miles away.

Second, fundraising could be very time-consuming. On common in fundraising, a founder will spend 70% of their time on this one job for months, even a yr. This may steal the main target from tremendous essential duties of a founder equivalent to bettering the product, main the group, and attracting prospects.

Even when every part goes effectively, it nonetheless takes a really very long time to lift. Right now on common, for startup, it’ll take round 10 months to lift their spherical (Supply: Crunchbase). So if your own home just isn’t so as, if the co-founders and group usually are not selecting up the slack on duties {that a} founder doesn’t have time to do whereas fundraising, that startup is doomed to fail earlier than the elevate is over.

The most important purple flag for VCs is when startups begin elevating with none traction or earlier than their MVP. That is the worst time to go after fundraising. Not even on the accelerator stage that is OK. Concept validation ought to be finished earlier than the rest.

In case you don’t spend money on your self, why ought to I?

Every startup is definitely 3 totally totally different companies with 3 totally different targets:

Enterprise #1 (Concept Validation): The objective is to search out out if the concept is value doing or not.

On this stage, startups can select to self-fund, elevate from family and friends, get loans, be part of an accelerator, or elevate from angel buyers. That is usually referred to as the pre-seed spherical.

Enterprise #2 (PMF): The objective is to achieve regular development by securing a big, loyal fan base who love our product.

On this stage, startups can select to lift their seed spherical from early-stage VCs and angel buyers.

Enterprise #3 (Scale): The one job is to create a rising however sustainable enterprise.

On this stage, startups elevate their collection A, B, C, …. to develop their enterprise.

These are 3 totally different companies, they’re not the identical. Every thing modifications at every stage, greater than something, fundraising modifications dramatically in every of those phases.

When a startup is within the scale stage, they usually’re elevating their Sequence A, B, and so forth. it’s a completely totally different story than elevating for the pre-seed and seed phases. From Sequence A, VCs need to spend money on well-established, rising companies. Companies which might be scalable like startups, however on the similar time they’re a well-oiled machine, sustainable, not tremendous dangerous.

On the seed stage and earlier, VCs usually are not investing in a enterprise, they’re not even investing in an concept, they’re investing within the group.

VCs know that within the early phases, every part will change. Startups may pivot their product into a completely totally different product, they may change their enterprise mannequin, goal prospects, goal markets, and every part else about their firm. They’re not investing in a enterprise, reasonably they’re investing within the capability of that group to beat any impediment of their method and discover the expansion.

Crew is every part, a group is essentially the most worthwhile asset of any startup.

Everyone knows that 9 out of 10 startups fail within the very starting. One other statistic that folks don’t speak sufficient about is that 8 out of 10 startups that efficiently elevate cash, nonetheless fail within the subsequent 2–3 years of their life.

Early-stage VCs and buyers have one goal, discovering hero startups within the sea of zero ones, those that can ultimately flip right into a zero-dollar valuation ultimately.

That one hero startup will cowl all of the losses of all different investments that can fail. Hero startups don’t have nice concepts, they’ve nice groups. An ideal VC will determine the groups which might be able to making a hero sooner or later, and guess on them.

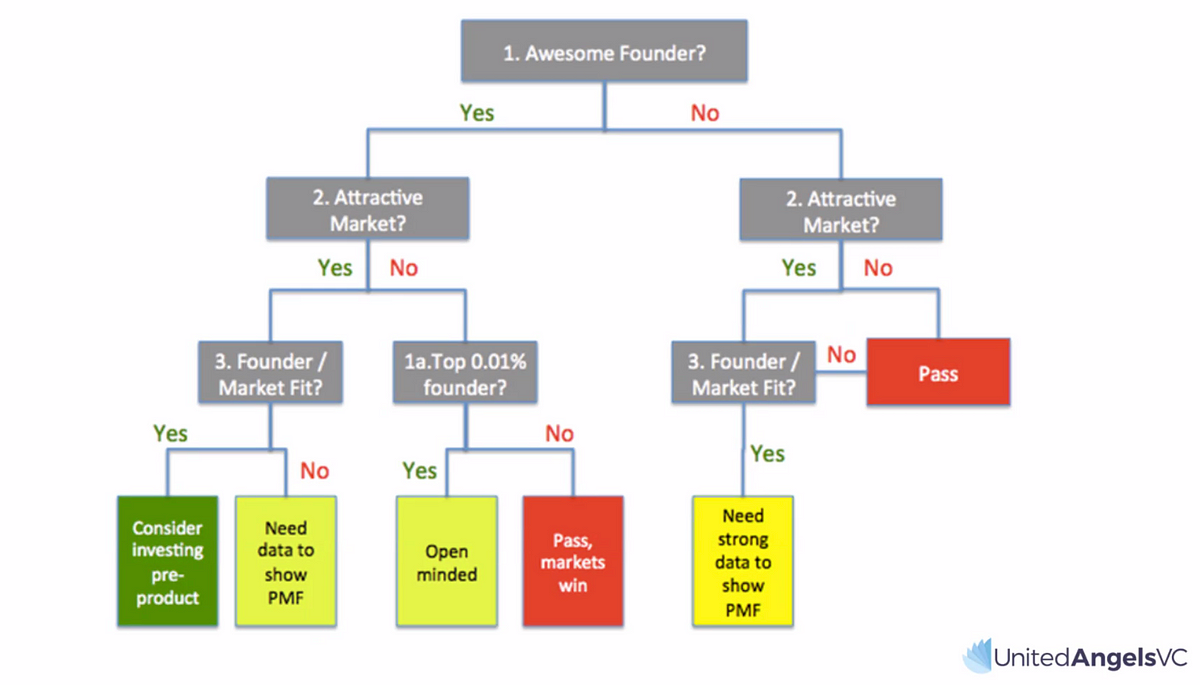

This flowchart exhibits how most VCs consider startups earlier than investing:

Identical as every part in startups, you’ll study it by doing it. As Aristotle says, “For the issues now we have to study earlier than we are able to do them, we study by doing them.”

VCs, accelerators, and angel buyers are people as effectively. Everybody prefers to work with folks whom they know, and that’s why you need to make connections and construct relationships earlier than you begin to elevate.

Being energetic within the startup ecosystem is essential and provides you an opportunity to attach with like-minded folks and brainstorm concepts collectively. It is best to know energetic members of your trade and attempt to get linked to them.

Conferences and startup occasions are nice locations for constructing these relationships. To not point out on-line occasions and LinkedIn, which allow you to attach with folks all around the world.

An effective way to get linked with potential buyers is by collaborating in pitch competitions. Finest case situation, you discover your future investor proper there, worst case situation, you may have practiced your pitch, obtained suggestions on it, and located what’s fallacious within the enterprise from difficult questions that buyers ask there.

The nice factor is whenever you speak with VCs earlier than you elevate, they may let you know their trustworthy suggestions, which exhibits what’s fallacious with the enterprise, and offer you some insights and concepts on find out how to enhance the enterprise, and find out how to make it able to be investable.

I all the time sucked once I needed to elucidate my startups to different folks, particularly at first. I couldn’t pitch the concept clearly, which meant that even I didn’t perceive my answer, so why ought to others?

Practising the elevator pitch of the startup with actual folks will present what’s fallacious with our concept. The eyes inform all of it. After each pitch, I realized what was fallacious with my concept, am I specializing in the fallacious downside that doesn’t exist? Am I specializing in an answer that’s not higher than others? Am I specializing in the fallacious market or the fallacious product positioning? A damaged elevator pitch will present all the issues within the enterprise.

After that, we fastened the essential elements of our startup and our home is so as, now that we made some connections, it’s time to begin reaching out to potential buyers. Listed here are the essential steps to outreach:

- Create a VC CRM

Record each potential investor that you simply’d like to have as your investor. Every investor should examine all of those bins:

1. They’re energetic in your trade and/or in your market.

2. They’ve a terrific status

3. They concentrate on the stage that you simply’re in proper now (Pre-seed, Seed, Sequence A, …) - Rating them from 1 to five, 5 being the perfect one you would like for. Take away those that rating low.

- If them, contact them straight. In case you don’t know them, attempt to discover a mutual connection and ask them to make an intro for you. It’s all the time higher to have a private intro.

- Don’t be afraid in the event you don’t discover an intro to them. Many VCs love chilly emails. E-mail them straight, message them on LinkedIn.

It really works greater than you assume, in my final spherical, we obtained 11 presents, 5 of which resulted from chilly emails. - Ship a really brief e-mail. Introduce your self and pitch your startup in just one sentence. After that, add one thing thrilling about your startup, like your traction, your group’s monitor document, KPI development, key companions, and something that makes you stand out.

Lastly, connect your pitch deck (the less slides the higher) and that’s it! VCs don’t have time to learn lengthy emails or pitch decks. On common, a VC analyst will take a look at your deck for lower than 30 seconds. - Meet with buyers, replace your CRM with the notes of every assembly, what went fallacious, what went effectively, and extra importantly, consider the VC to see in the event that they’re the precise associate for you or not.

- Rinse and repeat!

In our VC CRM, we stored monitor of those:

- The standing of every dialog

- The sensation towards that VC (Superior, Mediore, Terrible)

- Their goal areas

- Notable portfolios

- Focus areas/industries

- Most well-liked phrases (Lead investor, follower, typical funding kind)

- Deal dimension candy spot (How a lot they normally make investments)

There are a number of nice templates yow will discover for creating a terrific pitch deck. A very good observe is to examine the pitch decks of leaders in your trade and study from them. An expert pitch deck has only a few slides, solutions three key questions (Why, What, How) about the issue and your answer, has all of the related KPIs, achievements, and tractions, exhibits your imaginative and prescient each short-term and long-term, and most significantly, explains why your group is superior and why it’s the precise group to do it.

Identical as every part in startups, the 80/20 rule ought to be adopted in fundraising too.

The 80/20 rule means that roughly 80% of your outcomes come from 20% of your efforts.

In every spherical, 80% of our effort and time ought to be centered on securing the precise lead investor. The lead investor is the investor who gives the most important quantity of funding in that funding spherical they usually normally take essentially the most energetic function when working with the startup. The lead investor is normally accountable for making ready time period sheets and authorized paperwork and conducting the due diligence as effectively.

Our main job is to search out the precise lead, the precise associate. When selecting a lead investor, ask your self these questions:

- Do you belief them?

- Are they a visionary mentor? Do you worth their mentorship and recommendation?

- Are they able to rising you to the subsequent stage? Might they allow you to within the subsequent spherical?

If the reply to all of those 3 is sure, that’s a terrific lead investor to have. Whereas our focus ought to be on discovering the precise lead, we must always open conversations with different buyers who may take part within the spherical as effectively. Allocating 20% of the time for these conversations is ideal.

Everybody prefers to work with somebody who’s knowledgeable of their subject. VCs love founders who know their shi* as effectively. They don’t like amateurs.

They anticipate founders to know the rules of working a startup and their market very effectively. They anticipate founders to know all their KPIs by coronary heart. They hate it when a founder doesn’t know their opponents. They hate it when founders brag about unimportant stuff or fallacious KPIs. They hate it once they have to elucidate to a founder fundamental startup phrases like ICP, USP, CAC, and so forth. These are all purple flags for a VC.

A professional founder just isn’t solely a professional in their very own subject, they’re a professional in working a enterprise. A professional founder analyzes and understands each single certainly one of their opponents, they usually have a plan for find out how to beat them. A professional founder has a transparent roadmap, is aware of the aim of elevating this spherical, and has chosen the precise milestones and KPIs.

A professional founder has a terrific response to those fundamental questions:

- Inform me about your market, how effectively do you perceive your opponents?

- What are you planning on doing with this funding? Why?

- Why are elevating proper now?

- What’s your subsequent objective? What’s your finish objective?

- What in the event you’re fallacious? What’s your plan b? What’s your plan c?

A professional founder is a trainer and a scholar on the similar time.

The most effective founders within the eyes of VCs, are those who themselves study from within the conferences. Visionary founders with a deep understanding of their enterprise and market whose perception is effective to any skilled.

Holding monitor of the entire conversations with buyers is admittedly essential as a result of they comprise incredible classes. Every dialog with a VC signifies that you and your startup will likely be challenged and we are able to study what’s fallacious with our enterprise and the way we are able to repair it.

80% of every assembly is VCs asking the identical questions, the FAQs. Whereas this makes assembly quantity 50 tremendous boring, it’s a possibility too. Ceaselessly requested questions are the areas during which our startup ought to shine. If we don’t have reply to those key questions, we must always change one thing in our enterprise, quick.

An ideal strategy to fundraising is to not begin it with the large names. As an alternative, we begin with smaller VCs. This manner we are able to observe pitching and turn into a professional at it. This manner we discover the actual points with our enterprise mannequin, our product, and our advertising. This manner we are able to repair all of those points and make our startup develop quicker.

Once we fastened the intense points with our enterprise, our pitch, our deck, and had a terrific reply to all of the ceaselessly requested questions by VCs, now it’s time to begin the dialogue with huge names. Now they see a rising startup with a terrific pitch, slam dunk.

Valuing an organization within the first years of its life just isn’t simple. In later phases, you may have actual monetary information, projections, and market information that can provide you a good valuation. However within the early phases, particularly pre-seed, it’s only a guessing sport.

A critical purple flag for buyers is when a startup overvalues itself. It’s an indication that the founders didn’t do their homework and haven’t any understanding of their market.

There are a few well-known strategies that each VCs and startups use for valuation within the early phases. One in every of them is the Berkus Methodology.

Berkus’s methodology of valuation was created to search out a place to begin valuation with out relying upon the founder’s monetary forecasts. The Berkus Methodology research 5 essential areas of a startup and signifies a worth starting from zero to $500,000 for every space:

One other widespread methodology is the Payne Scorecard methodology. This valuation methodology compares a startup to different typical startups on the similar stage, the same offers that occurred in that house. (buyers benchmark the “normal” worth of a pre-seed or early-seed firm on this case), inside a geographic area and their startup sector (SaaS, AI, digital well being, fintech, and so forth.).

For this methodology, researching related startups in related phases is important. The excellent news is these offers’ information are accessible publicly in companies like Cruchbase and CB Insights.

The unhealthy information is that not all of the buyers on the market are nice. In actual fact, most of them are unhealthy. Sadly, a big phase of buyers who name themselves VCs or angel buyers, don’t know the very first thing about startups, they’re simply right here as a result of they assume it’s simple cash or as a result of it simply sounds cool.

Most of these buyers are simply detectable from their portfolios. They normally haven’t any expertise working with actual, rising startups. They normally attempt to persuade founders with empty guarantees like discovering strategic companions or prospects for them. They normally brag about their connections as an alternative of their achievements.

That is much more widespread amongst many who name themselves angel buyers. As a rule of thumb, you don’t desire a wealthy angel investor who’s doing this as a hubby.

The most effective angel buyers are strategic angel buyers. Those which might be prime consultants in your subject and will be your mentor.

The most effective angel buyers are entrepreneurs themselves who grew their companies and may educate you find out how to develop as effectively. They’ve a vested curiosity in you and your enterprise, greater than the ROI alone.

Once you encounter a brand new investor, observe these steps:

- Test their portfolio, and see in the event that they’re focusing in your market and stage or not.

- Test their success tales. What number of of their portfolios grew to the subsequent stage, examine to see in the event that they participated within the subsequent phases or not.

- Discuss to a few founders of their portfolio, particularly those who grew to the subsequent stage. Ask how was their experiences working with them, in the event that they helped them within the subsequent spherical or not, how was their mentorship, and in the event that they micromanaged or not.

No have to be shy, founders love to assist one another and are more than pleased to share their suggestions.

That’s how we are able to see the potential of an investor. That’s how we are able to differentiate a terrific investor from the unhealthy ones.

There are three sorts of buyers: Nice ones, Mediocre ones, and Unhealthy ones.

Two of those will kill your startup.

I’ve seen many promising startups with nice groups wrestle to lift simply because they’ve raised from the fallacious folks earlier than and now, VCs are saying no to them simply because they don’t need to be on the identical cap desk as that different investor with a nasty status.

Elevating cash from the fallacious investor with a nasty status could make that startup un-investable. However, elevating cash from mediocre buyers just isn’t that totally different both.

Mediocre buyers are mediocre mentors at greatest. They do not convey actual worth to a enterprise. They can not assist a startup develop to the subsequent stage, they can not assist that a lot in later phases or subsequent rounds. All of those are far more essential than the cash itself.

Nice VCs like to work with different nice VCs. They don’t wish to spend money on startups which have raised cash from mediocre or unhealthy ones. That’s normally a purple flag for them.

Right now’s local weather could be very unforgiving for startups. In response to Carta, investments are down 50%–75% in 2023 in comparison with previous years, and on common, for startup, it’ll take round 10 months to lift their spherical. It was simply 4–5 months again in 2020, now startups need to be ready that their fundraising will take much more than a yr.

Again then, VCs pushed for one factor and one factor alone: Develop, irrespective of the price. Burning cash to attain was a token of satisfaction for a lot of founders and VCs even promoted this conduct. That’s not the case.

Now that the market is extra risky and VCs misplaced all their cash in loopy offers within the Covid period, they’re pushing startups to be extra steady, and fewer dangerous, even when which means much less development.

Sustainability now could be extra essential than development, as a result of VCs are indignant in any respect the nice startups they’ve invested in however at the moment are bankrupt as a result of they burned all their cash within the title of development.

The KPIs of every enterprise in every stage are totally different, however there’s one KPI that every one VCs worth greater than every other KPI within the startups at present with regards to fundraising and that’s Capital Effectivity.

Capital effectivity exhibits the VCs that the founders know find out how to run an actual enterprise. It exhibits not solely that they’re producing revenues, however they’re managing their bills as effectively they usually’re not performing like spoiled children. Nice VCs love founders who can construct a scaling, sustainable enterprise.

Listed here are among the most essential elements in a VC’s playbook:

- Capital effectivity (Being cashflow optimistic or in a position to survive and not using a elevate are huge benefits)

- Founding group benefit (Why this group, particularly, will win over their opponents, why this group is totally different)

- Development in revenues (Regular quantity month over month)

- Development in essential KPIs (Totally different for every startup however normally MAU, GMV, Utilization, and so forth.)

- Product/Market match rating

- A novel promising know-how, product, and/or IP

- Measurement of the market vs dimension of the competitors

Capital effectivity additionally helps founders elevate a greater spherical with higher phrases. I’ve seen many nice startups with nice concepts fail earlier than they might end their spherical as a result of they ran out of cash. Capital effectivity provides the startup choices.

VCs work on totally different timetables, some may provide the last sure or no in 2 days, and a few may take two weeks to determine to have one other name. Founders ought to discover all their choices on the similar time, ready just isn’t sport technique right here.

Nice VCs normally work very quick, in the event that they’re , they may get again to you instantly. However that’s not all the time the case and a few may shock you after some time. A very good trace when a terrific VC is keen on you is once they attempt to introduce you to different nice VCs. They need to get extra eyes on you, your product, and your deck. They need to get suggestions from different nice VCs about you, and presumably, lock of their co-investor within the spherical.

A very good observe is to maintain the dialog open with all of the events, the nice ones. Nothing is for certain till it’s. A number of offers that startups and VCs labored months on will fall by in the long run. By holding the dialog going, you’ll have choices and won’t waste time on just one VC.

When speaking to VCs, transparency is the important thing. VC world is a small world, all of them speak to one another, and most of the buyers you speak to will talk about your startup in personal between themselves. In the event that they ask you who’re speaking to, there’s an opportunity they already know. The extra data you share together with your potential buyers, the extra transparency you may have with them, the higher.

Elevating from the fallacious investor is likely one of the essential causes of demise in startups. You’re not solely elevating proper now, however you must also think about all the long run rounds as effectively. Particularly whenever you’re making an attempt to determine on the precise buyers and the share of the corporate you’re giving up.

A fallacious title in your cap desk (the listing of all of your shareholders and their ownerships) may equal to by no means elevating cash ever once more. The status of every investor, their monitor document, and their function in rising the corporate are the essential issues to concentrate to from the start.

Many startups fail or need to settle to promote their stake simply to do away with a partnership with a nasty investor, like what I needed to do again within the day. Accepting cash and signing a time period sheet is simple, going again after that’s arduous.

Nice VCs love startups which have clear, comprehensible cap tables. No mess, no surprises. Right here’s what a terrific cap desk seems to be like:

- Founders have divided their shares pretty.

There ought to be a cause why every co-founder has their share, and it can’t be as a result of we’re buddies or we began on the similar time. Every co-founder’s share ought to replicate their function within the startup, their experience, and their monitor document. - The founders didn’t lose an excessive amount of of their fairness in every stage.

On common, founders ought to give buyers lower than 10% within the pre-seed stage, lower than 20% within the seed stage, lower than 20% in collection A, and fewer than 15% afterward.

That is the common of the market, and every state of affairs will be totally different, however your numbers can’t be method off from these. Giving up an excessive amount of of the corporate early on is an enormous purple flag. - The startup raised solely once they have been imagined to.

Every spherical and every new investor has a objective. They didn’t have too many rounds. There are not any bridge rounds simply to decrease the chance. - There are not any names on the cap desk with unhealthy reputations.

- Ideally, there are not any advisory shares on the cap desk. If there’s, there ought to be cause for it.

- The cap desk on the post-money valuation remains to be thrilling sufficient for founders.

- There’s a steadiness between the important thing buyers, nobody has too many shares.

Cap desk ought to be protected in any respect prices, there is no such thing as a compromise ok that can justify making a messy cap desk. Future rounds are as essential as the present spherical, we must always all the time look out for the large image, for our imaginative and prescient.

{kind=link}