NooMUboN

Celsius Holdings (NASDAQ:CELH) is not a meme inventory, and any hype related to the model is warranted. CELH went from producing $52.6 million in income for his or her 2018 fiscal yr to delivering $1.15 billion in income over the trailing twelve months (TTM). CELH is clearly executing on its strategic plan, and the model has a lot momentum that PepsiCo (PEP) took a $550 million stake in CELH again in August of 2022. PepsiCo has extra data in regards to the beverage trade than most entities, and its distribution chain may also help CELH with its international growth targets. Brief curiosity has climbed to over 25%, and whereas the valuation could also be a bit too wealthy for my blood, I do not assume this can be a firm price shorting. CELH has large progress potential, and PepsiCo has a vested curiosity in CELH’s success. CELH is a type of shares that got here out of nowhere, and the individuals who did the homework and took the chance generated huge returns. Clearly, I want I acquired in earlier as CELH has completed nothing however gone up and to the suitable, however for now, I can be ready on the sidelines for a greater entry level.

Searching for Alpha

The Penny Inventory that took the market by storm

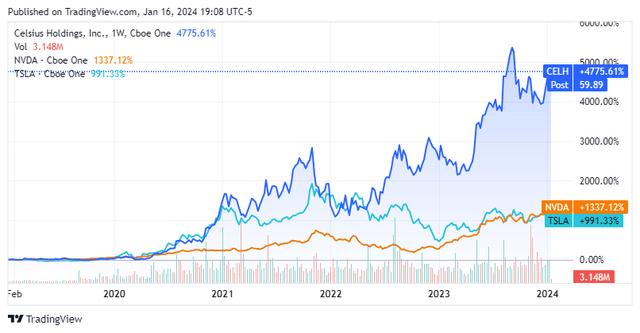

To be sincere, I’m not certain if I’ve seen this massive of a return from some other firm during the last 5-years or the previous decade. Relating to progress, I really feel like Nvidia (NVDA) and Tesla (TSLA) have a steady highlight shining on them, however the true story is CELH. Any CELH shareholder that has held for the previous 5 or 10 years, I simply wish to say congratulations as a result of this has been an absolute monster. Over the previous 5-years, TSLA has generated a 991.33% return, whereas NVDA has appreciated by 1,337.12%. These are unimaginable outcomes that shatter the appreciation from each the Invesco QQQ Belief ETF (QQQ) of 152.40% and the SPDR S&P 500 ETF Belief (SPY) because it returned 82.65%. CELH did not simply beat the market, it went into one other stratosphere in comparison with TSLA and NVDA, because it has appreciated by 4,775.61% over the previous 5 years. What could also be even crazier is that over the previous decade, shares of CELH are up 52,816.63%. On January 20th, 2014, shares of CELH traded for $0.11 and traded for beneath $1 till roughly January 9th, 2017.

CELH has taken the market by storm, and I can perceive why there are such a lot of bulls. CELH looks like it is simply getting began, and with PepsiCo behind them, there’s a sturdy alternative to broaden its footprint. What CELH has achieved is nothing wanting superb, contemplating they’re going head-to-head with established manufacturers, together with Purple Bull and Monster Vitality, and coming house with a chunk of the pie. Having the ability to generate YoY income progress for a decade is not a fluke, and now CELH is popping the web page on profitability. The actual query now could be, can the rally proceed?

Searching for Alpha

Why I feel Celsius Holdings has a vivid future

CELH is tackling the useful vitality drink and liquid complement classes in the US and internationally. Its core choices embrace pre and post-workout useful vitality drinks and protein bars. One of many huge differentiators between CELH and its rivals is that six self-funded research printed in varied journals, together with the Journal of the Worldwide Society of Sports activities Diet, the Journal of the American School of Diet, and the Journal of Energy and Conditioning Analysis, concluded {that a} single serving of CELSIUS burns 100-140 energy. That is completed by rising a shopper’s resting metabolism by a median of 12% whereas offering sustained vitality for as much as three hours. These research have additionally indicated {that a} single serving of CELSIUS previous to exercising could enhance cardiovascular well being and health and improve the lack of fats and achieve of muscle from train.

Celsius Holdings

The important thing differentiator between CELH and its main rivals is its concentrate on the health trade. On the finish of 2019, there have been an estimated 205,180 well being and health golf equipment worldwide, with roughly 184.59 million health club memberships. In 2024, the worldwide well being and health market is predicted to achieve $96.6 billion because it grows at roughly 7.7% on an annual foundation. The pre-workout complement market is valued at round 15 billion {dollars} and is predicted to almost double by 2028. A crucial side of the complement market is that 75% of Individuals take dietary supplements basically, with pre-workout dietary supplements being the preferred. CELH is focusing on a particular viewers relatively than attempting to compete in opposition to espresso and different merchandise that provide a caffeine increase. By engineering a drink that burns energy and physique fats, whereas offering an vitality increase and being supported by important nutritional vitamins, people who already take a pre-workout could also be inclined to modify to a can of Celsius. CELH can be tackling the post-workout aspect, and whereas it’s normal for people to have a protein shake after figuring out, Branched-chain amino acids (BCAAs) are important vitamins, together with leucine, isoleucine, and valine that stimulate the constructing of protein in muscle and probably scale back muscle breakdown. CELH has a full BCAA+ line that may be consumed throughout a exercise or as a post-workout restoration protocol. If CELH can convert a shopper on one finish, they are able to grow to be a part of somebody’s pre and post-workout routine.

Celsius Holdings

The take care of PepsiCo was large for CELH. On August 1st, 2022, CELH and PepsiCo entered into a number of agreements the place CELH issued 1,466,666 shares of Sequence A Convertible Most well-liked Inventory to PepsiCo for $550 million. The Transition Settlement specifies funds to be made by Pepsi to Celsius for transitioning sure current distribution rights to PepsiCo. The Distribution Settlement resulted in PepsiCo changing into the Firm’s major distribution provider for CELH merchandise in the US. After I have a look at what has occurred since this deal closed, it is actually compelling. CELH has generated $1.15 billion in income for the trailing twelve months (TTM), which is a further $49.9 million greater than their earlier three fiscal years mixed. In 2020, 2021, and 2022, CELH generated a mixed complete of $1.1 billion in income. There isn’t a query in my thoughts that PepsiCo’s distribution footprint performed a major position in CELH’s growth. The outcomes did not cease at income, CELH was capable of enhance its gross revenue by 101.51% to $545.9 million YoY and generate $155.5 million in web earnings in comparison with dropping -$187.3 million in 2022.

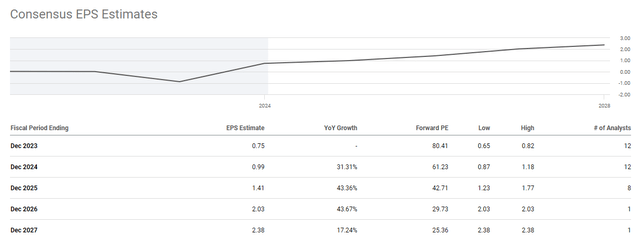

On Wednesday January 10th, CELH introduced that the model formally launched in Canada. Since PepsiCo has been a stakeholder, that is CELH’s first international growth endeavor. After I learn via the Q3 earnings name, administration particularly addressed that worldwide progress can be crucial for his or her progress story over the subsequent three years to 5 years. Administration indicated that they had been aiming to execute on a handful of nations in 2024 after which set their sights on extra international markets in 2025 and 2026. Customers vote with their wallets, and if CELH wasn’t making a great product, its gross sales progress would not be this strong. With PepsiCo behind them, I feel that CELH may have years of progress on the horizon as they proceed to broaden domestically and break into new international markets one by one. The analyst neighborhood appears to agree, as 12 analysts have a consensus EPS estimate of $0.99 in 2024, which might be a YoY progress charge of 31.31%. Searching to 2025, there are eight analysts which can be calling for $1.41 in EPS, which might be a further 43.36% of EPS progress in 2025. These numbers may truly be conservative if CELH can ship on its international growth objectives.

Searching for Alpha

Whereas I like all the things I’m seeing, I’m sitting on the sidelines due to the valuation

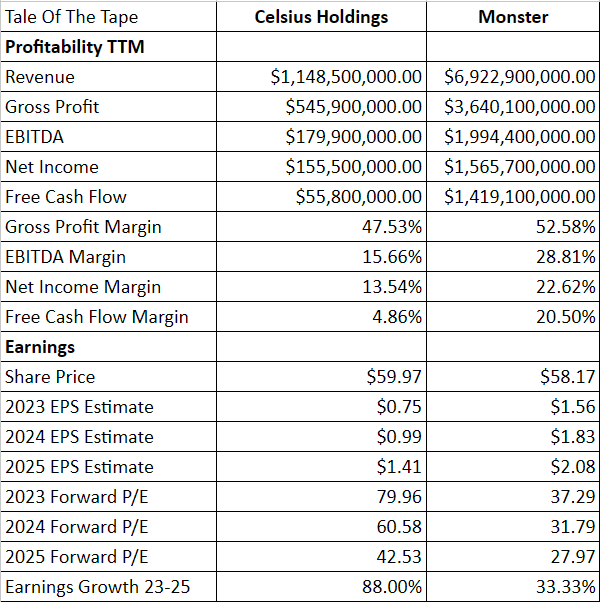

I would not guess in opposition to CELH as they’re delivering on their marketing strategy, however I can be ready for a greater entry level earlier than including them to my progress portfolio. After I evaluate CELH to Monster Beverage Company (MNST) it is onerous for me to justify including CELH at these ranges. MNST is producing $502.78% extra income ($5.77 billion), 566.81% extra gross revenue ($3.09 billion), 906.88% extra web earnings ($1.41 billion), and a couple of,443.19% extra free money circulate (FCF) ($1.36 billion) than CELH with higher margins. MNST is working at a 5.05% increased gross revenue margin, they’ve a 9.08% increased revenue margin, and a 15.64% bigger FCF yield on each greenback of income produced. After I have a look at the earnings progress, MNST continues to be rising at a double-digit charge YoY and trades at 31.79x 2024 earnings, and 27.97x 2025 earnings. CELH, alternatively, trades at 60.58x 2024 earnings and 42.53x 2025 earnings. I could also be incorrect, however I’m not keen to pay these valuations for CELH.

Steven Fiorillo, Searching for Alpha

The dangers of sitting on the sidelines

I may very well be 100% fallacious, and CELH drive extra EPS than anticipated over the subsequent yr by capitalizing on worldwide growth whereas taking extra market share domestically. PepsiCo is the ace within the gap, and so they have a vested financial curiosity in CELH’s success. It is totally potential that CELH can beat earnings estimates and trigger shares to proceed up and to the suitable. The opposite side is the quick curiosity. Greater than 25% of the shares are bought quick as a good portion of the funding neighborhood thinks shares are overvalued. If CELH has an impressive quarter or releases any kind of compelling information from a product line that opens up new markets or international growth forward of their earlier timeline, there may very well be a brief squeeze. I would not guess in opposition to CELH, and the chance for me is dropping out on upside appreciation. I by no means make investments due to the concern of lacking out (FOMO), and I feel there are different alternatives that I’m extra comfy with at this level.

Conclusion

CELH is now on my progress watchlist as this can be a firm I’m very excited by. CELH has a $14 billion market cap, and that is one thing that I may see PepsiCo buying sooner or later in the event that they assume it will likely be a robust asset to their portfolio. In 2020, PepsiCo acquired Rockstar Vitality for $3.85 billion, so this would not be their first enterprise into the area. CELH has a number of issues going for it as there’s double-digit progress in each EPS and income on the horizon for years to come back. They’ve proven they will ship on worldwide growth and have plans to enter extra markets over the subsequent a number of years, and so they have discovered a technique to differentiate themselves from the competitors. Customers are talking with their wallets, and PepsiCo owns a stake in CELH, making them have a vested curiosity in CELH’s success. Proper now, I’m staying on the sidelines, but when shares dump, I can be very excited by beginning a place.

{kind=link}