MoreISO/iStock Editorial by way of Getty Photographs

Compañía Cervecerías Unidas (NYSE:CCU) is a Chilean beverage firm. It is a market chief in its dwelling market and a challenger in quite a few different South American international locations. CCU produces and distributes market main manufacturers, has homeowners with deep pockets and a sturdy stability sheet.

The monetary efficiency of CCU is considerably in a turnaround place. The corporate remains to be pursuing to achieve pre-covid profitability degree after affected by a number of exterior components pressuring the financials. Its Q3 earnings declined as a result of change charges and one-time expense in its three way partnership. If exterior headwinds normalize, the inventory might simply commerce 25% greater.

Firm overview

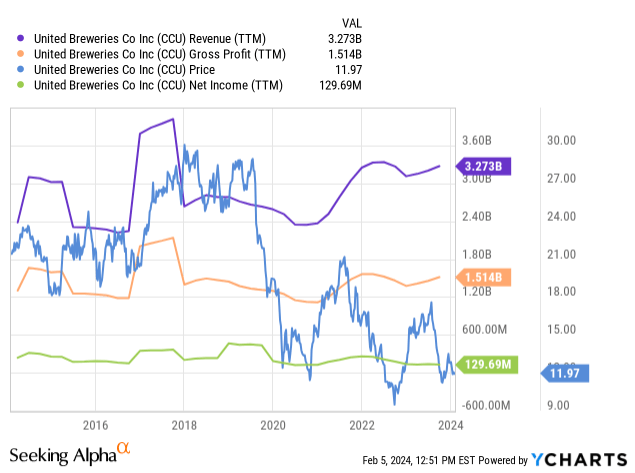

Compañía de las Cervecerías Unidas (CCU) is a Chilean producer, distributor and exporter of drinks. CCU was based in 1902 and its identify, United Breweries Firm, represents its historical past as a consolidator of the brewing market in Chile. In 2022 the corporate had revenues of $3.3 billion and employed 9400 individuals.

CCU has 4 working segments: Chile, Worldwide Enterprise, Wine and Joint Ventures and Related Firms. Its operations are reasonably complicated, however under follows a abstract for a ok understanding.

Chile. In its dwelling market CCU has numerous totally different operations. It’s a bottler and distributor of various merchandise of PepsiCo. It produces and/or distributes Schweppes, Pink Bull, Gatorade and totally different purified water manufacturers underneath a license from Nestle. CCU additionally produces alcoholic drinks in 5 totally different vegetation and distributes drinks of Pernod Ricard in Chile. Within the beer class CCU produces and distributes numerous manufacturers resembling Heineken, Sol and Coors.

Worldwide Enterprise. The worldwide working section consists of operations in Argentina, Uruguay, Paraguay and Bolivia. The section generates lower than 30% of the revenues however the share has been slowly rising.

In Argentina, with a inhabitants of 46 million, CCU is the producer and distributor of, for instance, Heineken, Amstel, Sol, Miller and Warsteiner beer manufacturers. Within the different international locations talked about above CCU additionally does enterprise with numerous native beer manufacturers and non-alcoholic drinks.

Wine. Wine working section is virtually 84.7% possession in an organization known as VSPT, which is without doubt one of the largest wine producers in Chile and among the many prime 20 on the earth. It has eight vineyards in Chile and Argentina. VSPT exports a bit of over 40% of its complete manufacturing quantity.

Joint Ventures and Related Firms. CCU has three joint ventures. In Chile it owns a 50% share of an organization that produces beer model Austral. In Colombia it additionally operates in an equal three way partnership that produces and distributes a number of the nation’s hottest beer manufacturers (Tecate, Andina, Sol) and worldwide beers resembling Heineken and Coors Lite. In Argentina CCU has an equal three way partnership with Danone within the bottled water enterprise.

Gross sales and working outcomes of the segments. (CCU)

A powerful firm dealing with exterior headwinds

A market chief with a strong stability sheet

CCU is a market chief in its dwelling market, Chile. When it comes to quantity its market share was 45.2% in 2022 and its place has remained secure over the previous three years however rising 1-2 share factors from 2017-2019 ranges. In Chile the corporate claims to have a market main place in all of its classes besides in smooth drinks and ciders. Within the worldwide markets it is sometimes a challenger.

Market place of CCU. (CCU)

The draw back of the market management is that firm’s revenues fluctuate along with consumption patterns. In Q3 outcomes mentioned in November the administration referred to the weak consumption in Chile, volumes lowering 4.7% however compensated by over 10% worth improve. Within the worldwide working section volumes decreased by 4.3% and common worth elevated by 2%. Within the wine working section the volumes decreased by over 17% with out a lot assist from pricing. Throughout YTD Q3 the quantity growth is fortunately on a greater degree declining just one.7%.

Key figures Q3 2023. (CCU)

Right here, the quantity lower is considerably defined by greater than regular volumes within the comparability interval and the unfavorable climate. Due to this fact the administration doesn’t see a decline in market share. The long-term quantity development has averaged roughly 4% over the previous 20 years in Chile and its worldwide markets.

CCU has a strong stability sheet with a leverage of 2x on internet debt to EBITDA foundation. The leverage ratio barely decreased all through the primary 9 quarters of 2023. 65% of its debt expires after 2027. A big a part of the debt is tied to USD or euro, which is a adverse as its important currencies have been depreciated through the years.

CCU’s debt place. (CCU)

65.9% of CCU is owned by Quinenco and Heineken collectively. Quinenco is an funding firm of the fourth richest household in Chile. Their investments span from cable manufacturing to banking. The remainder of the inventory is floated in NYSE as an ADR (20.6%) and in Bolsa Santiago (13.5%). Whereas there’s no purpose to imagine that almost all homeowners could be promoting the corporate, it’s good that there’s a secure proprietor within the firm.

Additionally, the possession of Heineken reduces the danger of shedding the correct to provide and distribute manufacturers of Heineken. Then again, the presence of Heineken might cut back the quantity of potential alternatives and partnerships with different firms. Though it already has partnerships with Coors, Nestle, PepsiCo, Pink Bull and Pernod Ricard amongst others.

CCU has been pressured by exterior components

As a beverage producer CCU has suffered from the value will increase of uncooked supplies resembling sugar, orange juice, aluminum and malt. Though the costs stay greater than typical historic ranges, the costs have come down and CCU is beginning to face comparability durations the place the uncooked materials costs have been greater. CCU has successfully compensated uncooked materials inflation with worth will increase.

CCU is presently operating a program to get better its profitability again to pre-pandemic ranges. The administration remains to be calling for stronger efforts sooner or later however has highlighted the optimistic influence of this system on operational efficiency , as seen within the figures offered within the following part. This system isn’t solely about effectivity but in addition about sustaining scale. As part of this system CCU has invested reasonably closely into advertising as a way to construct its model fairness and drive demand.

One of many main dangers, and a chance, is the Chilean peso. At the moment the peso is buying and selling at the long run lows in relation to the U.S. greenback or with a greenback one can get an virtually a document quantity of pesos. The forex has developed in opposition to an investor investing {dollars} for over a decade. A turnaround within the change fee would work within the favor of overseas investor.

USD to Chilean peso. (Google)

The image is comparable for Argentine peso, which the administration commented in a following method within the Q3 earnings launch, emphasis by the writer:

The discount of internet earnings was largely defined by two results in Argentina: (i) the next loss in Overseas forex change variations by CLP 8,8183 million from the sharp devaluation of the ARS through the quarter, and (ii) CLP 8,6653 million of non-recurring bills associated with the route-to-market integration of our JV in Argentina with Aguas Danone into our operation. Isolating the aforementioned results, Web earnings would have elevated 25.3%.

The inventory is probably going buying and selling at its truthful worth

CCU has a lovely historic development profile. Its annual gross sales and internet earnings development have averaged near 11% and 9% over the previous 20 years.

Lengthy-term efficiency. (CCU)

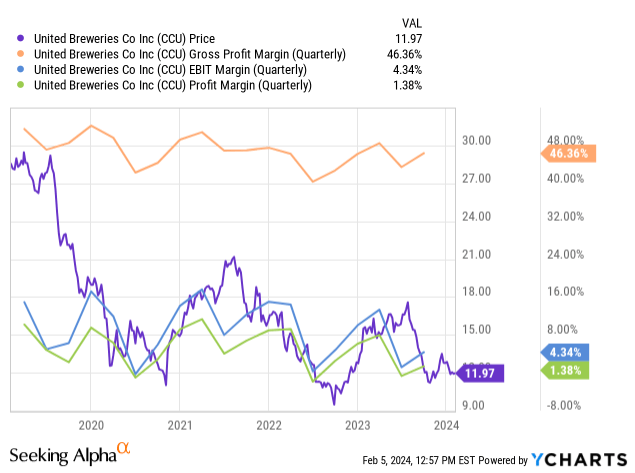

Nevertheless, the current monetary efficiency is reasonably cloudy and inconsistent. In Q3 CCU’s internet earnings decreased by 35% resulting from overseas forex change charges and losses from joint ventures offset by decrease monetary bills and better gross revenue. Therefore, EBIT elevated by 52%. In Q3 YTD its income elevated by 2.6%, EBIT 22.1% however the EPS decreased by 10.4% as a result of similar causes as in Q3.

Monetary figures for Q3 YTD 2023. (CCU)

Within the case of CCU, a situation evaluation offers a degree of understanding of the truthful worth.

The analysts predict CCU to ship an EPS of $0.92 for 2023 and speedy development after that. Nevertheless, by the tip of the third quarter CCU had produced earnings per share of roughly $0.37. Within the This fall CCU has sometimes delivered an EPS of roughly $0.2 to $0.22. Due to this fact, one potential situation is that 2023 annual earnings are available someplace between $0.5 to $0.6. That’s our bear case, which assumes that earnings get better a bit sooner than in additional optimistic outcomes for 2023.

Earnings estimates. (In search of Alpha)

In a base case we merely estimate that the 2023 earnings are available 15% decrease than the analyst estimates, at $0.78. Within the base case we additionally assume a bit of bit slower earnings development than within the bull case. Within the bull case we merely assume that CCU meets the common analyst estimate for 2023.

In response to In search of Alpha, the 5 12 months common P/E-multiple is 17-18. Due to this fact the estimation right here has a degree of security margin with decrease multiples and development in comparison with historic ranges.

By making use of a forty five% chance for the bottom case, 35% for the bull case (contemplating it’s an analyst common) and 20% for the bear case we arrive at a good worth of $12.3 per share. If the exterior components fade away and if CCU meets or exceeds analyst estimates for 2023, there’s possible an enormous upside for the inventory. With 12% low cost fee the truthful worth could be $10.8.

The typical goal worth for CCU is $15 per share starting from as little as $6.6 to as excessive as $21.

Completely different eventualities to estimate truthful worth. (Writer)

CCU’s relative valuation is reasonably enticing. Listed within the American exchanges there are just a few related friends and rivals of CCU. Chilean Embotelladora Andina is a bottler for Coca-Cola in quite a few South American international locations. Coca-Cola Femsa (KOF) can be a bottler for Coca-Cola in Mexico and Central and South America.

Additionally, the most important Chilean producer of wines and a producer and importer of beers, Viña Concha y Toro, is listed on the Santiago inventory change. Its current monetary efficiency doesn’t appear to justify a valuation premium compared to CCU. Heineken is one other attention-grabbing comparability. Taking a look at margins, development and returns on capital, Heineken’s degree of efficiency doesn’t appear to justify such a big valuation premium.

In Europe there are additionally loads of related listed friends with their very own manufacturing and distribution companies. CCU might be in comparison with the Irish C&C Group, Polish Ambra or Nordic Anora Group, one more turnaround inventory. From this group, Ambra, which doesn’t produce beer, can be a comparatively good firm with an inexpensive inventory.

Valuation multiples for chosen friends and rivals. (Tikr)

CCU isn’t the most affordable inventory within the chosen group of friends. On EV/EBITDA foundation Embotelladora Andina is the most affordable and has greater EBIT-margin and return on capital and good historic development profile. Nevertheless, traditionally Embotelladora Andina has traded at a decrease a number of than CCU.

What we are able to see right here is that CCU isn’t buying and selling at a premium valuation, however on a reduction at virtually all multiples – whereas its monetary metrics are sometimes at a comparable degree. As soon as the headwinds settle down, anticipating a P/E-multiple of 12-15 isn’t an excessive amount of of a stretch.

Variable dividend gives small cushion

CCU doesn’t have a constant dividend historical past. Its dividend coverage is to distribute 50% of the annual internet earnings as dividends. Because of the dividend coverage and ranging change fee the annual quantity of dividend in greenback phrases is unstable. In 2023 CCU paid a complete dividend of $0.26 per share leading to a dividend yield of two.2% on the present share worth of $12.

If CCU would meet the analyst expectations of $0.92 EPS for 2023, the dividend might theoretically be $0.46 leading to a dividend yield of three.8%. Traditionally the dividend has been effectively lined by the EPS and money circulation per share.

Growth of EPS, dividend and money circulation per share. (Tikr)

Conclusion

CCU’s assortment of premium worldwide manufacturers and native champions makes it an attention-grabbing inventory to get publicity to South America. CCU is a powerful firm in the midst of a number of exterior headwinds. It is valuation is modest contemplating the headwinds and low in the event that they dissipate within the close to future. Contemplating the historic development profile, reasonably wholesome stability sheet and resilient business, CCU is a worthy addition to earnings looking for portfolio with a stable potential upside.

{kind=link}