Ultima_Gaina/iStock through Getty Photos

Background:

Spectra7 (OTCQB:SPVNF) is a micro-cap firm traded on the OTCQB underneath the image SPVNF and on the TSX, Toronto Inventory Change underneath the image SEV. They’re primarily based in San Jose, CA.

Spectra7 is a fabless semiconductor firm specializing in silicon chips embedded within the connectors of normal copper cables. These chips amplify and situation knowledge transmission indicators. By bettering the sign, knowledge will be reliably transmitted utilizing longer and thinner copper cables. These cables, known as Lively Copper Cables or ACC for brief, current a worth proposition for knowledge facilities, VR headsets, and the automotive business. AI factories use as much as 3 times the variety of cables than in a typical knowledge middle. AI facilities are a goal marketplace for Spectra7.

What Spectra7 does (Spectra7 web site)

Funding thesis:

Spectra7 is within the enviable place of being first to market with ACC, and at present, they’ve few direct rivals. They’ve 55 patents that present a stage of safety for his or her options. ACC’s candy spot is for techniques that require 800Gbits/second interconnects with distances over 1 meter and underneath 7 meters. Traditionally, passive copper cables have been used for brief distances and optical cables for longer interconnections. Spectra7’s know-how extends the vary of passive copper cables and is considerably inexpensive than an optical cable resolution.

Spectra7 has gross sales within the knowledge middle market, a significant Japanese car producer, and Sony to be used of their PlayStation VR headset. It’s necessary to notice that these clients have confirmed the necessity for and the viability of the Spectra7 resolution.

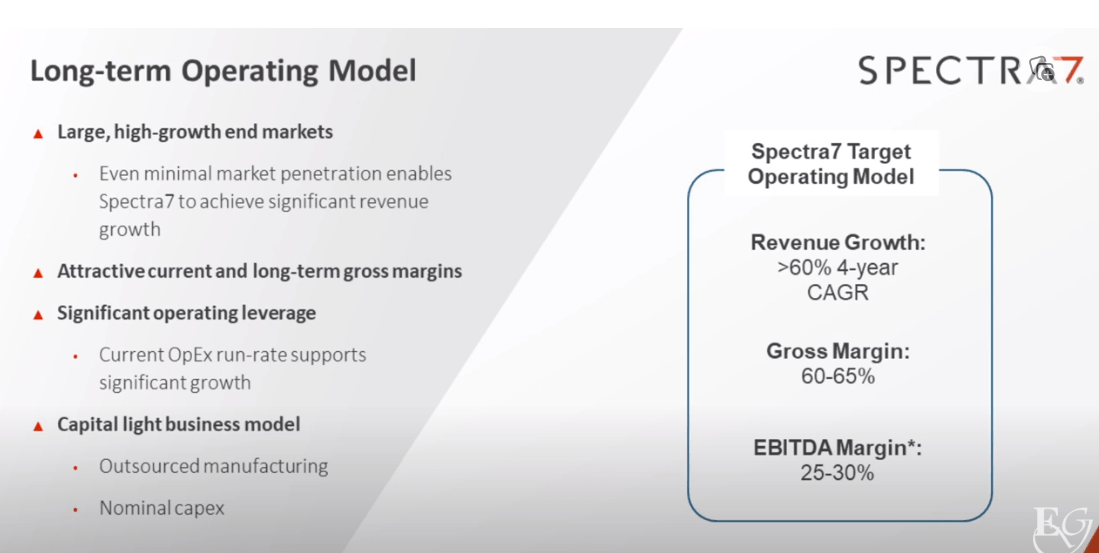

Their enterprise mannequin forecasts a CAGR of 60% for a number of years. They’re forecasting GMs of as much as 65% and internet of 25 to 30%.

Spectra7’s working mannequin (Spectra7 web site)

When energetic copper cables are used as an alternative of optical cables, they’re ½ the worth and use as much as 1/tenth the ability. The client saves with the upfront buy and has a decrease value of possession by utilizing much less electrical energy. As a result of they use much less energy, their resolution produces much less warmth and makes use of much less air con, which is one other value financial savings. A single knowledge middle can use lots of of hundreds of cables, so the financial savings are substantial. Spectra7 expects knowledge facilities to understand as much as $17M in yearly financial savings utilizing their ACCs.

There may be a longtime pattern in knowledge facilities, particularly for AI, that knowledge charges are rising. Because the charges go up, Spectra7’s options change into extra worthwhile, and their ASPs go up. At 800Gbits/sec, 100Gbits per lane at eight lanes, it isn’t sensible to make use of a typical copper cable for greater than a meter, and optical cables, whereas nice for lengthy distances, are costly and power-hungry. The ACC gives an economical, lower-power resolution for one to seven-meter cables.

At a latest investor presentation, the CEO said that if a buyer begins deploying ACCs, Spectra7 can anticipate as much as 5 to 10 years of steady gross sales. I view this as a type of recurring income.

Spectra is forecasting the ramp for his or her merchandise to begin in the midst of 2024 and presumably sooner. Whereas Spectra7 has didn’t ship on earlier steerage, I think about their anticipated ramp due to latest bulletins from DesignCon and their announcement about their first manufacturing contract that I’ve listed under. As well as, administration’s expectations for the ramp are tied to the following Broadcom Tomahawk launch. These chips function at 800Gbits/second and 1.6Tbits/second, Spectra7’s candy spot, and might be put in in switches from a number of producers that Spectra7 cables will join.

After listening to Spectra7’s newest company presentation and speaking on to administration, I’m satisfied that the market is prepared for Spectra7’s resolution, and the ramp will happen shortly.

If I take a look at their present yearly income of over $9,700,000 a yr, the corporate isn’t worthwhile or an thrilling inventory. The thrill is sooner or later, significantly within the AI knowledge middle market.

Tencent, an enormous, multinational knowledge middle supplier slated to be the biggest in China, is listed on Spectra7’s company presentation as a blue-chip accomplice. On the Rising Progress Convention in December, Raouf Halim, CEO, defined how Tencent is a vital current buyer. Tencent makes use of Spectra7’s chips in ACC cables of their knowledge facilities for 50Gb/second options per lane.

Present gross sales to Tencent are low, because the market and gross sales of Spectra’s resolution for 50Gb/second are restricted as knowledge facilities are deploying higher-speed interconnects. Gross sales are anticipated to extend when new switches with the brand new Broadcom Tomahawk are deployed, operating at 100Gb/second at eight lanes. 800Gbits/second is Spectra7’s candy spot, the place they carry essentially the most worth to the shopper and have the best ASP. This chance is anticipated to ramp up in Q2 or presumably sooner.

Spectra7 has said of their newest presentation that they’re engaged closely with Alphabet (GOOG), Apple (AAPL), AWS (AMZN), Meta (META), and Microsoft Azure (MSFT). Clearly, from Spectra7 numbers, these potential clients have but to ramp or contribute any substantial income.

Clients that Spectra7 is engaged with. (Spectra7’s web site)

A serious car producer in Japan is utilizing Spectra7’s know-how. The worth proposition for the automotive market is the Spectra7 cables are lighter and extra versatile. That is their preliminary foray into the automotive market. At the moment, this isn’t a major contributor to their income. Time will inform in the event that they acquire traction on this market.

In addition they have a 5G design win from a major US provider, however little is anticipated from this market as they often require longer cables.

Spectra 7’s chips are used within the Digital Actuality Market, particularly with Sony (SONY) on the PlayStation Digital Actuality Headset. This can be a very good win for Spectra7 and gives ongoing income. Spectra7 might see extra gross sales on this market to different VR producers. Their major competitors for Spectra7 in headsets is wi-fi, however wi-fi doesn’t have the bandwidth of the tethered resolution, and due to this fact, the shopper expertise isn’t nearly as good.

Spectra7 additionally providers the HDMI market, the place their gross sales are minor, and I anticipate little development.

Spectra7 is projecting a four-year 60% compounded annual development fee. To give you a worth goal, I might be conservative with Spectra7’s projections and apply a 50% development fee for the following three years. Spectra7’s anticipated income for the trailing 12 months is $9,700,000 for the complete yr.

If Spectra7 achieves a 50% yearly development fee, revenues might presumably attain greater than $30,000,000 in income in 2026. If I apply a P/S ratio of 4, which I consider is sensible given the expansion fee, I get a market cap of roughly $130,950,000, up from the present market cap of roughly $26,000,000. With 40,440,000 shares excellent and a possible $130,950,000 market cap, I get a share worth of $3.24.

Spectra7 is projecting an EBITDA of 25 to 30%. This can take a while, particularly given their disastrous 4th quarter. If they will obtain 10% internet revenue after taxes in three years, I consider that is achievable given they’re a fabless chip producer; I get a backside line of $3,273,750. With 40,440,000 shares excellent, I get an EPS of $.081. If we apply a 25 P/E ratio, it ought to be a lot larger with that development fee; we get a $2.03 share worth.

Even with my fashions exhibiting a goal of $2.03 to $3.24, I do not need to get forward of my skis, and I’m beginning with a purchase ranking and a $1.25 worth goal. I’ll replace my goal if and after I see progress within the ramp.

A disastrous 4th quarter:

Spectra7 has pre-announced a disastrous 4th quarter with anticipated income of solely $100,000.00. Whereas Spectra7 put a constructive spin on the income expectations, this announcement despatched shares to a low of $.2446 on January eleventh. Nonetheless, the shares have recovered properly attributable to a number of constructive bulletins I listed under.

At DesignCon 2024, Spectra7 demonstrated that their chips embedded within the cables from the next corporations labored with the sign testers from the below-listed corporations:

- ACC Cable Corporations:

- ACES Electronics Co., Ltd (“ACES”), a number one Taiwan-based connector and cable provider.

- Volex plc (“Volex“), a worldwide chief in high-speed knowledge middle interconnect merchandise.

- Take a look at Gear Corporations:

On January sixteenth, Spectra7 introduced that it had obtained its first manufacturing order for its GaugeChanger chips from a significant Chinese language cable provider that providers Hyperscalers in China and North America. After these bulletins, the shares began to pattern upward.

The demonstrations and the manufacturing order have taken important dangers out of the equation, because the product is confirmed to work, and there’s a viable marketplace for their merchandise.

The issue:

Optical cables are costly and power-hungry. Copper cables are low cost however are overly thick and stiff, they usually have points with larger bandwidth indicators, longer lengths, and sign integrity. At 800Gps, the copper cables is perhaps efficient as much as 1.5 meters lengthy earlier than they expertise sign integrity issues. Optical cables will be kilometers lengthy however are expensive and use considerably extra energy.

The Resolution:

For lengths higher than 1 to 1.5 Meters however lower than 7 meters, energetic cables with Spectra7’s embedded chip prolong the size of passive copper cables and are considerably inexpensive than an optical resolution.

Spectra7’s know-how (Spectra7’s web site)

Enterprise mannequin:

Spectra7 is a fabless semiconductor firm producing chips however doesn’t promote cables. Their chips are purchased by cable corporations like Molex and Amphenol, who combine them into their copper cables’ connectors. Molex and Amphenol have established relationships with the information facilities and are an extension of Spectra7’s salesforce.

Competitors:

At the moment, the corporate claims that they’ve restricted direct rivals. A division of MA/COM has an ACC resolution, however Spectra7’s administration doesn’t consider they’ve gained broad traction within the market.

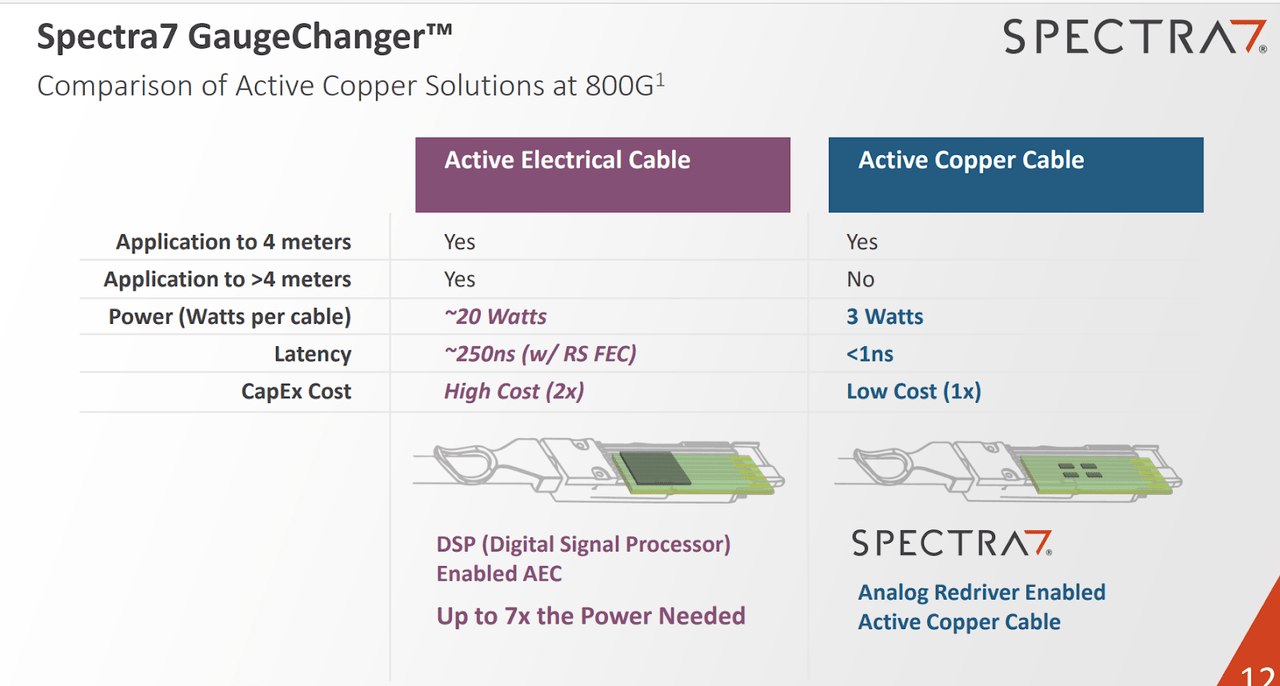

A number of corporations that make Lively Electrical Cables, AEC, or Good Cables are gaining acceptance within the market and are rivals to Spectra7. Their options are just like the ACC, however they use Digital Sign Processing, DSP, with re-timers, they usually create a cleaner sign, eradicating noise and amplifying the sign. They’re costlier and use extra energy.

The AECs could carry out higher than ACCs in compatibility between completely different techniques. Producers of servers and switches can use completely different chips, which could not be appropriate.

The Lively Electrical Cables have gearbox options, which, for instance, can permit ten lanes at 10Gbits to be appropriate with 4 lanes at 25Gbits/second. Their DSP and re-timer know-how permits for higher compatibility with swap and server producers.

Corporations need to be sure that every little thing is 100% appropriate, so AECs have a aggressive benefit. Nonetheless, corporations like Tencent design their servers and switches for end-to-end compatibility, which is why they like the inexpensive and lower-power resolution from Spectra7.

A number of corporations produce the AECs. One such firm is Astera Labs with the Taurus Ethernet Good Cable. This cable is just 3 meters in distance, whereas different AECs have longer attain. The latency operation is < 100ns, considerably higher than Spectra7’s resolution. That is important since every little thing about AI and 800Gbits/second transmission is about pace. The Good Cable has superior safety features, which I don’t perceive. Why would somebody put safety features in a cable? Perhaps somebody studying this text can enlighten me.

One other AEC firm is Credo, which makes the HiWire.

Under is a slide from Spectra7’s company presentation that depicts the ACC and AEC variations in worth, energy, latency, and attain.

Lively Electrical vs. Lively Copper (Spectra7 web site)

There’s a large enough marketplace for each ACC and AEC cables, and the adoption of both ought to assist the opposite.

Spectra7 was first available on the market, they usually have skilled gross sales cycles of as much as 4 years in size. The purchasers evaluated their merchandise extensively, as knowledge facilities don’t tolerate sign integrity issues. COVID and provide chain points additionally slowed acceptance. The rigorous evaluations and lengthy gross sales cycle ought to present a head begin for Spectra7. Nonetheless, since Spectra7 proved the viability of ACCs, and with COVID delays a factor of the previous, I don’t anticipate rivals might be required to undergo as lengthy and demanding evaluations.

Market Analysis

Here’s a hyperlink to an unbiased market analysis white paper on ACC. The paper has a constructive outlook for ACC and states, “Spectra7 pioneered this know-how and was the primary to deploy it at a significant Hyperscaler (Tencent in China).”

Dangers:

The inventory isn’t listed on the Nasdaq or Dow change, as it’s on the Toronto Inventory Change TSX and the Enterprise Market, OTCQB.

The inventory is illiquid, and the bid and ask costs will be huge sufficient to drive a truck by means of. DO NOT PLACE A MARKET ORDER WHEN BUYING OR SELLING SHARES. ALWAYS USE A LIMIT ORDER.

Probably the most important threat is that somebody infringes on their patents and creates a copycat product.

The rivals listed above, with higher sources, might scale back the worth of their options.

There are not any analysts listed on Yahoo that cowl Spectra7.

The ramp has taken for much longer than anticipated, and there’s no assurance that it’ll occur.

I had hassle discovering ACCs on the Molex and Amphenol web sites. Amphenol had a number of ACCs in inventory, but it surely was famous that one ACC cable was discontinued. I requested Spectra’s administration about this, however they have been unaware that Amphenol had discontinued a cable.

Molex and Amphenol web sites have extra details about AECs than ACCs. It seems that AECs are gaining traction quicker than the ACCs. This is smart since Molex and Amphenol do not need management over incompatible techniques and switches. This isn’t a problem for corporations like Tencent, as they management each ends of the cable.

Whereas the stability sheet appears stable, a further increase is feasible and possible in the event that they get a major order and want capital to buy stock. That might be downside to have.

ACC is a brand new know-how that has but to achieve widespread acceptance. Whereas Spectra7 is the pioneer on this new discipline, it has taken for much longer to be adopted than anticipated. I’ve owned shares for a few years and have unrealized losses. I’m nonetheless ready for the inflection level to happen. On the constructive facet, Spectra7 claims that they’ve been perfecting their merchandise with a number of iterations of their know-how which were examined and certified by main cloud corporations. Consequently, they declare that they’re considerably forward of their rivals.

The Ethernet Alliance just lately sponsored a Greater Pace Networking Plugfest, the place corporations have been invited to check the compatibility of their merchandise. Spectra7 was very profitable with compatibility of 5 out of seven distributors. This takes appreciable threat out of the equation.

Conclusion:

This can be a speculative inventory. Nonetheless, the worth proposition for Spectra7’s clients is just too nice to disregard. It makes good sense that their clients need to undertake and deploy their resolution at scale. Their options have been confirmed and deployed. I consider it’s only a matter of time earlier than we see a major ramp.

The corporate has 13% insider possession, so the administration has their cash the place their mouth is, and there may be loads of incentive for the corporate to achieve success.

Spectra7 mannequin predicts a 60% CAGR and as much as 65% GMs. The present worth of round $.64 a share is engaging, particularly for a corporation that expects to develop at a 60% CAGR. With their current gross sales and an thrilling future, I anticipate the draw back to be restricted. I anticipate important upside potential if the ramp performs as anticipated.

Please do your due diligence, as this can be a speculative play.

Editor’s Be aware: This text discusses a number of securities that don’t commerce on a significant U.S. change. Please pay attention to the dangers related to these shares.

{kind=link}