AutumnSkyPhotography

QUALCOMM (NASDAQ:QCOM) has rallied 21% for the reason that final article was printed (which will be discovered right here).

The corporate has printed their FY1Q24 outcomes, and this text will cowl my ideas on the earnings.

This was a powerful print as high and bottom-line exceeded the excessive finish of the steering and expectations.

The sturdy outcomes confirmed an enchancment within the handset cycle, with demand stabilizing and the corporate being extra optimistic about the place we’re at within the handset cycle.

Aside from the handset section, automotive additionally was sturdy, whereas administration expects this FY1Q24 quarter to be the underside for revenues for the IoT section.

Final however not the least, Qualcomm is displaying its upside in generative AI as AI pushes to the sting to allow on-device AI, and there may be additionally a PC alternative that could possibly be large just a few years from as we speak.

FY1Q24

Qualcomm generated $9.92 billion in revenues for FY1Q24, up 15% sequentially. This was 4 proportion factors larger than consensus.

The beat was a results of the upper handset and automotive chip gross sales.

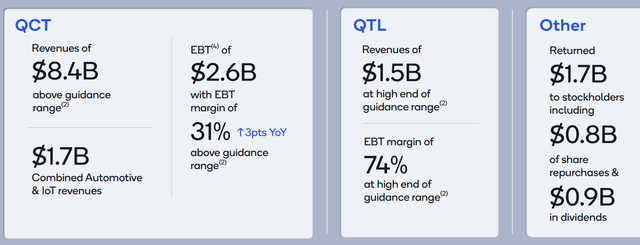

I’ll first contact on the QCT section earlier than delving into the QTL section under. QCT revenues got here in at $8.4 billion and EBT margin of 31% was delivered. Each got here in above the excessive finish of the steering vary, once more because of power in each handsets and automotive revenues.

QCT margin was a results of enchancment in income scale, higher product combine and continued working self-discipline.

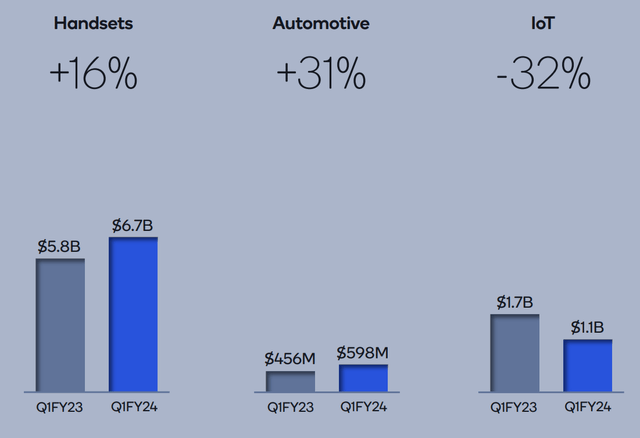

Handset revenues grew 16% from the prior yr to $6.7 billion. This was larger than administration’s personal expectations on account of larger demand because of the acceleration of Android flagship launches with the Snapdragon 8 Gen 3 cellular platform. Specifically, Android handset revenues from Chinese language OEMs exceeded administration’s expectations, rising greater than 35% from the prior quarter.

Automotive revenues had been additionally sturdy, rising 12% sequentially to $598 million, which was a results of elevated content material in new car launches with the Snapdragon digital chassis platform. IoT revenues of $1.1 billion mirror the industry-wide challenges we have beforehand outlined. We achieved report automotive revenues of $598 million, which grew by 12% sequentially,

Breakdown of QCT revenues (Qualcomm)

QTL revenues got here in at $1.5 billion and EBT margin of 74% was on the excessive finish of steering. Once more, this mirrored the marginally larger handset models.

For the QTL enterprise, Qualcomm additionally introduced a number of key license agreements extensions.

Firstly, Apple exercised its 2-year extension on its licensing settlement because of its prolonged reliance on Qualcomm modems. This takes the licensing settlement with Apple to march of 2027.

As well as, administration shared that Qualcomm additionally prolonged long-term agreements with two vital Chinese language smartphone OEMs.

Qualcomm continues to barter new agreements and renewals with new or current clients, with some expiring in early fiscal 2025.

QCT and QTL income breakdown (Qualcomm)

Gross margins got here in at 56.9%,up 139 foundation factors sequentially. This was 1 entire proportion level larger than consensus estimates.

EPS got here in at $2.33, 19% larger than market consensus, on account of the beat in gross margins and decrease taxes.

Nevertheless, steering got here in lighter than anticipated.

For FY2Q24, Qualcomm guided for revenues to be at $9.3 billion, which is down 6% sequentially, on account of share loss at Samsung. This was about 2% under consensus.

FY2Q24 EPS was guided to $1.79, 10% under market consensus, on account of decrease licensing income.

Throughout the quarter, Qualcomm continued returning worth to shareholders, $1.7 billion was returned to shareholders, $895 million within the type of dividends and $784 million within the type of share repurchases.

Samsung and generative AI

In FY1Q24, Qualcomm additionally introduced the Snapdragon 8 Gen 3 cellular platform, which brings generative AI capabilities to the top-tier Android smartphones and the efficiency and experiences it brings places the Snapdragon 8 Gen 3 cellular platform a class chief.

Importantly, the Snapdragon 8 Gen 3 cellular platform for Galaxy was featured within the Samsung Galaxy S24 Extremely, which was just lately introduced, together with the Galaxy S24 and S24 Plus.

This permits the Galaxy S24 Sequence to allow on-device AI options like dwell translate, chat help and extra.

I believe the adoption by Samsung of the Snapdragon 8 Gen 3 cellular platform for generative AI alternatives could lead on different smartphone gamers to begin incorporating it into their smartphones as effectively to match the person expertise and efficiency of the Galaxy S24 Sequence.

Qualcomm introduced that it has prolonged a multi-year settlement with Samsung. This settlement pertains to Snapdragon platforms for flagship Galaxy smartphone launches from 2024.

With this extension of a multi-year settlement with Samsung, I believe this exhibits the sturdy technological management of Qualcomm’s Snapdragon 8 and the worth of a long-term strategic partnership with Samsung.

With this settlement, Qualcomm continues to have a majority share place with Samsung, which is someplace within the 80% vary, down from the sooner 100%.

Steerage for international handset models

Qualcomm commented that they anticipate international handset models to fall mid-single digit proportion within the 2023 calendar yr, on a year-on-year foundation. Once more, that is an enchancment from the sooner down mid-to-high single-digit proportion relative to 2022 within the prior quarter.

It is a results of the latest stabilization of demand.

For the 2024 calendar yr, administration expects international handset models will likely be flat to barely up from 2023. Of which, 5G handsets are anticipated to develop high-single digit to low double-digit proportion.

For the June quarter, whereas Qualcomm shouldn’t be but guiding that far forward, administration suggests nothing out of the bizarre.

Diversification thesis continues

One of many key pillars to the funding thesis surrounding Qualcomm is the technology of latest sources of revenues from automotive and IoT.

Automotive is a crucial progress pillar and has achieved effectively but once more this quarter.

In 2023, administration shared that 75 new fashions had been launched commercially with the Snapdragon Digital Chassis Resolution.

It is a substantial variety of fashions for an rising and rising enterprise and thus, additional validates my thesis that Qualcomm continues to be rising in scale within the automotive section and administration is executing the design wins effectively.

Qualcomm additionally introduced that it’s collaborating with Bosch, for Bosch to make use of the Snapdragon Experience Flex system-on-chip (“SoC”) to energy their new central car laptop.

Qualcomm’s Snapdragon Experience Flex SoC permits for the combining of infotainment in ADAS functionalities on a single SoC.

Lastly, Qualcomm shared that it demonstrated digital cockpits linked companies and superior driver methods enabled by generative AI fashions working regionally on the Snapdragon platform. This could merely be enabled by way of a software program improve and presents new alternatives for Qualcomm.

Throughout the IoT section, the buyer a part of it’s seeing some type of stabilization after Qualcomm known as out the weak spot earlier in 2023. That stated, it’s seeing weak spot in industrial and edge networking aspect as effectively.

That stated, administration is of the view that FY1Q24 was the underside for its IoT revenues, with the steering for the section within the subsequent quarter being a progress of mid to high-single digits.

With the second half of FY2024, administration expects that the stock channel to normalize and an awesome product portfolio to elevate issues up then.

Qualcomm is trying to launch the Snapdragon X Elite in the midst of 2024 for PCs, and the corporate has seen traction in design wins on this space because it was introduced in October final yr. The Snapdragon X Elite would be the {industry} benchmark for on-device generative AI and co-pilot experiences for the next-generation Home windows PCs, together with main efficiency and battery life.

Inside Qualcomm’s combined actuality enterprise, it just lately introduced the Snapdragon XR2+ Gen 2, brings about very top quality and immersive combined actuality and digital actuality experiences.

Qualcomm did accomplice with Samsung and Google to result in XR experiences for Galaxy finish customers utilizing the Snapdragon XR2+ Gen 2.

Lastly, inside edge networking, Qualcomm introduced the Snapdragon X35 5G Trendy-RF system, which is the first 5G NR mild Modem RF system on the planet, which can carry a unified 5G platform for IoT gadgets.

Valuation

In my earlier In search of Alpha article on Qualcomm, I raised my 1-year value goal to $159, because the bettering market surroundings for handset, together with the continued enchancment in fundamentals led to revisions in my near-term monetary forecasts.

On this article, I’m reiterating my earlier 1-year value goal of $159, on condition that there aren’t any materials adjustments after the FY1Q24 outcomes.

With that, I might reiterate my Purchase ranking for Qualcomm given that there’s appreciable conservatism embedded in my 1-year value goal, with only a 15x 2024 P/E a number of utilized to the 2024 EPS estimate to derive the 1-year value goal.

In fact, this conservatism is to make sure a ample margin of security and I do suppose that when the cycle turns and restoration strengths, I can enhance the a number of additional given it will possible lead to a a number of enlargement.

For now, the 15x 2024 P/E I utilized for Qualcomm remains to be somewhat conservative in my opinion given the sturdy technological and aggressive management of the corporate.

Conclusion

I believe Qualcomm’s FY1Q24 outcomes confirmed the power within the handset and automotive section.

The handset section continues to point out rising demand and indicators of a backside, whereas the automotive section stays within the early days and exhibits sturdy momentum.

Qualcomm additionally confirmed that it has alternatives within the type of the generative AI upside, and an thrilling new alternative in PCs that could possibly be enormous few years from now. The truth that the Snapdragon 8 Gen 3 cellular platform is used within the Galaxy S24 Sequence to allow on-device AI options exhibits that Qualcomm is certainly successful in on-device generative AI.

The corporate is one to observe on condition that we’re seeing a change within the firm. Whereas handset revenues are prone to lower within the income combine, we are going to begin to see extra IoT and automotive revenues offset that. PCs are positively an space of alternative that I can see Qualcomm successful in as effectively, which can additional present one other pillar of progress and additional diversification to revenues.

{kind=link}