Koshiro Kiyota/iStock Editorial by way of Getty Photos

Notice: All quantities referenced are in Canadian {dollars}. Inventory worth referenced is from TSX and never the USD OTC worth.

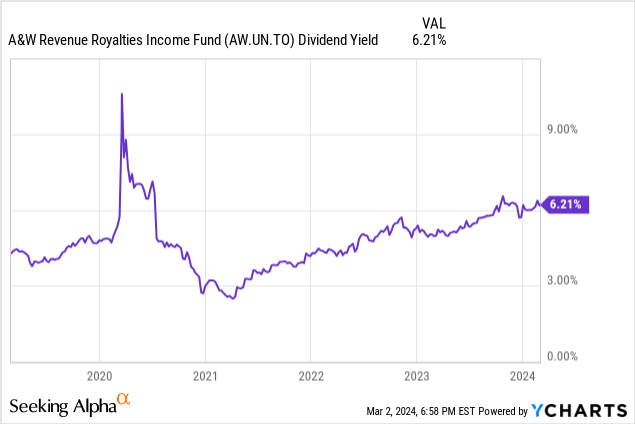

You possibly can bid up something to any worth. You possibly can throw rational multiples out and transfer to “this time is totally different”. That nearly at all times means poorer returns from that time than from the previous interval. A&W Income Royalties Earnings Fund (OTC:AWRRF) (TSX:AW.UN:CA) was in the identical class as its valuation flew excessive in 2021 and leapt to extraordinarily irrational ranges. Certain, there was the “reopening” forward however shifting this to a trailing 12 month dividend yield of three% was simply plain foolish.

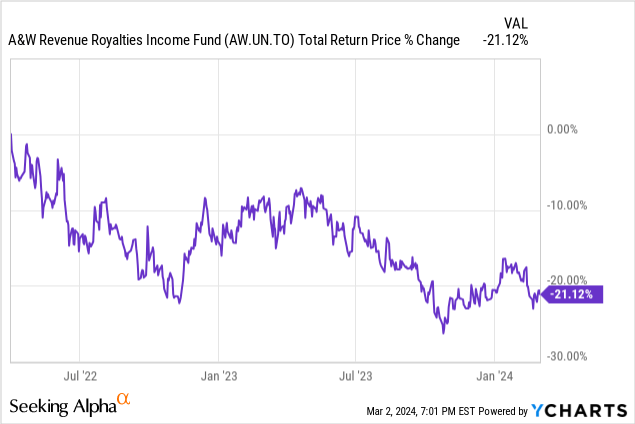

Briefly, although A&W’s trailing 12 month dividend yield truly moved up sooner than the worth and the inventory truly peaked close to $42 in 2022. Should you purchased then, you might be sitting 21% losses, regardless of some hefty dividends.

We go over the This fall-2023 outcomes and inform you why now you can take into account this for an funding place, and what dangers you must take into consideration.

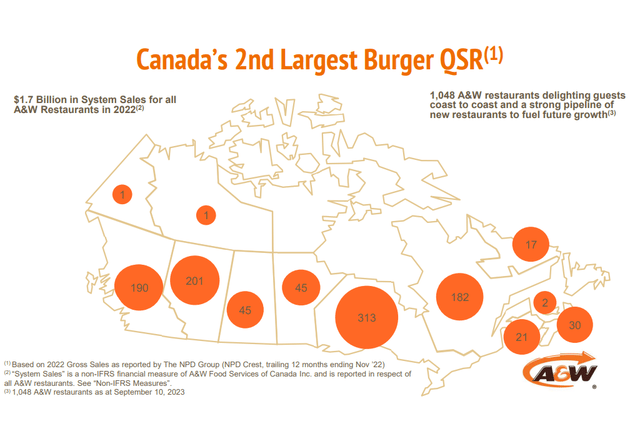

The Firm

We now have launched this firm greater than as soon as, so we cannot get into the small print right here.

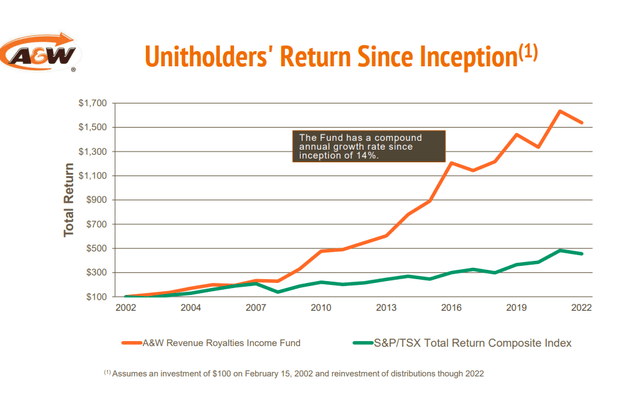

A&W Presentation

These , can see an earlier article spelling out the setup and why that’s helpful. We wish to add right here that the corporate usually retains little or no money because it doesn’t want money to fund its growth. It additionally tends to pay out most of its earnings as dividends and it’s actually aiming for a 100% payout. So traders shouldn’t be complaining concerning the payout ratio being extraordinarily excessive. That is a function, not a bug.

A&W Presentation

This fall-2023

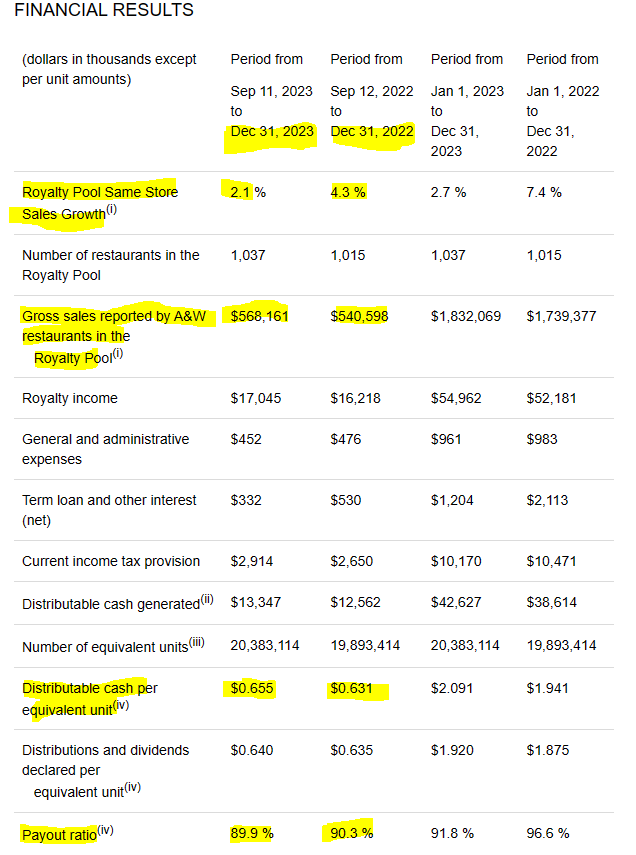

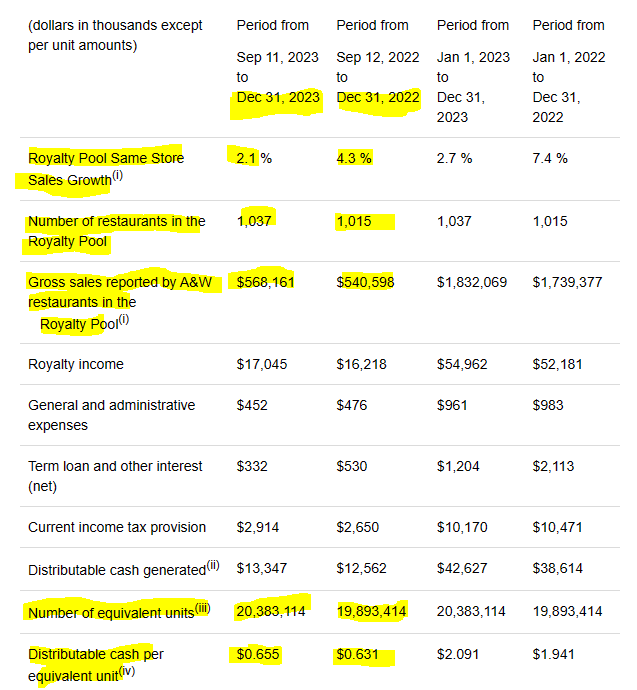

This fall-2023 marked an excellent finish to an excellent yr for A&W. The identical retailer development was mediocre at 2.1%, however total product sales have been up by over 5% from This fall-2022.

A&W This fall-2023 Outcomes

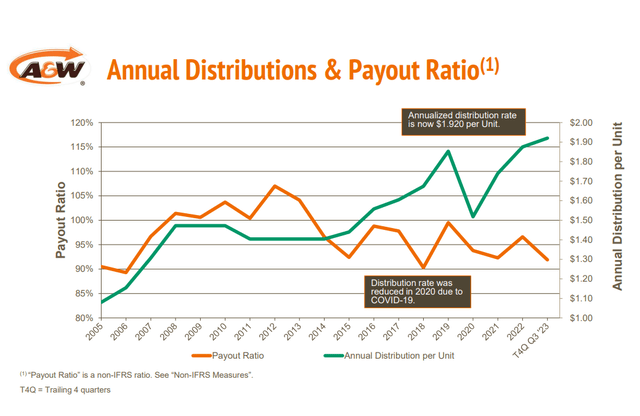

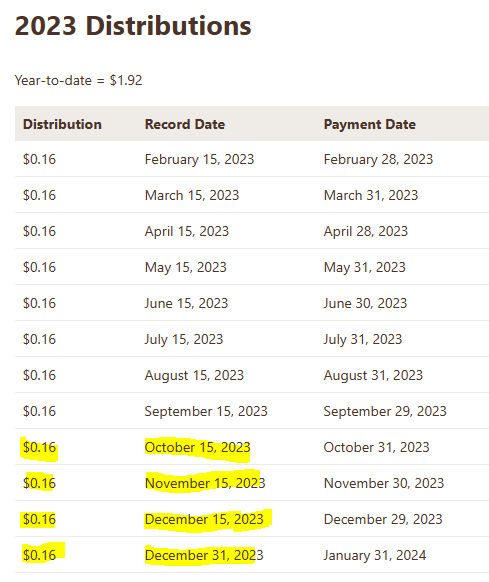

The full variety of eating places within the royalty pool expanded and the distributable money per unit was up by 3.8%. Regardless of a slight improve within the complete quantity of distributions in This fall-2023 relative to This fall-2022, the payout ratio fell barely. These confused concerning the quantities, should word that there’s one additional distribution made in This fall and Q1 will skip one.

A&W Presentation

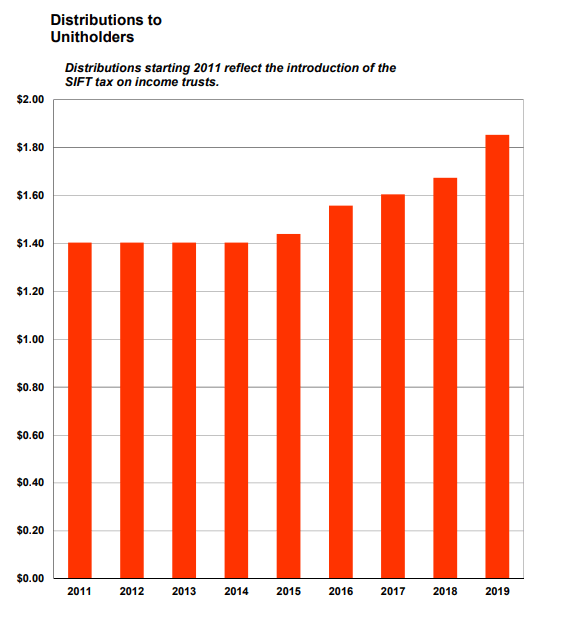

The distributions at the moment are firmly previous the pre-pandemic ranges on an annual foundation and look nicely lined.

A&W Presentation 2019

Outlook

A&W is a royalty play that advantages primarily from gross sales development (quantity in identical eating places) and from inflationary modifications to the highest line in these eating places. What they do not actually profit from, no less than to the identical extent, is the opening of latest franchise areas. The reason being that they need to problem new models for these eating places.

The Royalty Pool is adjusted yearly to replicate gross sales from new A&W eating places added to the Royalty Pool, internet of the gross sales of any A&W eating places which have completely closed. Meals Providers is paid for the extra royalty stream associated to the gross sales of the web new eating places, based mostly on a method set out within the Amended and Restated License and Royalty Settlement. The method gives for a cost to Meals Providers based mostly on 92.5% of the quantity of estimated gross sales from the web new eating places and the present yield on the Models, adjusted for revenue taxes payable by Commerce Marks. The consideration is paid to Meals Providers within the type of extra restricted partnership models (“LP models”).

Supply: Annual Report

They do share considerably in these and naturally over time these gross sales develop as nicely, however the fairness issuance does neutralize this angle of development to some extent. You possibly can see this on this quarter’s outcomes the place the distributable money per unit grew 3.8%, someplace between identical retailer development fee (2.1%) and complete development fee (5.1%).

A&W This fall-2023 Outcomes

This can be a pretty good mannequin although, as for those who add the 6.2% yield and get 3.8% distribution development in the long term, you get to 10% complete returns with fairly minimal capital threat. They’ve truly carried out higher than that over the very long term, although we’d not maintain our breath for something on this ballpark immediately.

A&W Presentation

We will see that lack of threat even on the debt aspect of the equation as A&W had accessed barely $15.7 million of its $40 million credit score facility.

As at December 31, 2023, Meals Providers had drawn $15,726,000 on the credit score facility (January 1, 2023 – $8,149,000), of which $3,366,000 was repaid by January 28, 2024, and had issued $198,000 in letters of assure (January 1, 2023 – $198,000), leaving $24,076,000 of the power accessible (January 1, 2023 – $31,653,000)

Supply: Annual Report

Annual pre-tax royalty revenue was round $55 million, resulting in a microscopic debt to EBITDA quantity. The chance right here comes from the broader macro points for the corporate. Quick meals was at all times costly, and one way or the other the pandemic actually made this right into a “luxurious merchandise”. We now have seen this primary hand of menu gadgets shifting from $5 to $7 over the house of 4 years. 40% worth will increase are actually arduous to swallow and except they get some pricing rationality quickly, there will probably be blowback. Canadians are additionally closely indebted and have hitched their hopes on rate of interest cuts. We are saying that as a result of as a rustic we thought that mortgages resetting each 5 years made extra sense than locking it in for 30 years.

Wealth Easy On X

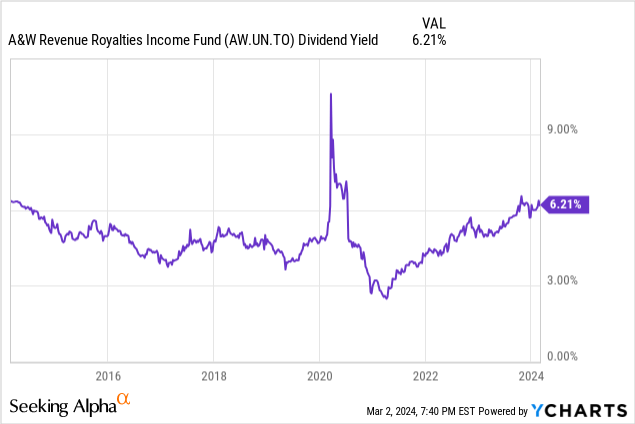

You additionally noticed that within the final quarter the CEO refused to acknowledge what everybody with fundamental math expertise knew, the shopper was hurting. So you will have a riskier setup, however on the plus aspect, we lastly have A&W buying and selling at a degree that is sensible. Should you ignore the 2020 COVID-19 worth crash (the place the trailing 12 month dividend yield went vertical), that is the very best yield you might be getting from this during the last decade.

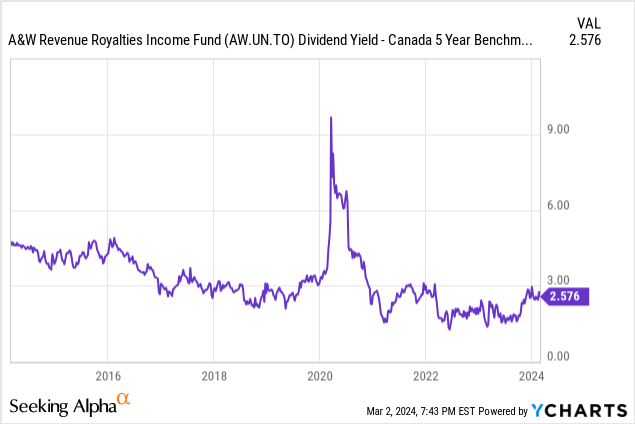

The counterargument in fact is that rates of interest are greater as nicely. Should you plot the dividend yield as a variety to the 5 yr Authorities of Canada bond yields, this isn’t precisely trying low cost immediately.

So which argument will we lean on?

Verdict

Our rationale of giving much less weight to the unfold right here relative to the GOC-5 yields is as a result of we predict {that a} excessive fee setting will solely persist if inflation is cussed. Whereas speedy worth will increase of 2020-2023 will not be taking place, we predict A&W can worth near inflation charges in its annual worth modifications. The corporate has a built-in offset and the very best absolute dividend yield of the final decade is nice sufficient to start out getting in. We can even word right here that if it paid out all the pieces it earned, the dividend yield would have been 6.77%. All issues thought-about, we predict it is a good level to start out nibbling on this one as valuation compression has taken sufficient of a toll. We’re going to do exactly that with a starter place a while within the coming week.

Please word that this isn’t monetary recommendation. It could appear to be it, sound prefer it, however surprisingly, it isn’t. Traders are anticipated to do their very own due diligence and seek the advice of with knowledgeable who is aware of their targets and constraints.

Editor’s Notice: This text discusses a number of securities that don’t commerce on a significant U.S. change. Please concentrate on the dangers related to these shares.

{kind=link}