koto_feja

The AI development has lifted virtually each inventory that has a whiff of synthetic intelligence capabilities available in the market this yr. However what generalist buyers need to be cautious of is that AI is a really broad class, and definitely not all corporations are of comparable high quality.

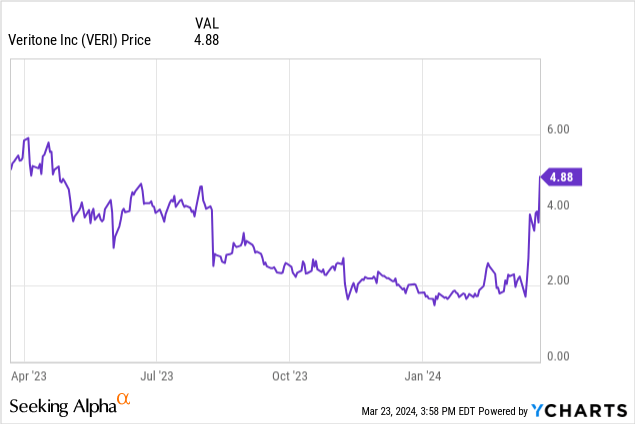

This yr’s rally appears to have lifted all boats, together with Veritone (NASDAQ:VERI), an organization based about ten years in the past that has made little or no incremental progress. Yr to this point, the inventory has practically tripled, recouping a lot of final yr’s losses as financials deteriorated. Do not belief this phantom rally: it is more likely to be short-lived.

I final wrote a bearish article on Veritone final Might, when the corporate was buying and selling simply shy of $4 per share. The inventory had been sleepily buying and selling downward till only in the near past when the corporate introduced This fall outcomes as nicely as a restructuring plan that goals to chop out not less than 15% of annual working bills.

That, in and of itself, ought to be the primary pink flag. AI is having a watershed second this yr, and most AI corporations are investing in development whereas the time is ripe: however Veritone is contracting. There isn’t any doubt, in fact, that this transfer is kind of needed for Veritone (we’ll get into the corporate’s shrinking steadiness sheet later on this article). However the level nonetheless stands: Veritone is definitely not thriving, even when its inventory value rally this yr means that it’s.

Purple flags abound right here, really. The corporate continues to see precipitous y/y drops in income, and new software program bookings are coming in decrease than final yr’s ranges. We observe as nicely that not all of Veritone’s income is software-driven; it nonetheless generates roughly half of its income from “managed companies,” or primarily its legacy ad-tech/media administration companies enterprise.

The query right here is survivability: for my part, Veritone will discover it troublesome to ship on its promise of returning to development and profitability this yr. I stay solidly bearish on this identify and advise buyers to take a position elsewhere.

Sharp contraction within the prime line: the place’s the AI benefit?

An analogous narrative has performed out throughout most software program corporations that ship AI merchandise this yr: enterprise adoption is surging as mainstream curiosity has picked up in ChatGPT, serving to these software program corporations buck the broader macro challenges and obtain excessive ranges of latest bookings.

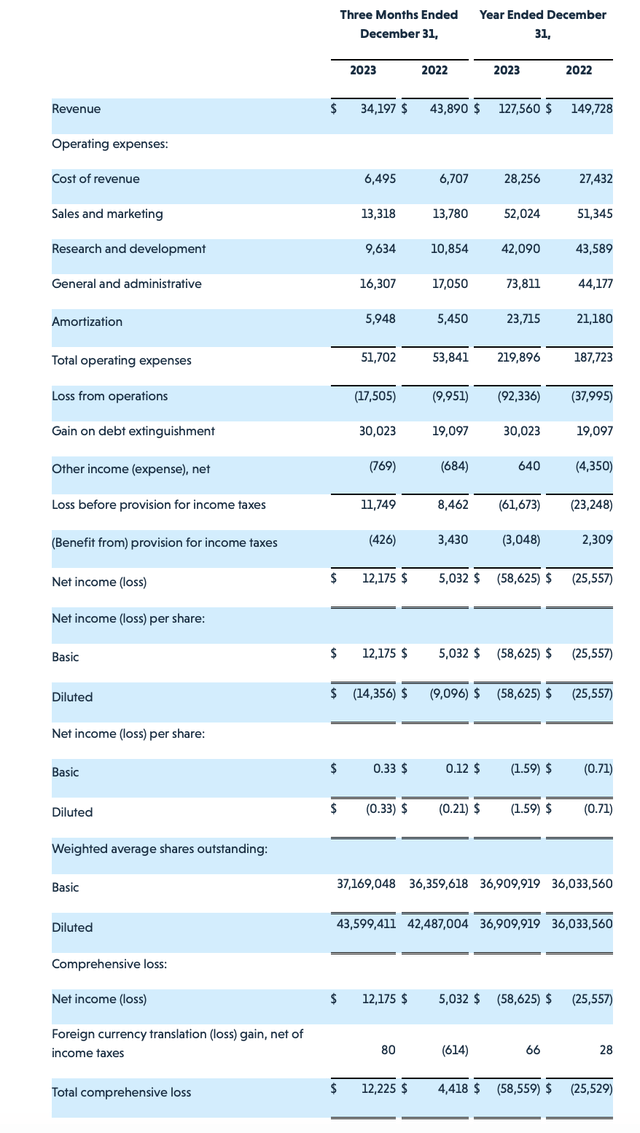

That is not the case for Veritone. Check out its This fall outcomes beneath:

Veritone This fall outcomes (Veritone This fall earnings launch)

Income declined -22% y/y to only $34.2 million (observe right here: Veritone is at an extremely small scale vis-a-vis different publicly traded software program corporations). Observe as nicely right here that software program income (which is what buyers who’re banking on the AI development ought to care about) fell -28% y/y to $19.8 million, whereas managed companies noticed a milder -11% y/y decline.

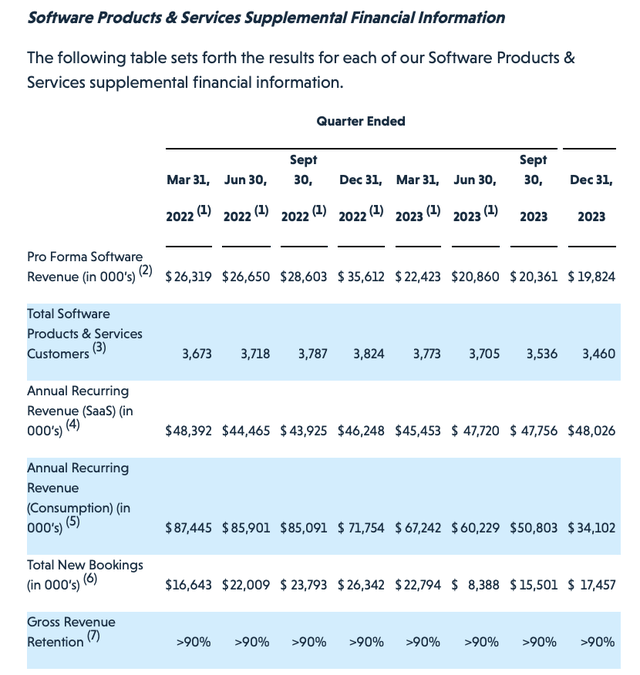

This is the opposite warning signal to be cognizant about: new software program bookings additionally declined -34% y/y to only $17.5 million within the fourth quarter:

Veritone key metrics (Veritone This fall earnings launch)

The corporate attributed the y/y bookings decline to lowered engagement from Amazon (AMZN), beforehand certainly one of its largest prospects. Going ahead, it expects Amazon to contribute to lower than 5% of total income. However that does not imply the danger is concentrated to Amazon solely. In the meantime, the corporate’s rely of software program prospects declined by 76 prospects quarter-over-quarter to three,460. That is the fourth straight quarter of buyer declines since peaking within the December quarter of 2022.

As a reminder, Veritone’s core AI product is known as aiWare. That is primarily a PaaS (platform-as-a-service) providing that offers corporations the flexibility to embed AI options similar to transcription and course of automation into internally constructed purposes. An excellent chunk of Veritone’s software program shoppers sits within the public sector, working with prospects similar to native police forces.

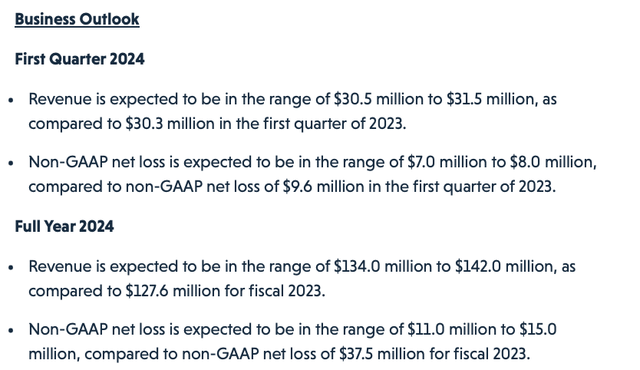

Veritone is projecting to return to whole income development by the primary quarter of FY24, and for the total yr FY24 to develop at a 5-11% y/y clip, as proven within the chart beneath:

Veritone outlook (Veritone This fall earnings launch)

To me, we have seen no proof of a path again to development, particularly with new software program bookings declining in This fall: so we must always deal with this outlook with a heaping grain of salt.

Even with layoffs, can Veritone stay solvent?

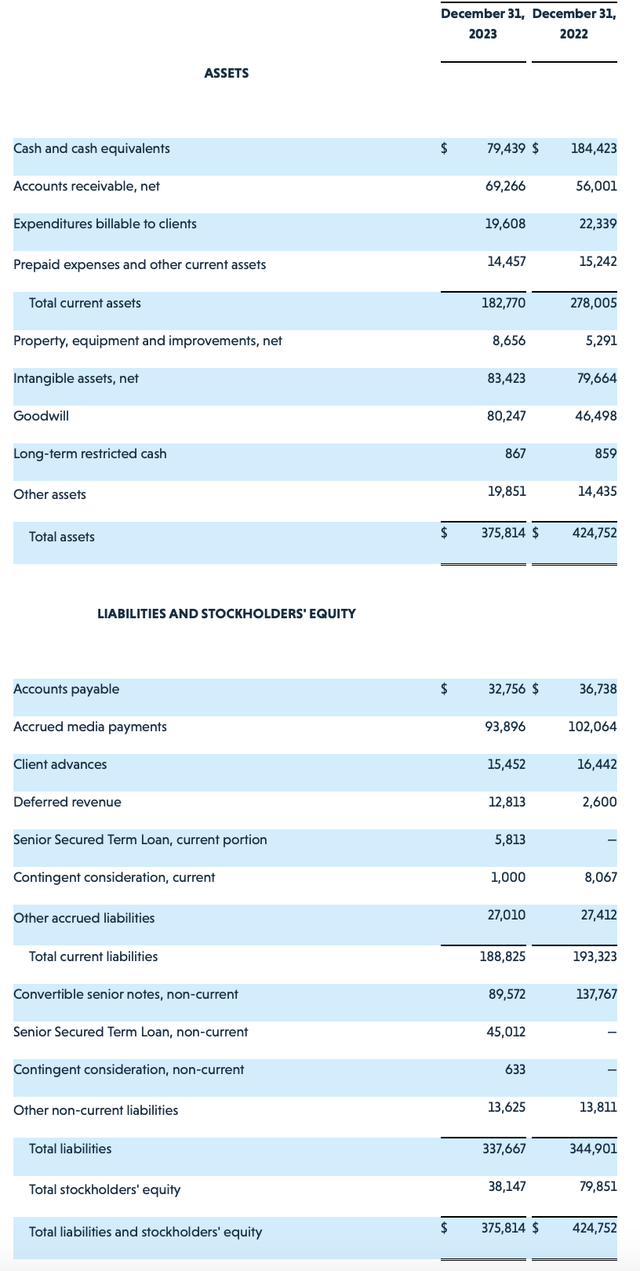

As of the tip of the fourth quarter, Veritone solely had $79.4 million of money left on its steadiness sheet, and it is really in a slight web debt place after contemplating its $50.8 million time period mortgage and $89.6 million of convertible debt.

Veritone steadiness sheet (Veritone This fall earnings launch)

In the meantime, working money circulate in FY23 was -$76.4 million. If Veritone does nothing else, the corporate would run out of money by the tip of the yr.

After all, administration is projecting that it’s going to return to profitability and optimistic money circulate by the second half of FY24 on the again of its layoff plan. Per CFO Mike Zemetra’s remarks on the This fall earnings name:

I am pleased to report that because of our Q1 2024 restructuring efforts, we executed on over $10 million of extra annualized value reductions via immediately, which is included in our full yr in Q1 2024 monetary steering, and we aren’t achieved. Because of this section of reorganization, we anticipate future synergies, each value and income associated to materialize within the latter a part of fiscal 2024, notably throughout our software program services and products traces.

The Q1 restructuring, together with organizational realignments inside gross sales engineering and company, the results of which was a discount of roughly 14% of our international workforce.”

All in all, the corporate expects a 15% financial savings on working bills. FY23 opex was roughly $220 million on a GAAP foundation; so 15% would translate to $33 million of annualized financial savings. All else equal, this is not sufficient to push Veritone’s money circulate again to optimistic. And that is to not point out the danger of additional software program deterioration, as has been the development over the previous few quarters.

Key takeaways

With a really restricted steadiness sheet, declining software program income, and what to me looks like unrealistic steering for FY24, Veritone has a variety of pitfalls forward of it this yr. Proceed to keep away from this inventory.

{kind=link}