Bilanol

Funding Thesis

The American Water Works Firm, Inc. (NYSE:AWK) is the biggest publicly traded water utility in the USA. The utility offers water provide and wastewater administration companies to clients throughout the nation by way of their regulated operations as effectively as servicing some army services too.

AWK stays extremely worthwhile and advantages from what I see as a largely constructive rate-setting panorama. The agency can be very operationally environment friendly which helps increase their margins and enhance shareholder returns.

Present valuations counsel shares of this extremely steady utility could also be undervalued by as much as 10% which is kind of unusual given the virtually bond-like returns.

Subsequently, I price AWK inventory a purchase this present day and see a really constructive long-term worth alternative in shares.

Enterprise Profile

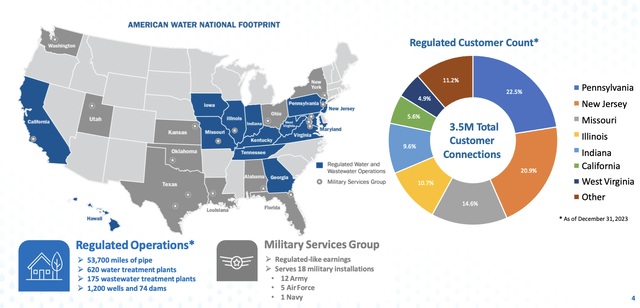

American Water Works Annual Presentation 2024

American Water Works is a regulated utility that operates a large portfolio of water provide and sanitation networks. The agency has over 3.5 million buyer connections in the USA and is the one pure-play large-cap water utility within the nation.

American Water Works Annual Presentation 2024

The utility operates on a large scale with over 53,700 miles of pipe, 620 water therapy crops, and 175 wastewater therapy services current of their regulated utility community. AWK additionally operates a small army companies phase which is a nonregulated enterprise phase.

A number of small-scale acquisitions from municipalities and different non-public enterprises have allowed AWK to increase their operations considerably during the last ten years with the agency planning to proceed this streak of acquisitions for the foreseeable future.

By way of these acquisitions, AWK has constructed a large presence in 13 states together with California, Pennsylvania, New Jersey, Missouri, and Indiana to call just a few.

Susan Hardwick is each the CEO and President of American Water Works and has overseen the continued execution of the agency’s aforementioned progress technique.

I imagine Hardwick is an efficient chief for the utility as she reveals a conservative method to capital allocation and an actual devotion to shareholder returns which I view very positively certainly.

American Water Works Financial Moat

As is the case with most utilities, AWK’s moat is constructed primarily upon the regulatory textual content which defines the utility’s proper to a return on their investments. I additionally see the agency’s army service phase as an extra booster of their general moatiness.

The present regulatory panorama permits AWK to cost a premium on their companies to ensure that the corporate to attain a ample price of return on their investments.

Traditionally, the agency has loved a really constructive rate-setting atmosphere which has allowed the utility to cost sufficiently for his or her water companies as a way to generate round a 5.5% ROIC.

AWK’s large scale and acquisitive method to enterprise has allowed the agency to essentially develop their earnings regardless of the general charges remaining largely steady.

American Water Works IR

The utility typically acquires smaller water provide and sanitation methods from non-public enterprises and municipalities as is the case with their most up-to-date acquisition of Manville wastewater system from the Borough of Manville.

Acquisitions from municipalities are topic to honest market worth legal guidelines which permit AWK to accumulate these property at an assessed worth relatively than a historic price. The states which function in line with these legal guidelines mainly be sure that the municipality will obtain a good deal for his or her asset whereas AWK is ready to profit from a beautiful value for mentioned property.

I actually like AWK’s historical past of acquisitions and imagine the utility has a great relationship with regulators which additional helps within the closing of gross sales. A rising portfolio of infrastructural property additionally will increase the full quantity of infrastructural upgrades that should be completed which additional boosts revenues for the agency.

AWK 2024 Annual Presentation

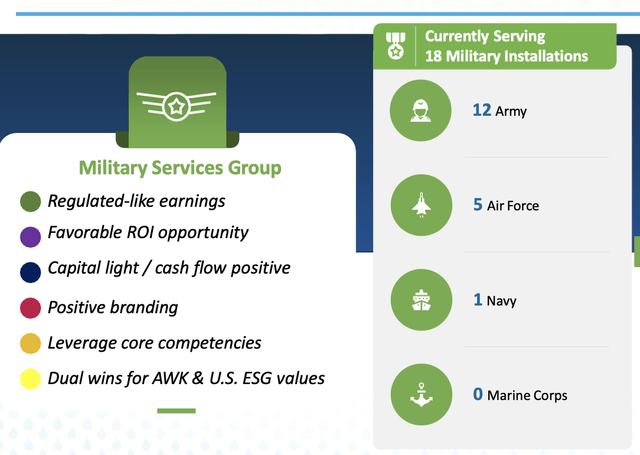

The comparatively small army companies phase is the one nonregulated ingredient of the agency’s operations and sees AWK provide water companies to 12 military, 5 air power and one navy base.

Whereas this phase doesn’t profit from set charges chargeable by the agency, AWK historically has contracts lasting about 25-30 years with these army clients with charges nonetheless securing stable profitability for the agency.

I imagine American Water Works’ regulated utility and army companies enterprise generates a large financial moat for the agency. The corporate enjoys a essentially constructive regulatory atmosphere which whereas generally topic to hostile rate-setting insurance policies, continues to permit the agency to generate steady and dependable returns from their enterprise.

Fiscal Evaluation

American Water Works continues to generate robust returns with their five-year working ROA, ROE, and ROICs of three.35%, 12.10% and 5.50% being very wholesome certainly. Whereas these returns are decrease than some traders might initially wish to see, it is very important take into account the restrict rules positioned on the worth utilities resembling AWK are allowed to cost for the companies.

Nonetheless, the present ROIC of 5.90% could be very constructive for my part, and really sees AWK outperform business rivals Important Utilities, Inc. (WTRG) by round 25bp.

February 15, 2024, noticed AWK publish their This fall and year-end 2023 earnings with stable top-line progress and nice working effectivity characterizing the yr.

AWK FY23 10-Okay

Whole working revenues grew a stable 11.31% YoY for American Water Works with the elevated revenues being pushed primarily by a constructive rate-setting atmosphere together with hotter than typical climate growing demand for retail water.

AWK additionally closed on 23 new acquisitions throughout 2023 which got here at a value of $589M for the agency. Whereas this price of acquisitions might sound very excessive, it’s fairly regular for American Water Works and is a core ingredient of their enterprise mannequin.

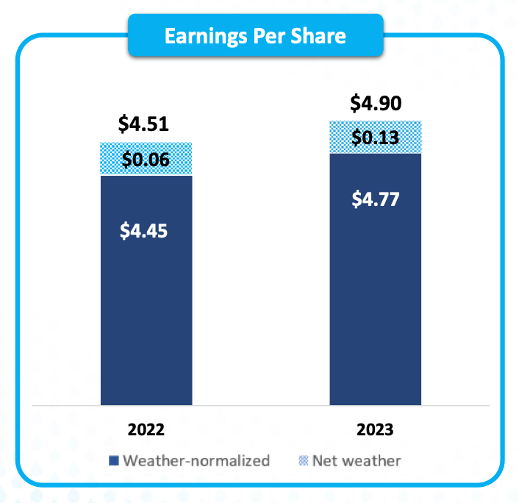

American Water Works This fall & FY23 Presentation

Climate impacts have been estimated to contribute an extra $0.13 to whole EPS earnings with 2023 weather-normalized EPS of $4.77 growing a stable 7.19% YoY.

The present regulatory atmosphere additionally sees American Water Works going through eight new price circumstances in Illinois, New Jersey, Pennsylvania, Virginia, West Virginia, California, Indiana, and Kentucky.

Many traders seem to have taken a bearish view in direction of these ongoing price circumstances which admittedly, do current AWK with the potential for decrease margin charges being set.

Whereas it’s potential that the regulators might take a tighter method than in earlier years, I essentially imagine that the utility will proceed to profit from a constructive system which helps assure earnings for the agency in change for the important companies they supply.

AWK FY23 10-Okay

Whatever the price circumstances, AWK continues to excel in operational effectivity with 2023 seeing whole working bills elevated simply 8.7% in comparison with the 11.31% progress in working revenues.

Such stable price management got here primarily because of tightly managed operation and upkeep prices which is spectacular for my part given how sticky inflation has confirmed to be.

Internet revenue elevated 15% YoY in 2023 due to the upper working revenue and the comparatively smaller enhance in bills.

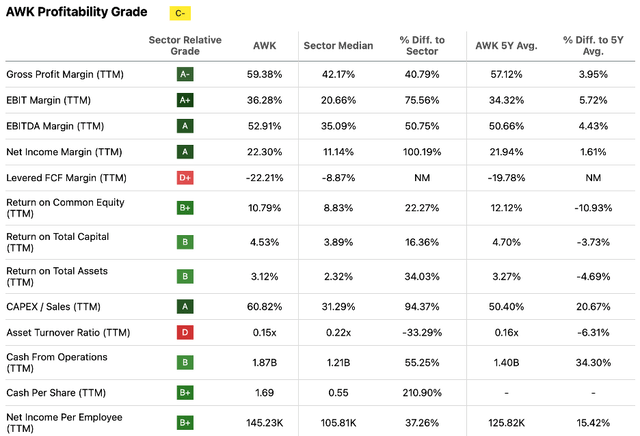

Looking for Alpha | AWK | Profitability

Looking for Alpha’s quant assigns American Water Works with a “C-” profitability ranking which I imagine is excessively pessimistic given their 2023 outcomes. The first components that seem to sway the quant away from a better grade are the poor levered FCF margin and the low asset turnover ratio.

The poor levered FCF margin is comprehensible given the expenditure on acquisitions in 2023 and subsequently doesn’t concern me in any way, particularly contemplating it falls in keeping with the utilities 5Y common.

The asset-heavy enterprise of a utility additionally lends itself mechanically to a low asset turnover ratio and thus this metric additionally doesn’t current any explicit issues.

AWK’s stability sheet suggests the agency has a stable asset allocation technique with cheap leverage and liquidity defining their fiscal profile. The utility has $1.39B in whole present property with whole present liabilities amounting to $2.15B.

This imbalance leaves the agency with a fast ratio of 0.49x and a good present ratio of 0.65x. Such low short-term liquidity is a normal attribute of utilities given how capital-intensive their operations are.

On condition that AWK’s present leverage ratio is round 3.09x, I’m not overly involved in regards to the low fast and present ratios particularly contemplating the variety of transactions the utility made in 2023.

AWK has maintained a ratio within the low threes for the final 10 years and plans to take action for the following ten years.

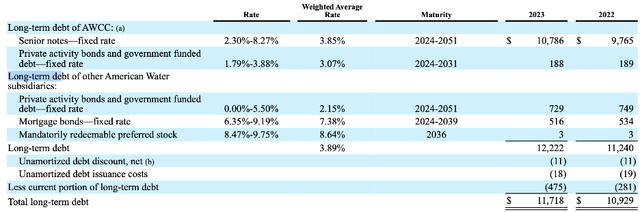

AWK FY23 10-Okay

American Water Works has a complete of $11.72B in long-term money owed which consist primarily of fixed-rate senior notes. I just like the construction of their debt profile and see the focus of long-duration notes as proof of a conservative progress technique.

AWK FY23 10-Okay

Certainly, the present maturity profile helps my speculation with an ideal majority of debentures maturing effectively after 2028.

Moody’s affirms a “Baa1” ranking for AWK’s LT issuer ranking. Moody’s classifies these “Baa1” rankings as being of “medium funding grade” which as soon as once more means that AWK has stable basic economics underpinning their enterprise operations.

American Water Works’ shareholder rewards are additionally fairly constructive with the utility nonetheless having the capability to repurchase as much as 5.1. million shares of frequent inventory beneath a 2015 approved repurchase program.

Whereas no shares have been repurchased in 2023, the utility did proceed to pay out a dividend to shareholders.

Looking for Alpha | AWK | Dividend

Looking for Alpha’s wonderful dividend tab for AWK tells us that the present FWD yield is 2.40% with an annual anticipated pay-out of $2.83 and a pay-out ratio of 56.80%.

Whereas the yield completely may very well be bigger, I imagine administration is prioritizing the sustainability of their dividend as an alternative of large short-term yields. Their 15-year progress streak is spectacular given what number of acquisitions AWK has executed on this time.

I actually like the present state of affairs presently at AWK. Their core operations stay worthwhile and the agency continues to profit from a largely constructive regulatory atmosphere.

This allows the corporate to generate sufficiently profitable returns from their enterprise in order to generate a tangible return on invested capital and reward shareholders handsomely.

Valuation

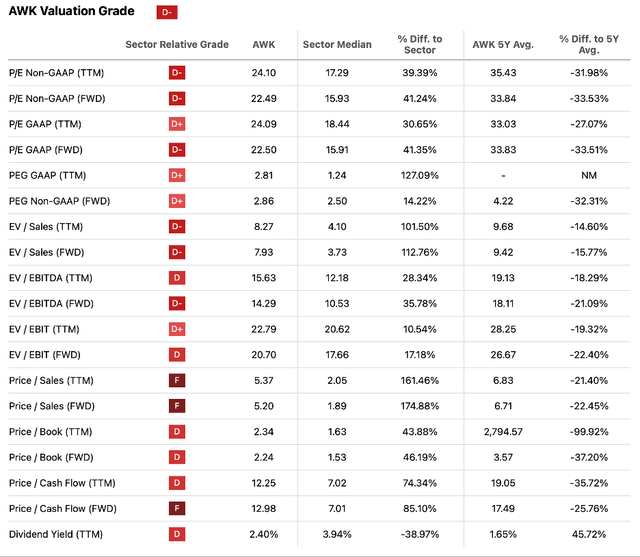

Looking for Alpha | AWK | Valuation

Looking for Alpha’s Quant calculates a “D-” valuation ranking for AWK inventory. I disagree with this relative evaluation and imagine the letter grades assigned to every metric may very well be barely deceptive.

Present P/E GAAP TTM and P/S ratios of 24.09x and 5.37x are each down 27% and 21% respectively from their 5Y averages. The numerous drop in valuations has largely come from traders reacting to a higher-for-longer rate of interest atmosphere and the potential injury this may increasingly do to the relative returns generated by utilities.

Nevertheless, I imagine this market response has been overdone and see the utility’s present P/CF TTM ratio of 12.25x (down 35% from 5Y averages) as proof that AWK inventory has maybe entered an oversold place given how steady earnings from utilities are.

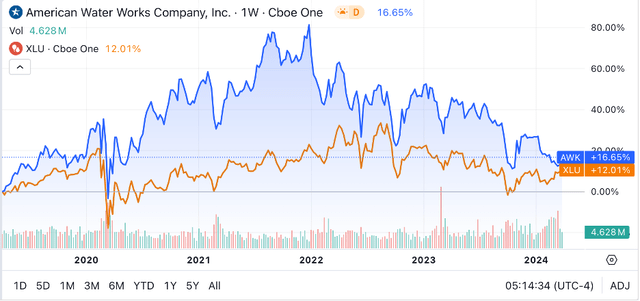

Looking for Alpha | AWK | 5Y Superior Chart

AWK inventory has seen way more volatility during the last 5 years with a increase in the course of the top of the COVID-19 pandemic being corrected post-2022. Nonetheless, AWK has nonetheless outperformed the better utility sector (as outlined by the favored utility sector ETF XLU by 4.5% during the last 5 years.

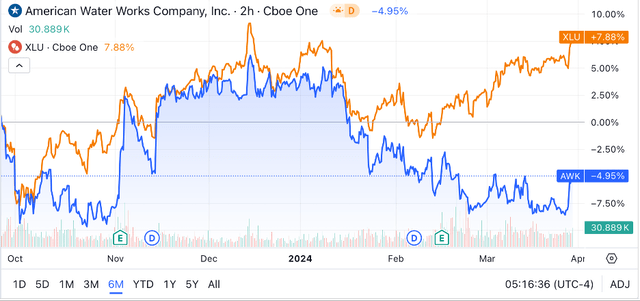

Looking for Alpha | AWK | 6M Superior Chart

Nonetheless, long-term shareholders will discover it troublesome to disregard the poor efficiency of the utility during the last six months with the better market rally that has even lifted most utilities by round 7% being unable to reignite American Water Works’ inventory.

The Worth Nook

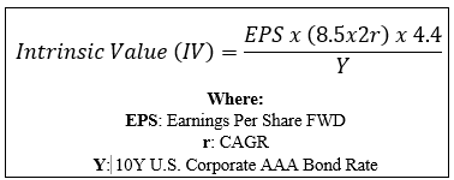

To realize an goal quantitative perspective of the worth current in AWK, we will use The Worth Nook’s Intrinsic Valuation Calculation.

By inputting the present share value of $121.50, 2024 estimated EPS of $5.24, a practical “r” worth of 0.08 (8%), and the present Moody’s Seasoned AAA Company Bond Yield ratio of 5.03%, I derive a base-case IV of $134.50 per share. This represents a ten% undervaluation in shares.

Utilizing a bear-case CAGR worth for r of 0.06 (6%) to replicate a situation the place unconstructive rate-setting limits income progress and nonetheless generates an IV of $112.50. This implies simply an 8% overvaluation at current costs.

I’m reluctant to make any explicit forecasts about AWK’s short-term (3-12 months) efficiency. The potential for any unfavourable or constructive catalyst to considerably influence the share value is actual and will simply shake investor confidence given the convoluted macroeconomic and political panorama within the U.S.

In the long run (2-10 years), I imagine American Water Works will proceed to be the main water provider within the U.S. and see the agency’s technique of constantly buying small water suppliers as a viable technique for long-term progress.

AWK Threat Profile

Whereas utilities are usually thought to be having one of many lowest danger profiles of any business, I need to admit that I see American Water Works now going through extra threats than maybe ever earlier than.

An more and more stringent regulatory atmosphere creates two threats for AWK. Firstly, the more and more strict necessities for the standard and security of the utility being offered (on this case, water and wastewater methods) might place a better fiscal burden on the agency.

Fairly merely, if AWK has to spend money on new infrastructure to adjust to ever-tightening high quality rules it’s fairly potential that their general profitability might be eroded.

The specter of a regulatory infraction additionally presents a large danger to AWK with Hawaiian Electrical energy serving as an ideal instance of the injury alleged negligence in utility companies provision can do to even essentially the most steady of firms.

Secondly, the potential for unconstructive rate-setting limiting profitability has change into an actual risk lately. Ought to a state by which AWK operates determine on charges which give a decrease return on capital for the corporate, an actual degradation in each top-line progress and actual profitability might happen.

Whereas I see little danger in most states, some resembling California current what I imagine might be an unconstructive panorama for AWK within the coming years.

These dangers additionally fall into the environmental and governance ESG classes which essentially limits my means to suggest AWK as an ESG acutely aware decide.

In fact, danger evaluation is an inherently subjective matter and I implore you to conduct your personal complete analysis into any and all dangers which can accompany this firm and its inventory ought to it’s of concern to you.

Abstract

Total, I proceed to view utilities on the whole positively and imagine American Water Works is an excellent instance of how worthwhile and environment friendly a well-run utility could be.

Their excellent operational effectivity helps the utility generate stable returns even from extra constrictive charges and illustrates how well-managed the agency actually is.

The present valuation additionally means that the utility might lastly be buying and selling at what’s an actual undervaluation. Whereas the uncertainty the continuing price circumstances create does enhance the chance related to an funding this present day, I nonetheless imagine the agency makes for a beautiful worth alternative.

Subsequently, I price AWK inventory a Purchase this present day and imagine the utility is well-positioned to proceed producing distinctive shareholder returns in the long term.

{kind=link}