William_Potter

IRM’s Development Catalysts

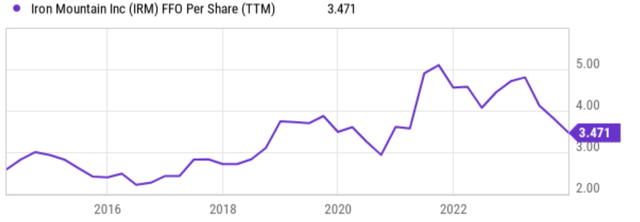

My final article gave Iron Mountain (NYSE:IRM) a promote score, and the objective of this text is to improve the score to carry. The important thing cause for the improve is the subsequent development catalysts which have developed since then. IRM has loved strong earnings development lately as seen within the chart under. This chart reveals that its FFO per share has grown from a mean of round $2.5 to throughout 2015~2017 a peak of greater than $5 in 2021~2022. And the expansion is pushed by elementary catalysts. The highest one on my thoughts is the information heart internet hosting enterprise, a section that’s experiencing explosive development. Over the previous 12 months, the unit has surged by a formidable 27%. This momentum is fueled by the current opening of 4 new colocation facilities, bringing the full to 24. Trying forward, I anticipate this division to proceed rising and contribute extra to the companywide income streams. An excellent portion of the expansion can be pushed by bolt-on acquisitions. Administration has been very efficient at discovering good matches that may speed up IRM’s development. Nonetheless, it’s my view that the steadiness sheet has turn out to be stretched now and the tempo of those additions is more likely to gradual (extra on this later).

Looking for Alpha

Outlook for the Subsequent ~3 Years

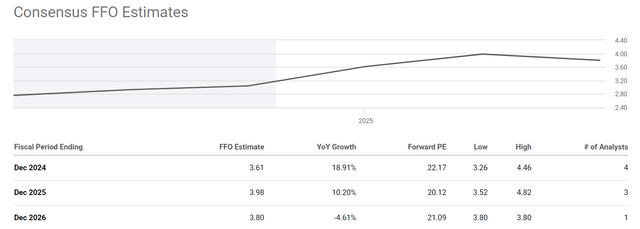

Trying forward, consensus estimates challenge continued development within the subsequent 3~5 years, and I see good causes to share such optimism. The chart under reveals consensus estimates of IRM’s future earnings. As seen, they challenge an FFO of $3.61 for FY 2024, representing a big enhance of 18.91% YOY. The expansion is predicted to proceed at a double-digit tempo of 10.2% into FY2025 after which start to plateau in 2026.

There are certainties amply catalysts afoot that may materialize such projections. In addition to the expansion in knowledge facilities and bolt-on acquisitions, a extra important and sustainable driver in the long run is cross-sell alternatives the way in which I see issues. Extra particularly, I anticipate that Iron Mountain ought to be capable to proceed to cross-sell into its massive buyer base within the years to come back. I do not anticipate an excessive amount of development in its core paper-document storage section. I feel its function would at finest be secure as we steadily embrace the digital age. However keep in mind that it’s by way of this “outdated” enterprise that IRM has developed sturdy relationships with 95% of the Fortune 1000 companies. The connection has gained IRM a repute for securely dealing with delicate paper information, which may simply lengthen into different strains of its service. And the connection may be very stick, as mirrored in its 98% retention price.

As such, I see loads of alternatives for IRM to leverage these current clients by promoting extra associated merchandise, corresponding to shredding paperwork or changing them into digital kind. With its repute for safety, the corporate has additionally been trusted to dispose of knowledge know-how gear on the finish of its usefulness, which creates a really renewable stream of revenue as IT gear turns into out of date and will get changed each few years.

Nonetheless, even when the projected development certainly materializes, I’m involved that the inventory continues to be totally valued, as detailed subsequent.

Looking for Alpha

However Full Valuation is Reached

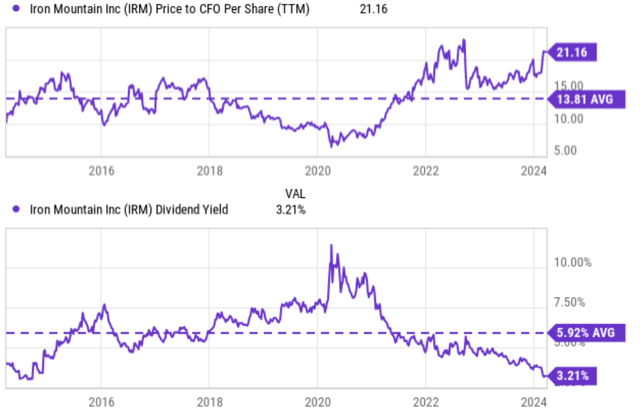

My view is that each one the above catalysts and development prospects have already been mirrored within the present inventory worth. Should you recall from the chart above, the inventory at present trades at 22.2x P/FFO ratio and the ratio would stay about 20x for the subsequent few years even when all of the projected growths are materialized. To higher contextualize issues, the chart reveals IRM’s P/ FFO ratio in comparison with its historic common previously 10 years (prime panel). As seen, a P/FFO ratio of 20+ shouldn’t be solely far above the historic common of 13.8x but additionally near the height ranges in at the least 10 years.

Looking for Alpha

To offer one other different evaluation, the chart under reveals its dividend yield in comparison with its historic common (backside panel). REITs pay out many of the revenue as dividends and subsequently dividends are an excellent (higher in my opinion) approximation to their true homeowners’ earnings in the long run. As of this writing, IRM’s dividend yield is 3.21%. It’s at a degree that once more shouldn’t be solely far under its historic common (5.92% previously decade) but additionally close to the bottom degree, offering one other indication of heightened valuation dangers.

Different Dangers and Last Ideas

In addition to the valuation dangers, there are a number of key dangers value mentioning. A few of them are frequent to each IRM and its friends (corresponding to macroeconomic dangers and competitors dangers), however a few of them are extra specific to IRM. Right here, I’ll give attention to the latter class.

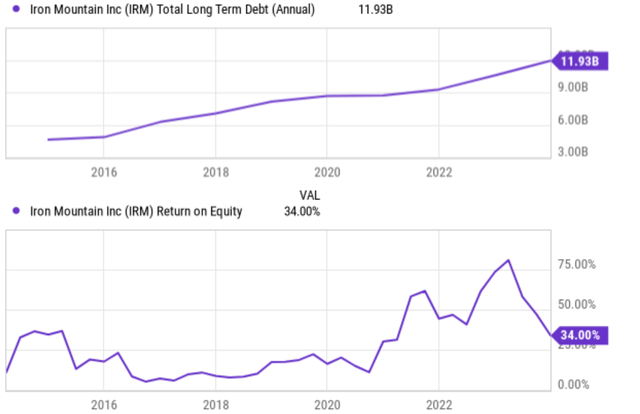

First, the long-term (say 5~10 years) development of its digital section stays unsure as adjustments in know-how evolve quickly. The rising use of cloud storage and digital file administration instruments not solely threatens the demand for bodily doc storage but additionally IRM’s digital initiatives in my opinion. Within the close to time period, its steadiness sheet has turn out to be a bit too stretched for me (see the highest panel of the chart under). As aforementioned, IRM has relied on bolt-on acquisitions previously to gas its development and I anticipate the tempo on this entrance to gradual due to the stretched steadiness sheet. To wit, IRM’s complete long-term debt has been trending upwards. Its complete long-term debt at present sits at $11.93 billion, in comparison with about ~$5 billion solely 5 years in the past. Mixed with the rising rates of interest, such a excessive debt degree can enhance its borrowing prices, eat into its income (see the ROE decline in current quarters within the backside panel), and restrict its future capital allocation flexibility.

To conclude, I price IRM as a maintain below present circumstances weighing the elements mentioned above (good catalysts, excessive valuation dangers, leverage, and so forth.). To recap, its knowledge heart division provides engaging alternatives in a burgeoning business and there are many cross-sell synergistic alternatives. Nonetheless, these constructive catalysts are opposed by some issues. On the prime of my listing is the valuation danger. Each its P/FFO ratio and dividend yield counsel IRM could be close to essentially the most richly valued degree in at the least a decade. Moreover, IRM’s rising debt ranges may restrict its monetary flexibility and hinder its potential to make future acquisitions or CAPEX investments.

Looking for Alpha

{kind=link}