Michael Vi

Palantir Applied sciences Inc.’s (NYSE:PLTR) enterprise has begun to reveal real power in latest quarters, which the corporate is basically attributing to its Synthetic Intelligence Platform. Development at present varies considerably throughout buyer segments although, hiding a few of this power.

Whereas Palantir’s valuation exposes traders to a number of draw back threat, and possibly caps upside within the near-term, Palantir’s constant efficiency and skill to create a compelling narrative will in all probability proceed to assist the share value.

I beforehand instructed that Palantir’s development was prone to proceed accelerating on the again of AIP however that it won’t be sufficient to satisfy quickly inflating expectations. Whereas development has picked up, Palantir has additionally continued to profit from a number of enlargement, which isn’t that stunning given present hype round AI.

Palantir Enterprise Updates

Palantir supplies an information administration platform that leverages the capabilities of AI. It allows customers to combine knowledge from a spread of sources and carry out evaluation in a scalable method. AIP brings the capabilities of LLMs to Foundry, which Palantir believes will increase accessibility. Based mostly on the latest surge in demand, this seems to be the case thus far.

Current commentary by Accenture plc (ACN) means that whereas clients are starting to deploy significant quantities of cash into generative AI, that is nonetheless largely exploratory, with most firms missing the know-how infrastructure to totally understand the worth of AI. This aligns with Palantir’s suggestion that clients are struggling to implement their very own AI options. Palantir may very well be an early beneficiary of generative AI demand on this regard, as its platform ought to deal with a number of buyer ache factors and allow a quicker time to worth creation. Not all firms will wish to outsource knowledge infrastructure although or pay thousands and thousands of {dollars} yearly.

Palantir is making an attempt to drive adoption of AIP by way of bootcamps. These are palms on classes the place clients work with Palantir engineers to deploy AI in operations. It is a mixture of coaching and creating preliminary use instances. Palantir is seeing momentum, notably within the US business enterprise, however believes that it’s nonetheless early. The corporate has accomplished greater than 560 bootcamps throughout 465 organizations to-date, which the corporate believes is compressing gross sales cycles and accelerating buyer acquisition. Palantir can also be working with channel companions in sure areas, together with Japan, not too long ago increasing its partnership with Fujitsu to try to improve adoption of AIP globally.

The extent to which Palantir has a bonus long-term in all probability depends upon whether or not the platform’s ontology genuinely helps LLMs to supply correct and related knowledge. That is unclear as longer context home windows and RAGs may undermine any benefit.

Along with its knowledge platform, Palantir has developed infrastructure know-how to assist its personal enterprise and is more and more opening this as much as clients. Mission Supervisor is a brand new infrastructure bundle (Apollo, Ontology SDK and Rubix) which allows software program integration. Mission Supervisor is now obtainable for each authorities program with full IL6 safety.

Apollo is an infrastructure abstraction layer which reduces the complexity of deploying and managing purposes throughout heterogeneous environments. Rubix is Palantir’s customized Kubernetes infrastructure. It supplies a safe and scalable scheduling and execution engine for distributed compute frameworks.

Palantir can also be giving clients entry to extremely safe infrastructure, opening up authorities alternatives. FedStart allows clients to run their merchandise inside Palantir’s safe and accredited surroundings and is constructed on Mission Supervisor’s capabilities. This considerably lowers the boundaries to providing governments software program and accelerates time to market.

- FedStart IL5 – obtainable now.

- FedStart IL6 – Q2 2024.

- FedStart FedRAMP Excessive – This fall 2024.

Development from Palantir’s authorities enterprise has been comparatively comfortable in latest quarters, however Palantir would not consider this displays the true state of its enterprise. A few of that is as a result of timing of huge contract awards, with the US Military not too long ago choosing Palantir for the subsequent part of TITAN. This contract is value virtually 180 million USD and entails the event of 10 TITAN prototypes, together with 5 Superior and 5 Primary variants. TITAN is a system that collects knowledge from a broad vary of sensors, offering situational consciousness and situational understanding. The principle distinction between the variants is that the superior model features a direct downlink from space-based property.

Palantir additionally not too long ago prolonged its partnership with the Military to proceed creating and working the Military Vantage platform. This platform is used for data-driven operations and choice making.

Whereas these contracts aren’t essentially that essential in isolation, the usage of software program in army purposes is prone to proceed increasing and Palantir is nicely positioned to capitalize on this. Palantir has estimated that the US Military solely spends round 0.015% of its finances on command-and-control software program in the mean time and believes that it will improve considerably over time.

Monetary Evaluation

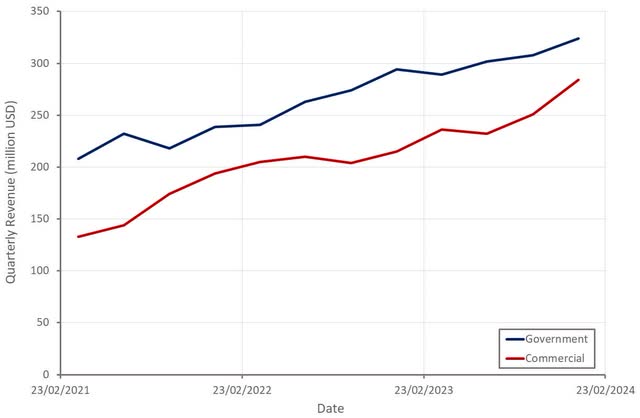

Income was 608 million USD within the fourth quarter, up 20% YoY, with business income rising 32%. The US business enterprise elevated 70% YoY, which Palantir attributed to AIP.

Palantir expects 612-616 million USD income within the first quarter, representing 17% development on the midpoint. For the complete yr, the corporate expects 2.652-2.668 billion USD income, a 20% improve implying a considerable acceleration by way of the yr. US business income is predicted to extend no less than 40% in FY2024.

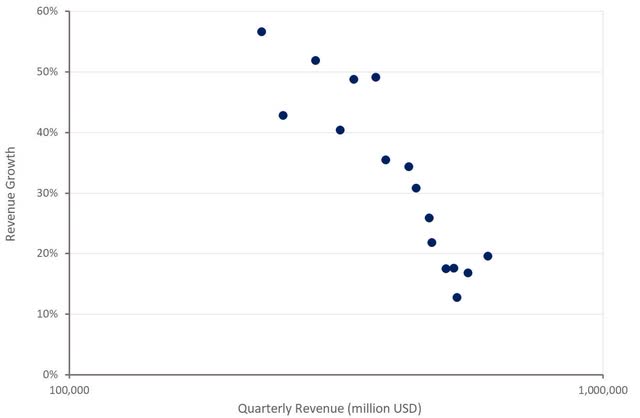

Determine 1: Palantir Income Development (Supply: Created by writer utilizing knowledge from Palantir)

Business income elevated 32% YoY within the fourth quarter, with the US business enterprise up 70% and worldwide business income rising 11%.

Fourth quarter authorities income grew 11% YoY, with US authorities income up 6% and worldwide authorities income rising 27%. Worldwide authorities income included the receipt of funding which resulted in a income catch-up for the quarter. Palantir expects its US authorities enterprise to speed up in 2024.

Determine 2: Palantir Income by Buyer Section (Supply: Created by writer utilizing knowledge from Palantir)

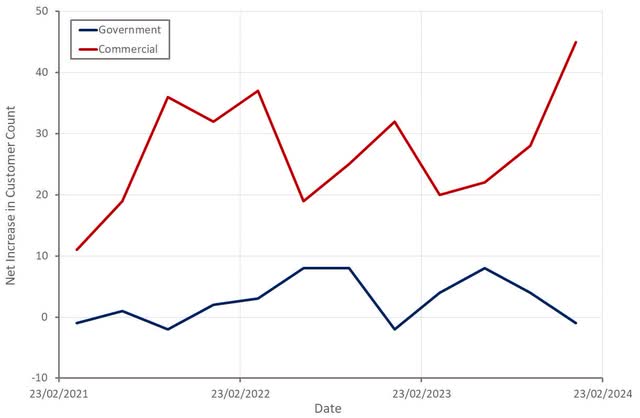

Palantir’s buyer rely was 497 within the fourth quarter, a 35% improve YoY. Buyer development is being pushed by business clients, notably within the US. Whereas Palantir’s buyer rely continues to be low, the corporate continues to land giant contracts.

Web greenback retention within the fourth quarter was solely 108%, though it is a backward wanting determine that’s but to actually profit from the reacceleration of the US business enterprise. Fourth quarter trailing 12-month income from Palantir’s prime 20 clients elevated 11% YoY to 55 million USD per buyer.

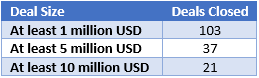

Desk 1: Palantir This fall 2023 Offers Closed (Supply: Created by writer utilizing knowledge from Palantir) Determine 3: Palantir Web Buyer Additions (Supply: Created by writer utilizing knowledge from Palantir)

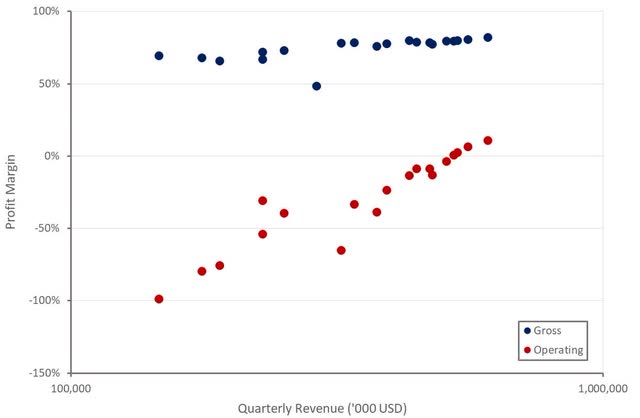

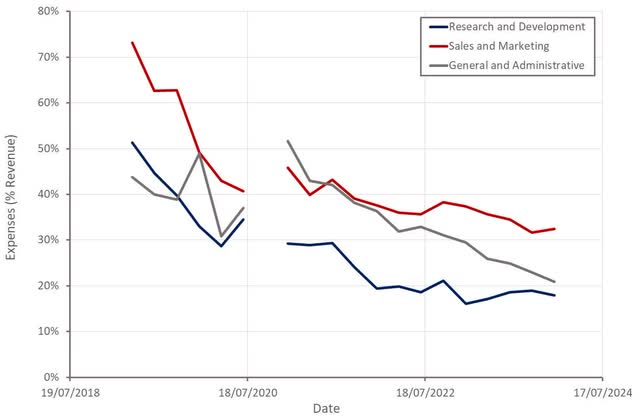

Palantir’s margins proceed to scale in a gradual method, which is one thing that many software program firms have failed to realize in recent times. Enchancment within the fourth quarter was extra modest than earlier quarters although. This seems to be largely attributable to gross sales and advertising and marketing bills. Common and administrative bills stay comparatively excessive, which means that is an space that ought to contribute to additional enhancements in profitability going ahead.

Determine 4: Palantir Revenue Margins (Supply: Created by writer utilizing knowledge from Palantir) Determine 5: Palantir Working Bills (Supply: Created by writer utilizing knowledge from Palantir)

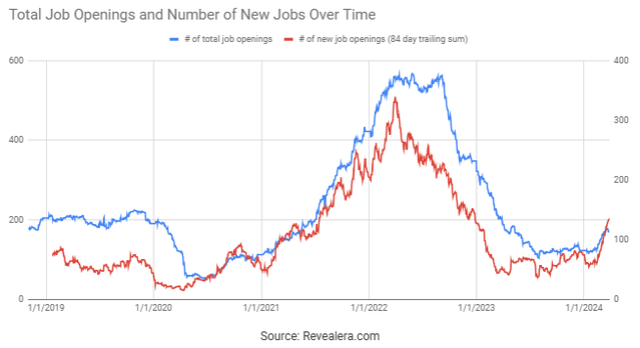

Palantir’s job openings picked up in early 2024 which is supportive of the latest enchancment in income development. Plenty of software program firms have elevated hiring considerably in latest months, which may very well be suggestive of an improved demand surroundings. For some firms, it in all probability additionally signifies beneath hiring in 2023 although.

Determine 6: Palantir Job Openings (Supply: Revealera.com)

Conclusion

Palantir’s development has improved in latest quarters and will improve additional in 2024, notably if the corporate’s authorities enterprise strengthens. Palantir can also be each worthwhile and producing free money circulate, with the corporate’s margins persevering with to steadily enhance. These components, together with a powerful narrative, have contributed to Palantir’s premium valuation.

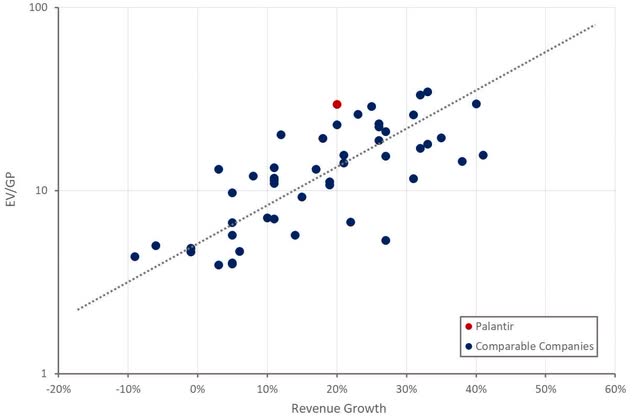

Palantir’s income now appears to be like extreme relative to friends with related development and profitability profiles although. This in all probability would not matter whereas execution is strong, and traders stay infatuated with something AI associated, however valuation will rely ultimately.

Determine 7: Palantir Relative Valuation (Supply: Created by writer utilizing knowledge from In search of Alpha)

{kind=link}