pidjoe

Alliant Power Company (NASDAQ:LNT) is a regulated utility that gives electrical energy to round 1 million clients and pure gasoline to round 425,000 clients within the Midwest.

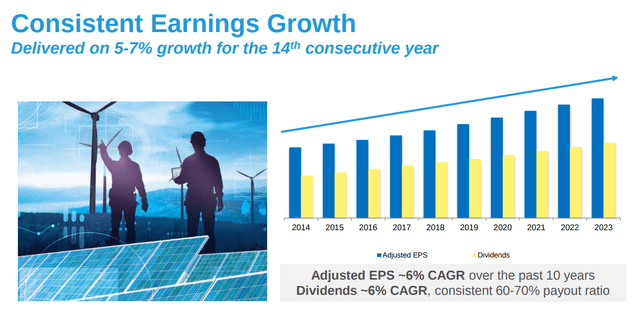

The corporate has had a stable historical past of earnings development, with 14 straight years of attaining at the very least 5% adjusted EPS development.

Alliant Power Investor Presentation

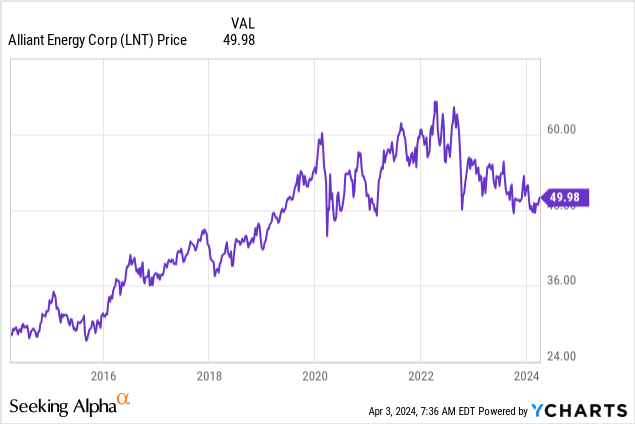

Though Alliant Power has grown adjusted EPS comparatively persistently, its inventory value is beneath its pre-pandemic value in early 2020 and in addition beneath its 2022 highs.

By way of potential causes for the inventory decline, Alliant Power inventory value fell in the course of the starting of the pandemic given the broader market decline. In my opinion, Alliant Power’s inventory value fell in 2022 given headwinds from larger rates of interest.

With the rise in rates of interest from the start of 2022, U.S. Treasury yields have elevated and better U.S. Treasury yields make dividend inventory yields much less enticing, all else equal.

On February 15, 2024, Alliant Power reported 2023 outcomes that mirrored continued regular development. For the long run, administration expects additional development.

2023

For 2023, Alliant Power adjusted EPS rose 5.5% 12 months over 12 months to $2.88 when adjusted for temperature as the corporate delivered on 5-7% development for the 14th consecutive 12 months.

In keeping with administration, temperature modifications leads to a $0.06 per share loss in 2023 and $0.07 per share achieve in 2022.

By way of tailwinds, Alliant Power’s EPS elevated on account of income necessities and better AFUDC from capital investments.

By way of headwinds, curiosity expense, internet, resulted in $0.19 decrease EPS for 2023, with long run debt rising attributable to capital expenditure packages and will increase in rates of interest additionally contributing to larger bills.

My takeaway is that Alliant Power had one other regular development 12 months regardless of larger rate of interest headwinds.

2024

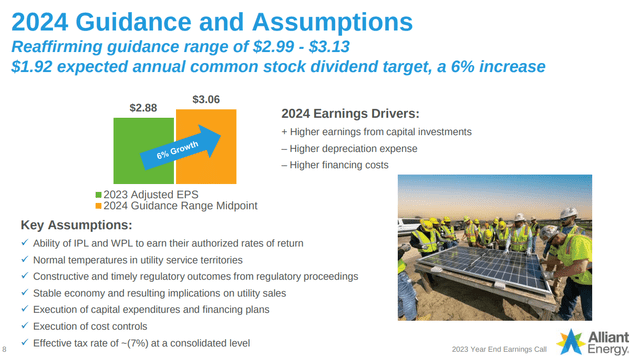

For 2024, Alliant Power expects additional regular development.

For the 12 months, administration reaffirms the earlier adjusted earnings per share steerage vary of $2.99-$3.13 per share as larger earnings from capital investments are anticipated to assist development. On the midpoint of the steerage vary, that will be round 6% development to $3.06 per share.

In consequence, administration has a $1.92 anticipated annual dividend goal for 2024, which might be a 6% enhance from the annual dividend in 2023.

Alliant Power Investor Presentation

By way of the long run, administration believes the corporate has 5%-7% long run EPS development potential.

By way of administration, Lisa Barton changed John Larsen as CEO on January 1, 2024, with Larsen turning into govt Chairman of the corporate.

My takeaway is that administration believes 2024 will proceed to be one other comparatively regular development 12 months for the corporate given larger anticipated earnings from capital investments. In the long run, administration believes Alliant Power has additional earnings development potential as nicely.

Dangers

Declining electrical energy costs might be a headwind if rising electrical energy consumption doesn’t offset value declines.

Demand for pure gasoline may decline as electrical energy prices lower.

Electrical energy consumption within the close to time period may not be as robust as anticipated given temperature modifications or financial modifications.

Alliant Power’s regulated charge base may not develop as a lot as anticipated.

Regulators may not enable Alliant Power to make as a lot because the market expects on its regulated charge base.

My View

The lengthy thesis for Alliant Power is pretty straight ahead because the inventory is buying and selling for a reasonably enticing valuation with a ahead PE ratio of 16.28 for 2024 and administration believes it has 5%-7% long run EPS development potential. With that development, there’s potential for inventory value upside in the long run given the EPS development.

Moreover, decrease rates of interest may result in decrease financing bills, which may assist enhance EPS. Decrease rates of interest may also probably make Alliant Power’s inventory extra enticing to some dividend buyers which may assist its valuation.

In my opinion, I feel rates of interest will start to lower this 12 months and can normalize in a 12 months or two as inflation is not as excessive because it was in 2022 or early 2023.

When incorporating debt, Alliant Power remains to be pretty enticing as the corporate has an funding grade credit standing, earnings development potential, and a ahead EV/EBITDA ratio of 12.06 versus its 5 12 months common of 13.88.

Within the medium to long run, nevertheless, I feel there’s extra uncertainty round Alliant Power’s long run EPS development charge given two developments.

One development, which I feel is simply starting, is the rise in electrical energy consumption given the will increase in EVs, information facilities, and different comparatively new sources of demand.

One other development, which is beginning to even have a bigger impact, is the lower in electrical energy manufacturing prices in photo voltaic.

In keeping with a 2021 report from the Workplace of Power Effectivity & Renewable Power, photo voltaic PV technology accounted for round 3% of U.S. electrical energy provide in 2020 and is anticipated to extend considerably as a proportion of the overall within the subsequent few a long time as utilities decarbonize. Below some situations, photo voltaic will account for round 40% of U.S. electrical energy provide by 2035 and 45% by 2050.

In the meantime, the price of photo voltaic technology is anticipated to say no considerably from the start of the last decade. By way of 2019 {dollars}, as an example, the U.S. authorities has a aim of reducing the levelized value of vitality for utility PV to 2¢/kWh by 2030 from 4.6¢/kWh in 2020.

Given photo voltaic vitality is intermittent, there’s presently a restrict to the quantity of photo voltaic technology a utility can have as photo voltaic can not meet baseload demand, which varies from place to position however could be round 50% of peak demand.

With the rising financial competitiveness of battery expertise, nevertheless, the photo voltaic and battery mixture may be capable of offset among the usually dearer baseload demand sooner or later.

In the long run, the development of extra economically aggressive photo voltaic and batteries may imply a decrease than anticipated regulated charge base for the vitality technology a part of Alliant Power’s enterprise. Moreover, some massive industrial clients may self-generate vitality if photo voltaic may be very economically aggressive, lowering demand as nicely.

On account of these two developments, I feel there are two situations within the medium to long run.

One state of affairs is the place electrical energy consumption grows considerably and Alliant Power has to improve its grid and spend significantly extra on its regulated charge base in consequence. On this state of affairs, the additional spending on the grid and additional funding in vitality manufacturing to fulfill the rise in electrical energy demand greater than offsets any decreases attributable to decrease electrical energy technology prices.

In one other state of affairs, electrical energy manufacturing prices decline considerably and electrical energy consumption will increase do not offset the manufacturing value decline, resulting in a lower than anticipated regulated charge base. If this happens, I feel regulators and what they determine by way of allowable returns on regulated charge bases will likely be more and more essential.

Personally, I feel the bullish former state of affairs is extra seemingly however given the bearish latter state of affairs is a risk, I’d personal Alliant Power in a diversified portfolio that features the Magnificent Seven and I’d not charge it as an ‘Chubby’.

Given the close to time period EPS development potential, I nonetheless charge Alliant Power a ‘Purchase’ in a diversified portfolio.

EPS Estimates

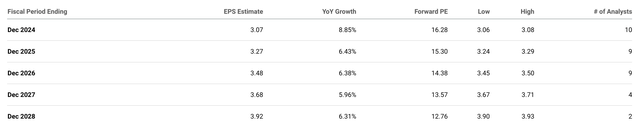

By way of EPS expectations, analysts on common anticipate Alliant Power to earn $3.07 per share in 2024, $3.27 per share in 2025, and $3.48 per share in 2026 in accordance with Searching for Alpha. That provides the corporate a ahead PE ratio of 16.28 for 2024, 15.30 for 2025 and 14.38 for 2026.

Searching for Alpha

By way of EPS estimates by 2026, I feel Alliant Power may meet the typical analyst EPS estimates given its historical past of rising adjusted EPS at across the vary that analysts are predicting.

When together with 2023’s outcomes, Alliant Power has had adjusted EPS of round 6% CAGR during the last 10 years.

Previous 2026, nevertheless, I feel administration’s long run 5-7% development projection in EPS is likely to be much less sure given the impact of photo voltaic and the potential will increase in electrical energy consumption. As I discussed earlier than, there’s an upside state of affairs and a draw back state of affairs, though I personally am cautiously optimistic and suppose the upside state of affairs is extra seemingly.

By way of honest valuation, I feel Alliant Power may commerce for a ahead PE a number of of 18x 2024 EPS estimates as rates of interest probably start to normalize, which will get me a value goal of $55.26 in round a 12 months.

By way of the lengthy thesis, I’d comply with Alliant Power’s earnings reviews, rates of interest, electrical energy consumption developments, and electrical energy costs. If electrical energy consumption rises considerably and electrical energy costs do not decline a lot in any respect, I feel this could assist the inventory. I feel earnings reviews might be catalysts.

{kind=link}