ryasick/E+ through Getty Pictures

Thesis

Whereas boring and boring, Stanley Black & Decker (NYSE:SWK) affords traders an unbelievable alternative to personal a chunk of the world’s industrial crown jewel. With no discuss of Synthetic Intelligence or Massive Language Fashions, this dividend king has fallen out of favor on this technology-driven market, at the very least for now. What many have didn’t account for is that this speedy technological development solely occurs with an infrastructure and building increase. That is the place the worldwide chief in instruments & outside gear comes into play. As you might recall, it is good to be within the pick-and-shovel enterprise when everyone seems to be digging for gold.

Firm Overview

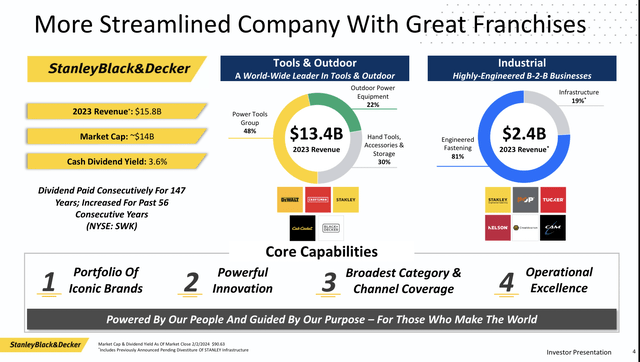

Stanley Black & Decker, Inc. is the longtime international chief in instruments and outside gear. Established in 1843 in New Britain, Connecticut, this industrial big is house to among the most generally recognized names in the area. These Iconic manufacturers embody Dewalt, Craftsman, Black + Decker, Lenox, Irwin, and Cub Cadet.

Stanley Black & Decker Public Filings Stanley Black & Decker Public Filings

Almost all the pieces round you, from the house you reside in to the roads you journey, is constructed with SWK merchandise. Over 50 SWK instruments are offered each second, and over 90% of automobiles and lightweight vans throughout North America and Europe use SWK fasteners. It’s secure to say that the world could be a really totally different place with out this iconic firm.

In my eyes, it’s this robust model recognition and international scale that give SWK a comparatively robust moat. Along with these aggressive benefits, I at all times search for important pores and skin within the recreation on behalf of firm administration. CEO Donald Allan checks this field off, proudly owning 82,564 shares value roughly $8 million.

Why Is It Down?

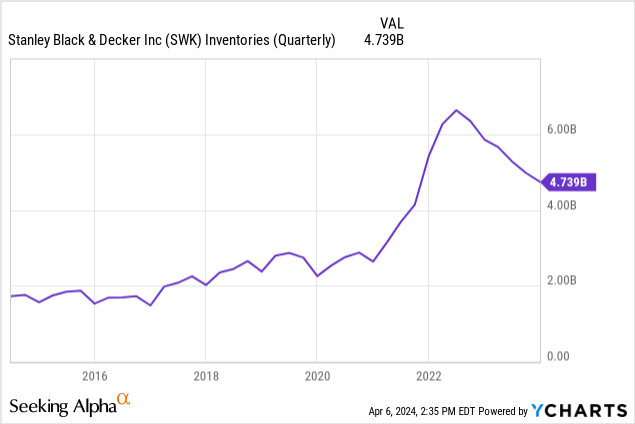

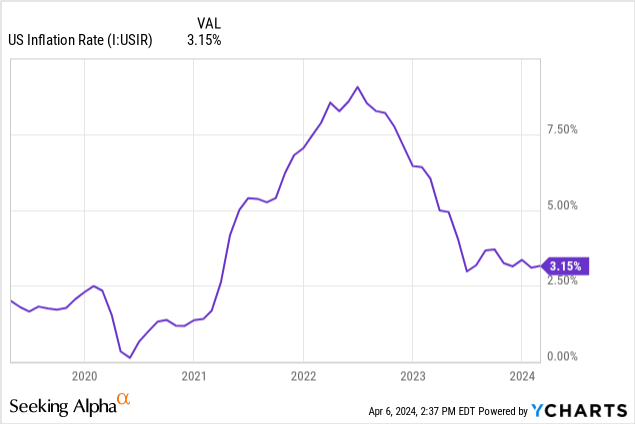

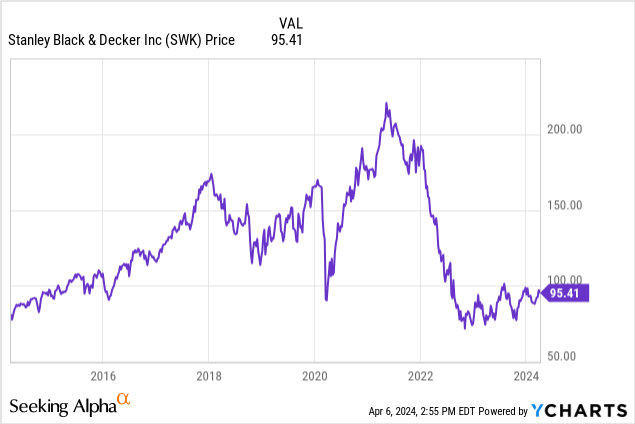

After hitting an all-time excessive of $225 in 2021, Stanley Black & Decker has since fallen over 65%. Whereas many elements contribute to this extreme decline, COVID-19 and the provision chain disruptions ensued are primarily in charge. For an prolonged interval through the pandemic, folks had been caught of their houses and had no alternative however to deal with areas that wanted renovations and touch-ups. This led to an in a single day uptick in demand for SWK, and the corporate was pressured to extend its sources to match it. Full-time staff ballooned from 53,100 to 71,300, an almost 35% enhance in lower than one yr. Along with this enhance in labor, stock volumes skyrocketed from 3.68B in 2021 to six.64B in 2022.

This stock bloat was much more expensive when factoring within the spike in uncooked materials inflation. As inflation and better enter prices continued to deteriorate profitability, SWK confronted one more headwind: The Federal Reserve’s quickest fee hike cycle in historical past. This surge in the price of borrowing pressured firms to delay capital expenditure tasks and shoppers to carry off on massive ticket purchases. SWK is especially weak to residential building and residential renovation, an space that noticed a dramatic slowdown.

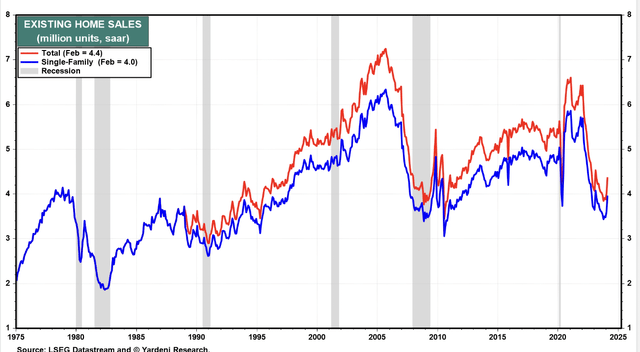

Yardeni Analysis

As highlighted within the following chart offered by Yardeni Analysis, constructing permits and present house gross sales concurrently fell off a cliff. This decline was instantly felt at SWK, with top-line revenues going through YoY declines of roughly 7% in FY2023.

Restructuring Plan

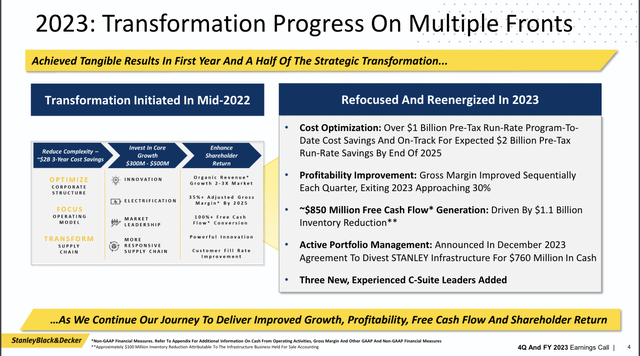

To fight these important headwinds, administration initiated a three-year $2 billion price financial savings plan in 2022. This plan targeted on remodeling the corporate’s provide chain, decreasing stock complexity, and right-sizing the company construction. Administration has performed a wonderful job executing this plan and is working properly forward of schedule, having already reduce over 1B in pre-tax run-rate price financial savings.

Stanley Black & Decker Public Filings

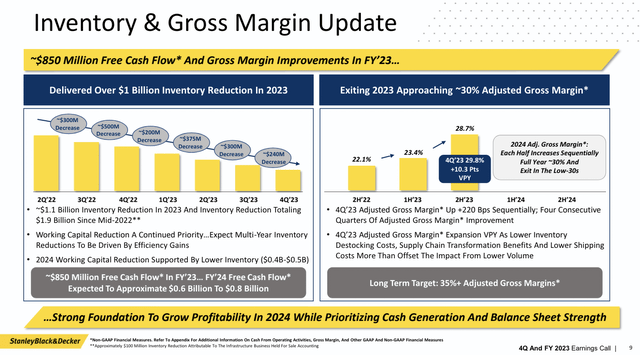

Worker headcount has consolidated from 71,300 to extra traditionally in-line ranges of fifty,500. Stock ranges have already been diminished by $1.9B since mid-2022, and administration has forecasted an extra discount of $400-500 million in FY 2024. Within the This autumn 2023 earnings name, administration highlighted the numerous discount in complexity, citing that that they had already recognized roughly 85,000 SKUs for discontinuation. This relentless deal with stock discount has been the largest driver of optimistic free money movement technology, contributing roughly $850 million in 2023. When it comes to worth add, this restructuring plan has super alternative. Spreading the $2B in pre-tax run-rate price financial savings throughout the 151m shares excellent ends in $13.25 per share in worth. If you happen to had been to assign a extremely conservative 10x P/E a number of to this added worth, the consequence could be $132.50 per share. In my view, the potential worth add of this important restructuring plan is being missed. As well as, SWK just lately introduced that they’ve efficiently divested STANLEY infrastructure for an all-cash deal of $760 million. This divestiture emphasizes the heightened deal with simplification and making a extra streamlined, built-in firm.

Macro Tailwinds

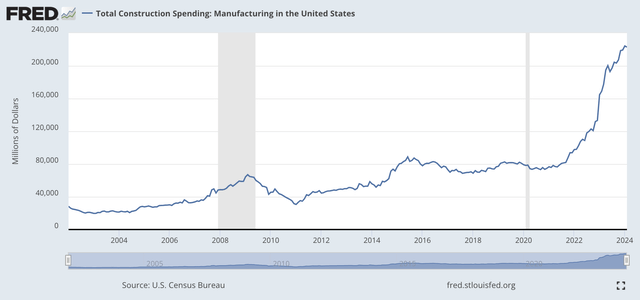

Though SWK continues to face stress from the upper rate of interest setting, loads of longer-term tailwinds are in place that assist a multi-year restoration. Some of the impactful of those is the Bipartisan Infrastructure Regulation. Signed in late 2021, this legislation allotted over $400B to restore roads, bridges, airports, and different infrastructure throughout the US.

U.S. Census Bureau

The funding has led to over 40,000 new tasks and record-high jobs throughout the building sector. Along with this legislation, the Biden Administration signed the bipartisan CHIPS and Science Act of 2022. This legislation explicitly targets home manufacturing and has already had a significant impression, positively contributing to a 116% enhance in new manufacturing services in 2023. In my view, this enhance in infrastructure funding and push for extra building tasks creates a multi-year runway of natural development for SWK.

As famous, being within the pick-and-shovel enterprise is sweet when others dig for gold. Among the world’s most vital and predominant expertise firms are betting massive on the unreal intelligence race. To hold these plans out, we’re starting to witness a speedy surge in cloud infrastructure and information middle manufacturing. Simply final week, Amazon (AMZN) introduced plans to spend nearly $150B on information facilities within the coming 15 years to deal with the anticipated increase in AI demand. Based on Grand View Analysis, the worldwide information middle building market is anticipated to broaden at a compound annual development fee (CAGR) of seven.4% till 2030. Though SWK will likely be on the sidelines within the race for cloud computing and AI, they are going to be joyful to promote as many screws, bolts, fasteners, and instruments because it takes to construct out the infrastructure.

Innovation

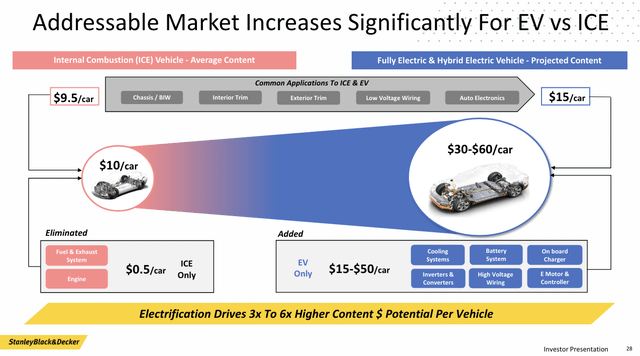

Along with these macro tailwinds, SWK has refused to turn into complacent and has remained steadfast in its dedication to breakthrough innovation and higher-margin product traces. One of many few brilliant spots in the newest quarter was the economic section, particularly aerospace and automotive, with every attaining double-digit income development. One of many greatest drivers behind this speedy development is the rise within the addressable marketplace for electrical autos (EVs) as a substitute of inside combustion (ICE) autos.

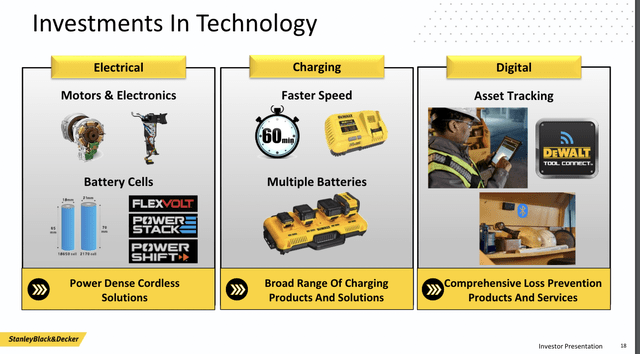

Stanley Black & Decker Public Filings

Electrification drives 3x to 6x greater content material per automobile, rising from $10 per automobile to the $30-$60 vary. With an industry-leading presence, SWK has constructed relationships and belief with main OEMs to turn into probably the most credible full methods accomplice.

The upper-margin product traces throughout the EV {industry} have additionally carried over to the SWK software {industry}. SWK has positioned itself to take full benefit of the transition to electrification on a number of fronts. Stanley Black & Decker is the fastest-growing franchise within the cordless/electrical outside energy gear {industry} and nonetheless has far more room for additional penetration.

Stanley Black & Decker Public Filings

That is an space the place SWK forecasts its subsequent wave of development because it plans to realize objectives of natural income development 2-3x market. Administration is investing $300-$500M in core development by 2025, highlighting their relentless hunt for market share. The way in which I see it, this transformation to cordless energy instruments supplies SWK with an incredible alternative to capitalize on a model new section line.

Margin Enlargement

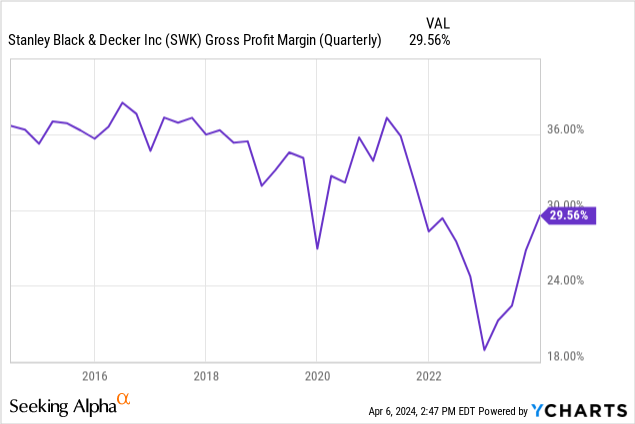

Some of the necessary initiatives of the SWK turnaround is the restoration of margins. After going through inflationary headwinds and extreme stock bloat, gross revenue margins fell sharply from 35.88% in Q2 2021 to an eye-opening 19.51% in This autumn 2022.

Stanley Black & Decker Public Filings

Fortunately, administration has targeted relentlessly on returning to historic ranges, and we will now safely label this the inflection level. Adjusted Gross margins have improved sequentially over the previous 4 quarters and now sit comfortably at 29.82%. Administration has attained this quick enchancment via decrease stock volumes, simplified provide chains, and an extra emphasis on direct-to-consumer (DTC) as a substitute of wholesale. Administration stays dedicated to their purpose of 35% adjusted gross margins by 2025 and expects to exit 2024 within the low 30s vary. I imagine combining the above-listed elements with higher-margin electrical product traces ought to contribute to long-term adjusted gross margins of 36% or greater.

Financials

Administration has been very clear with traders concerning medium-term strategic objectives: Stock discount, debt discount, and inside development investments. As I discussed, administration has performed an outstanding job attacking extreme stock, with internet reductions of $1.9B since mid-2022. Stock discount has led to a big rise in annual free money movement, which is getting used to scale back debt. SWK has appreciable leverage with $7.68B in whole debt and $449M in whole money and short-term investments. This extra debt outcomes from SWK’s poorly timed $1.5B acquisition of MTD merchandise in 2021. Nonetheless, given the sturdy free money movement technology and plans of utilizing any capital in extra of quarterly dividends towards debt discount, this isn’t one thing I’m overly involved about. Whereas there isn’t a debt maturity till 1Q 2025 ($500M), SWK plans to make use of the latest money readily available ($760M) from the STANLEY infrastructure divestiture to scale back debt. As a shareholder, I welcome this quick motion with open arms because it reduces pointless curiosity expense fees.

One of many advantages of proudly owning a improbable firm like SWK is that as administration turns the ship round and macro tailwinds kick in, you receives a commission a beneficiant 3.4% dividend. SWK has paid its quarterly dividend for the previous 147 years and has elevated it for the previous 56 years. This dividend king has no intention of dropping its sacred crown.

Steerage

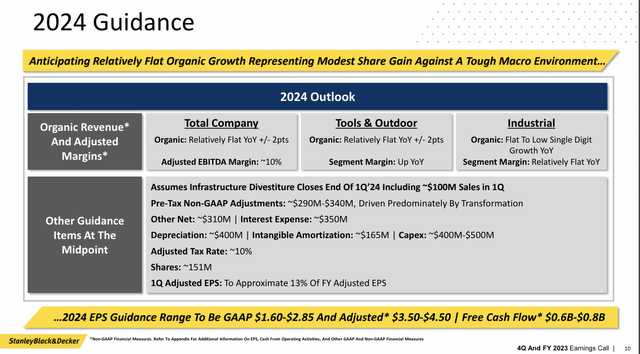

Many shareholders weren’t stunned by administration’s conservative 2024 steerage. With a weak macro backdrop, administration set the bar low and forecasted weak shopper and outside demand.

Stanley Black & Decker Public Filings

Administration guided for comparatively flat YoY natural development, Adjusted EPS of $3.50-$4.50, and free money movement of $600- $800M. Nonetheless, given the sturdy adjusted gross margin enlargement and ahead-of-schedule $2B price financial savings plan, I see the 2024 outlook as extremely conservative.

Valuation

Throughout 2021, Stanley Black & Decker traded between $200 and $220, hitting an all-time excessive of $225. Listed below are the financials of SWK in 2021.

- Complete Income: $15.28 Billion

- Gross Revenue: $5.09 Billion (33.32% margins)

- Internet Revenue: $1.54 Billion (10.06% margins)

- Shares Excellent: 165 Million

- Earnings Per Share: $9.32

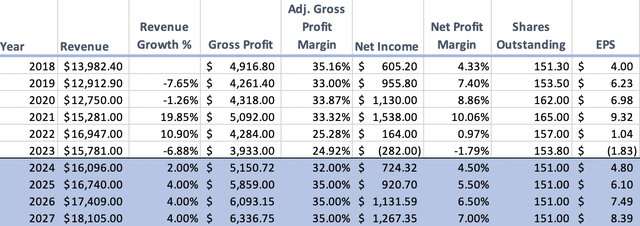

Right here is my valuation for Stanley Black & Decker under. That is intentionally conservative, considering the corporate’s price financial savings plan, margin enlargement, and {industry} volumes returning to historic ranges.

Authors Calculations, Stanley Black & Decker Public Filings

Given administration’s conservative top-line steerage, I forecasted 2024 income development of two%, adopted by extra traditionally in-line income development of 4% via 2027. This return to reasonable development continues to be comparatively conservative, given the SWK 5-year common development fee of seven.19%. Subsequent, I used administration’s adjusted gross margin forecast of the low 30s in 2024 (32%) and assumed they hit the 35% gross margin purpose in FY2025. Utilizing SWK’s five-year common internet earnings margin of 6.44% as a benchmark, I constructed internet revenue margins that may enhance to 7% by 2027. With the associated fee financial savings measures in place, simplified provide chains, and better margin product traces, I imagine 7% internet revenue margins are certainly attainable. With administration’s forecast of 151M shares excellent, this results in 2027 earnings per Share (EPS) of $8.39. Assigning a 20x P/E a number of to those earnings, which aligns with sector medians and historic ranges, provides us a share value of $167.80. This value goal implies a 76% upside to SWK from as we speak’s share value. Over three years, this boils right down to a 20.88% compounded annual development fee (CAGR) earlier than considering any dividend funds.

When taking a look at a handful of valuation ratios, SWK definitely trades on the low finish of historic averages. I listed a few of these ratios under and in contrast them to 5-year historic averages.

- Worth to Gross sales (TTM): 0.91 (33% under the five-year historic common of 1.35)

- Worth to Guide (TTM): 1.62 (32% under the five-year historic common of two.36)

- Worth to Money Move (TTM): 12.32 (38% under the five-year historic common of 19.80)

Based mostly on these assumptions and ratios, SWK appears extremely undervalued. In my view, the $80-$95 share value vary represents an incredible shopping for alternative. Any short-term seasonal weak spot must be taken benefit of.

Dangers

Whereas the turnaround story at SWK is undoubtedly starting to take form, any funding at all times has dangers. A few of these dangers embody however are usually not restricted to:

- Vital Leverage: SWK carries $7.68B in whole debt, and any slowdown in free money movement technology could considerably dampen steadiness sheet power

- Persistent Macro-Headwinds: Any uptick in inflation can have antagonistic results on SWK’s profitability, contemplating the numerous publicity to uncooked materials prices. As well as, a long-term restrictive rate of interest setting could proceed to place stress on the industrial and residential building market.

Conclusion

The chance to personal a improbable dividend king like Stanley Black & Decker won’t persist endlessly. Due to a once-in-a-lifetime COVID-19 Pandemic, traders now have the prospect to personal one of many world’s industrial crown jewels. Administration has targeted relentlessly on cost-cutting, profitability, and creating the optimum company construction to place SWK for long-term development. I’ll journey the coattails of this spectacular turnaround story and think about any short-term weak spot as a major shopping for alternative. Shopping for SWK as we speak is like shopping for a straw hat within the winter. Summer time will at all times come once more.

{kind=link}