gabetcarlson

Funding Overview

Elevance Well being (NYSE:ELV) will announce its Q1 2024 earnings subsequent Thursday, April 18th forward of the market open. After I final coated the corporate for In search of Alpha it was July 2020, and Elevance – then generally known as Anthem – inventory was buying and selling at $271 per share. I gave it a “Purchase” score.

At the moment, Anthem’s inventory value was being buffeted by pandemic headwinds, and a lot of the market believed the enterprise, offered these headwinds eased, was undervalued. That proved to be the case – Elevance inventory at present is price >$500 per share, and up almost 90% since my “purchase” name from 2020.

The place would possibly the share value be headed subsequent? On this earnings preview, I am going to attempt to reply that query by taking a deeper dive look “below the hood” of Elevance’s enterprise.

From Share Worth Peak To Current Day – Elevance Inventory, Climbs, Peaks, Plateaus

Elevance achieved its highest share value of almost $550 in October 2022, shortly after the corporate raised its full-year 2022 steering, citing sturdy efficiency, with Q3 revenues coming in at $39.6bn, and a medical profit ratio – which is basically healthcare prices paid divided by whole premiums acquired – of 87.2%.

One 12 months on from that, Elevance reported Q3 2023 revenues of $42.5bn – up 7% year-on-year – and a profit expense ratio of 86.8% – a 40 foundation level annual uplift. The corporate’s whole working margin fell barely year-on-year, nonetheless, from 6.1% throughout the primary 9 months of 2022, to five.6% throughout 2023 to the top of Q3. Its share value fell in worth to ~$450 per share.

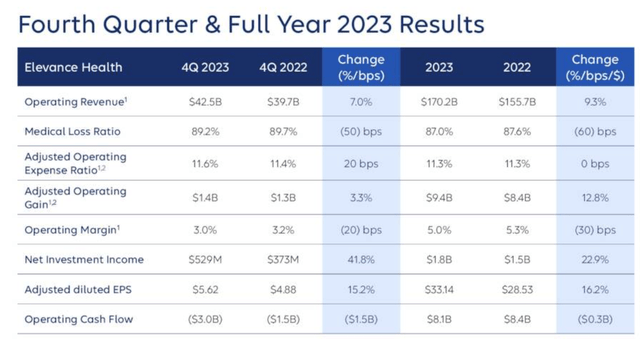

Administration blamed “medical value pattern on larger ranges of post-pandemic care”, for the working margin miss, but when we check out 2023 earnings as a complete, we will see a pattern of enchancment throughout quite a few metrics, together with the 60 foundation level enchancment in medical loss ratio, and better EPS of $33.14, albeit on an adjusted foundation.

Elevance 2023 earnings overview (Elevance presentation)

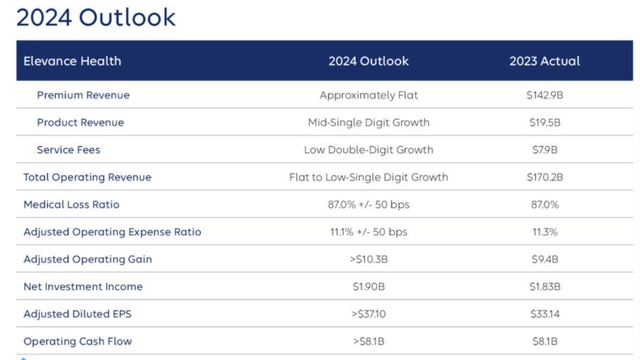

These outcomes – launched on the finish of January this 12 months – appeared to set off a mini-revival within the share value, which has climbed >$500 once more, regardless of a comparatively modest set of FY 2024 steering, as proven beneath:

Elevance 2024 steering (earnings presentation)

In equity to Elevance, administration is promising annual enchancment throughout many metrics – general revenues, web revenue, and earnings per share (“EPS’), and has been in a position to information for a similar medical loss ratio as final 12 months, at a time when most well being insurers are seeing margins shrink, owing to larger general medical prices.

Elevance Dodges Worst Of Medicare Benefit Charge Fallout

The worst hit a part of the medical insurance sector at current is Medicare Benefit. As soon as believed to be the way forward for healthcare for the over-65s, Medicare Benefit plans are administered by personal well being insurers on behalf of the federal government, and provide distinctive extras equivalent to dental care, and health applications.

Well being insurers are paid a price per plan administered and calculated by the Facilities for Medicaid and Medicare Providers (“CMS”), primarily based on historic prices of administering care in several elements of the US. The CMS additionally awards all plans a star score of 1-5, and presents extra bonuses to insurers primarily based on what number of of their members are in plans rated 4 stars and above.

As I wrote lately in a In search of Alpha observe on rival well being insurer Humana, which has large publicity to Medicare Benefit (“MA”):

Apparently, >30m People now have MA plans, which include extra advantages, equivalent to eye and listening to exams, health and dental plans, telehealth companies, meal advantages, and even acupuncture. With that mentioned the plans additionally include sure drawbacks, equivalent to not with the ability to go to physicians who’re “out of community,” and a rising pattern of claims being denied by insurers, or being settled solely after prolonged delays.

What is just not unsure is that historically, MA plans have been extremely profitable for well being insurers, and for brokers that promote healthcare plans. Analysis exhibits that gross margins for MA plans are twice that of unusual plans, whereas personal plans value the federal government – and, subsequently, the tax payer – on common 4% extra that normal plans.

The great factor for Elevance shareholders, now that the CMS is pushing again in opposition to MA price rises and trying to claw again tax payers cash – is that the corporate has a comparatively low publicity to MA. Of the 47m medical plan memberships on its books, solely ~2m are MA plans, and that quantity rose simply 4% year-on-year.

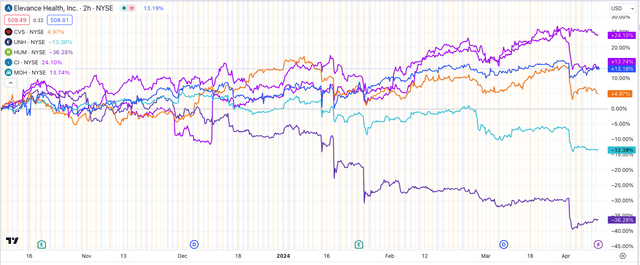

Share costs of various well being insurers in contrast (TradingView)

As we will see above, when the CMS introduced every week in the past that it could not be elevating MA plan cost charges from the three.7% stipulated earlier within the 12 months, most well being insurers’ inventory costs fell sharply. Elevance’s did fall, however not as considerably because the likes of Humana (HUM), CVS Well being (CVS), and UnitedHealth (UNH), who’ve the very best publicity to MA. Throughout the previous 6 months Elevance inventory is +13%, whereas CVS, UnitedHealth, and Humana inventory is +4.5%, -14%, and -36% respectively.

Primarily, the medical insurance market has to a sure extent been flipped on its head, with MA plans out of the blue squeezing margins, versus widening them. Elevance’s extra conventional and numerous vary of healthcare plans are permitting it to keep up and even enhance an already spectacular medical loss ratio, whereas e.g. Humana’s ratio climbs >90%, and CVS reported a soar from 85.5%, to 88.5%, in This fall 2023.

With that mentioned, Elevance – like Humana – nonetheless sees long run profit within the MA business, however is just not ready to undertake a “race to the underside”, providing decrease and decrease plan premiums as a way to bolster membership numbers. Elevance CEO and President Gail Boudreaux instructed analysts on the This fall 2023 earnings name with analysts:

Sadly, pockets of the Medicare Benefit market have remained hyper aggressive regardless of a tougher funding setting. Whereas our plans proceed to supply enticing and worthwhile advantages, we took intentional actions as a part of our 2024 bid technique to deal with product sustainability, and as such, we skilled greater-than-expected attrition in sure markets.

In consequence, we count on our Medicare Benefit membership to be roughly flat in 2024 on an natural foundation, however earnings to enhance. Importantly, value traits in our Medicare Benefit enterprise continued to develop as we anticipated, and we’re assured that the assumptions underlying our bids for 2024 are acceptable.

Elevance clearly retains an curiosity within the MA market, even when its 2m members are dwarfed by UnitedHealth’s ~9m members, and Humana’s ~6m – whereas CVS has grown to three.3m members, including >500k new members within the 2024 open enrollment interval which has lately ended. Elevance could have to enhance the extent of service it’s providing, nonetheless – based on Elevance’s 2023 annual report / 10K submission:

Based mostly on our membership at September 1, 2023, 34% of our Medicare Benefit members have been in plans with 2024 Star scores of a minimum of 4.0 Stars, in comparison with 64% of our Medicare Benefit members being in plans with 2023 Star scores of a minimum of 4.0 Stars primarily based on our membership at September 1, 2022.

This transformation in our 2024 Star scores is predicted to influence our Star high quality bonus funds and plan degree rebates starting in 2025. We count on a discount to our 2025 working income of roughly $500 million, web of offsets from contracting provisions.

Elevance – After A Yr Of Progress, A Yr Of Consolidation Beckons

The market is educated to imagine that Elevance is a traditional blue chip, dividend paying healthcare large whose share value is immune to volatility, making shopping for much like shopping for a fixed-interest safety, however that may not be solely true.

At present value, Elevance’s dividend of $1.62 per share presents a yield – at present share value of $509 – of simply 1.3%. As a further fillip to buyers, the corporate accomplished $2.7bn of share repurchases in 2023, though it appears there aren’t any extra applications ongoing presently.

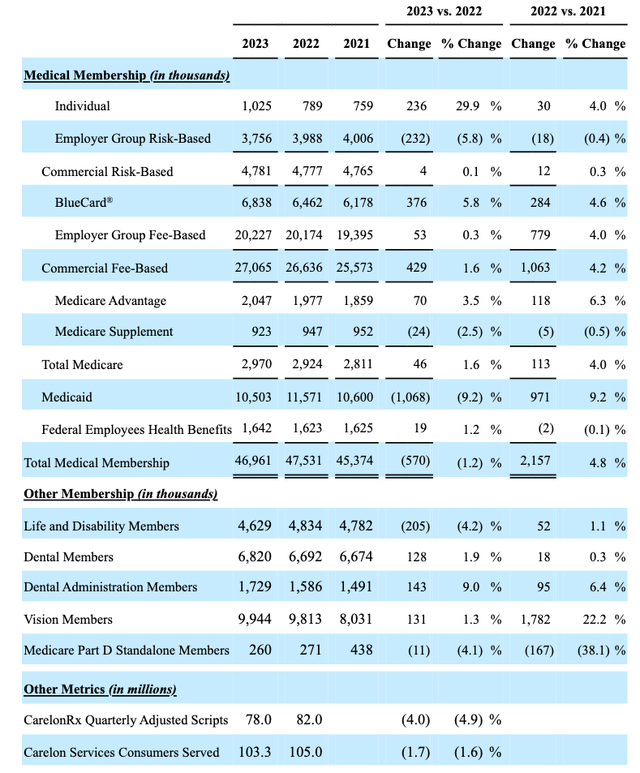

Elevance membership by class (Elevance 10K submission 2023)

As we will see above, Elevance has some 27m business, price primarily based members, ~3m Medicare members, and 10.5m Medicaid members, nonetheless revenues reported in 2023 have been $43.3bn from business, $35bn from Medicare, and $56.6bn from Medicaid, with Federal Workers Well being Profit (“FEHB”) buyer revenues contributing $13.64bn.

On high of those revenues, which come to $148.6bn, Elevance provides revenues from its Carelon Rx division, which “markets and presents pharmacy companies to our affiliated well being plan clients”, arranging 78m scripts in 2023, the corporate says (down 4% year-on-year), and Carelon Providers, which presents a “broad array of healthcare associated companies and capabilities to inside and exterior clients”, and served 103m clients in 2023 – down ~1.7% year-on-year.

Working revenues grew by >9% year-on-year in 2023, to $170.2bn, with the Well being Advantages phase rising working margin from 4.3% in 2022, to 4.6% in 2023, Carelon RX’s margin reducing to five.8%, from 6.5% (probably because of authorities stress on drug pricing negotiations), and Carelone Providers’ margin rising to 4.8%.

Whereas Elevance is guiding for an working achieve of >9% year-on-year in 2024, it is usually anticipating membership numbers to shrink general, to 45.8 – 46.6m members. Administration expects Medicaid membership to fall by ~930k members in 2024 because of administrative points brought on by “modifications in our footprint” (though there may be confidence these members will return in time), whereas business membership is predicted to develop by >750k, with Medicare Benefit membership remaining flat.

In abstract, 2023 was a fairly robust 12 months for Elevance, with good and unhealthy parts. On the plus aspect, the corporate has been in a position to deal with constructing out its technique with Carelon, and altering its general reporting technique to place Carelon on the centre of its operations. It has delivered working income development and elevated its medical threat ratio margin.

On the extra destructive aspect, it has misplaced members year-on-year, and been buffeted barely by points round Medicaid enrollment and Medicare Benefit plan pricing.

Waiting for 2024, administration has referred to this 12 months as a “reset 12 months”, with CEO Boudreaux telling analysts on the This fall 2023 earnings name:

We anticipate that our well being advantages enterprise goes to proceed to develop in 2025 after a reset 12 months in 2024. We must always see an accelerated influence to that development, which is able to drive income for Carelon.

I feel we really feel that we have positioned our enterprise very prudently and that the stability and resilience of our enterprise and our earnings energy of our well being advantages in Carelon collectively offers us plenty of confidence in our capability to realize our long-term targets.

Based on its This fall 2023 incomes presentation, the corporate’s strategic priorities are centered on:

margin restoration of our business risk-based enterprise, the strategic repositioning of our Medicare Benefit plan choices in sure markets, continued penetration of Carelon Providers capabilities in our well being plans, and transformation of our value construction.

Concluding Ideas – Would I Make Elevance A “Purchase”, “Promote”, or “Maintain” Forward of Q124 Earnings?

As mentioned, by most measures Elevance loved a robust 2023, outcomes clever, throughout most metrics aside from general membership development. Whereas memberships could fall once more in 2024, administration is assured that development is feasible in 2025, and is positioning itself accordingly, whereas backside line enchancment has been promised for 2024 – administration’s steering for EPS of $37 in 2024 interprets to a ahead value to earnings ratio of ~14x.

In the meantime, the operational focus can be on enhancing the business and medicare parts of the enterprise, and utilizing Carelon to optimise margins and convey members again.

With its restricted publicity to MA plan markets, Elevance could carry out higher in 2024 than a number of friends with the next publicity, equivalent to Humana, CVS Well being, and UnitedHealth, though I’d argue that firstly, this diminished publicity to turbulent MA markets is already priced in, and longer-term, it is clear that Elevance will re-focus on MA when it feels it has its technique proper.

Elevance’s share value, after making stable beneficial properties from 2020 to the start of 2023, remained flat or down for almost all of final 12 months, nonetheless its present share value of $514 is near an all-time excessive.

Fascinated with Elevance’s present market cap of ~$120m, it’s near 4x the worth of Humana’s $38.5bn market cap, but Humana’s revenues in 2023 have been $106m, in comparison with Elevance’s $171bn, and its web revenue ~$2.5bn, in comparison with Elevance’s ~$6bn. In the meantime, CVS Well being’s market cap of $93bn is decrease than Elevance’s, but its revenues of $358bn have been >2x larger than Elevance’s, and web revenue of $8.35bn additionally considerably larger.

In brief, the medical insurance market supplies a considerably confused image at the moment, with an overriding deal with what is going on inside the MA market influencing present inventory costs and valuations arguably extra so than precise efficiency and administration steering.

Satirically, my suspicion is that this situation could favour corporations which have the next publicity to MA, and whose inventory costs have already undergone a extra important correction, than corporations like Elevance whose core focus lies elsewhere.

Elevance will probably present compelling profitability and income development in 2024, preserve margins and probably obtain EPS of $37 per share on a non-GAAP foundation, however will this be sufficient to drive share value beneficial properties?

Wanting previous these numbers, the dearth of membership development in 2024, together with falls in Medicaid and flat MA development, could injury Elevance’s share value and valuation in 2024 because the market digests a 12 months of consolidation, not development.

As such, with a dividend yielding <1.5%, and having skilled a fast restoration from the current market sell-off associated to MA plan pricing, but set for a probably underwhelming 12 months, if I have been holding Elevance I would be tempted to contemplate promoting, and shifting my cash to an organization that’s positioned to do some bit extra with it in 2024.

I haven’t got any doubts that Elevance has the capabilities to realize the next valuation and maybe a share value >$600 at some point, however throughout a 12 months of consolidation, it might be affordable to additionally count on a 12 months of downward share value drift, with earnings not fairly residing as much as the premium value Elevance inventory now trades at.

{kind=link}