nzphotonz

Let’s attempt to check out Trump Media & Know-how Group Corp (NASDAQ:DJT) inventory out of the context of my (or your) opinion on the forty fifth. U.S. President. It will be tough, however isolating DJT from its founder is vital to understanding the expansion prospects of the inventory, which has generated plenty of buzz right here on Searching for Alpha after the SEC permitted Trump Media’s merger with SPAC Digital World in mid-February 2024.

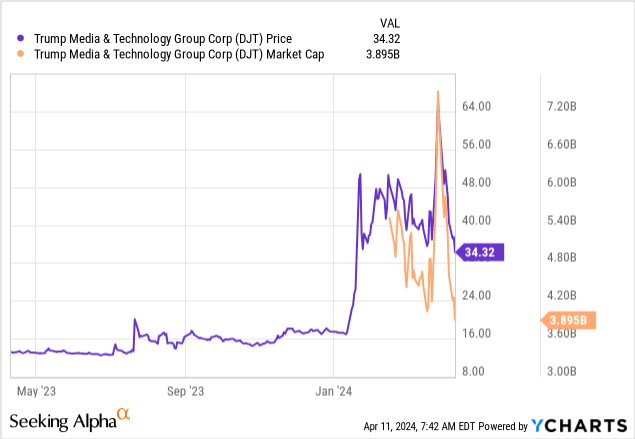

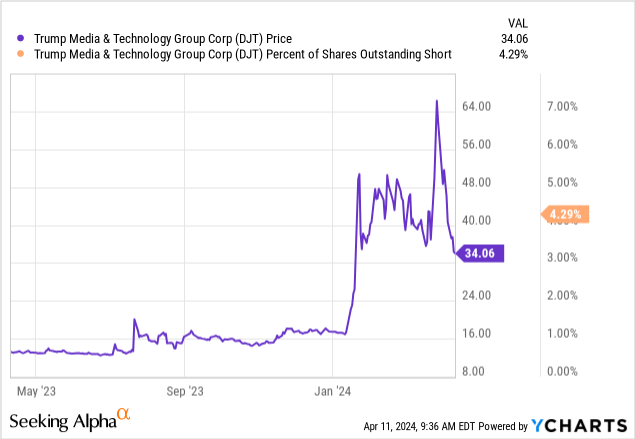

Since then, as anticipated, the inventory has proven very excessive volatility: At one level, its market capitalization was over $7 billion, however by in the present day, because the hype surrounding DJT died down, its market capitalization has fallen to ~$3.9 billion:

What precisely do buyers pay such large quantities of cash for?

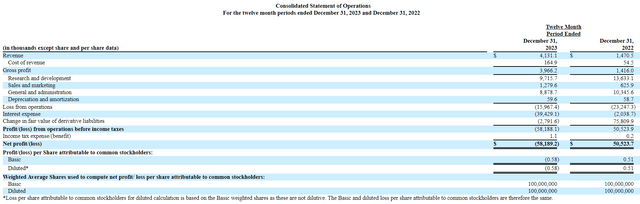

Trump Media elevated its gross sales by 180% in comparison with the earlier 12 months, however in absolute phrases, gross sales amounted to solely $4.1 million. I wasn’t incorrect: the ~$4 billion firm solely generated $4.1 million within the 2023 monetary 12 months. Already at this level, any debate of the corporate’s present valuation is proving untenable: DJT appears ridiculously overvalued to me. However what instantly strikes me once I first analyze DJT’s earnings assertion is that the administration itself would not appear to see any sense within the firm’s future improvement. I draw this conclusion from the decline in R&D expenditure by greater than 30% YoY. On the similar time, curiosity expense exceeded income by 8.5x in FY2023 – the primary time I’ve seen the inventory develop by 278.70% YoY with such indicators.

SEC, DJT’s latest 10-Okay

Organizing a digital enterprise like Fact Social – DJT’s most essential asset in the intervening time – requires large investments in analysis and improvement that haven’t been made to this point. One may assume that it will change in 2024, as the corporate now has way more scope for versatile administration because of its itemizing on the most important inventory exchanges. However, I understand that these alternatives for the corporate will solely come by way of dilution – not a very good factor for individuals who need to maintain DJT shares for quite a lot of buying and selling days.

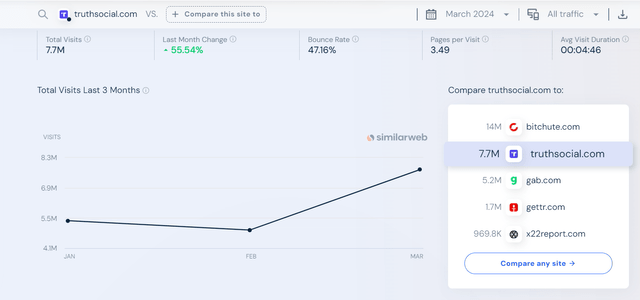

If you happen to take a look at the customer numbers for Fact Social on SimilarWeb, it seems at first look as if the web site is rising fairly quickly: final month it recorded a 55.5% enhance in complete visits. On nearer inspection, nevertheless, you’ll be able to see that this metric fell from January to February and the primary development passed off in March. I attribute this to the truth that DJT’s web site was within the public eye as a result of all of the information that the corporate acquired permission from the SEC. That stated, it is unlikely to be an actual inflow of stay customers – I feel these are simply individuals who occurred to come back to the location, or analysts like myself who’ve tried to review DJT’s product.

SimilarWeb, Fact Social

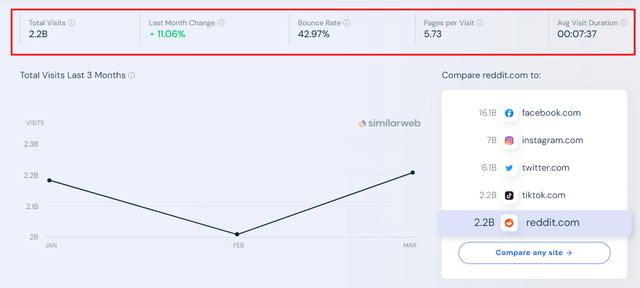

Take note of what number of pages the person views throughout a go to and the way lengthy a mean go to takes: 3.49 pages/go to and 4 minutes and 46 seconds, respectively. Simply evaluate that to Reddit (RDDT), which additionally not too long ago grew to become a full-fledged public firm, solely by way of a basic IPO:

SimilarWeb, Reddit

Site visitors can also be down from January to February, however a) RDDT’s site visitors exceeds Fact Social’s by an element of ~285, and b) common web page visits are considerably higher when it comes to the time spent on the location and the variety of pages visited. Moreover, RDDT’s market capitalization is only one.75 occasions that of Fact Social.

My elementary evaluation tells me that DJT could possibly be value $206 million at greatest if we assume that gross sales enhance 5x this 12 months and we use a price-to-sales ratio of 10x (that is a 48% premium to RDDT’s forwarding a number of). Which means that the elemental draw back potential when it comes to valuation is 94.7% of the present DJT value.

On the similar time, I do not see a lot sense in hoping for a brief squeeze with a brief curiosity of 4.29% as of in the present day. That’s the reason, even speculatively, DJT inventory doesn’t appear to be the perfect choose, in my view.

So to summarize my article in the present day, let me state that DJT has nothing excellent if we disregard your entire political context surrounding this inventory. The corporate’s enterprise prospects are doubtful as a result of its unit financial metrics are poor (in comparison with its closest opponents like Reddit), it lacks R&D focus and there is merely an excessive amount of competitors within the social networking market. On the similar time, DJT inventory is priced to perfection – at sure moments, compared to RDDT or compared to the gross sales volumes, I used to be amazed. My comparatively optimistic valuation findings counsel a draw back potential of ~94.7% in comparison with the present inventory value – not together with potential dilution.

Based mostly on the sum of all of the components analyzed, I really feel compelled to subject a “Promote” score in the present day.

Thanks for studying!

{kind=link}