Klaus Vedfelt/DigitalVision by way of Getty Pictures

In our final protection of Ares Industrial Actual Property Company (NYSE:ACRE) we gave it a “Promote” score. What was uncommon about our stance is that we did it within the face of a declining inventory. Usually, we have a tendency to maneuver our scores in the other way of the inventory value. As excellent news will get priced in and shares transfer greater, we transfer from “Purchase” to “Maintain”. Conversely, when shares tank, we acknowledge that unhealthy information is probably getting priced in and transfer from “Promote” to “Maintain”, and even to a “Purchase”. After we wrote about ACRE, it had already dropped 25% from current highs in a short time. Therefore, staring with a “Promote” was uncommon. Our rationale although was that the e-book worth would get killed within the months forward, and it additionally bought a scary score for its dividend security.

ACRE would get an “Excessive” stage of hazard of a distribution minimize on our proprietary Kenny Loggins Scale.

Writer’s Scale

This score signifies a 50-75% chance of a distribution minimize within the subsequent 12 months. We charge this a Promote.

Supply: Dividend Minimize Extremely Possible In 2024

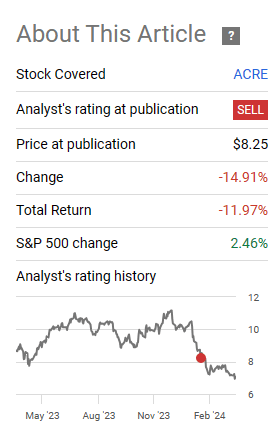

It’s uncommon for calls to work this effectively, and ACRE minimize its distribution lower than 12 days after the article. Inventory efficiency has been predictable in mild of that with the earnings buyers fleeing.

In search of Alpha

We do not assume that is achieved and imagine the second spherical of troubles is across the nook. Let’s go over why.

The Setup

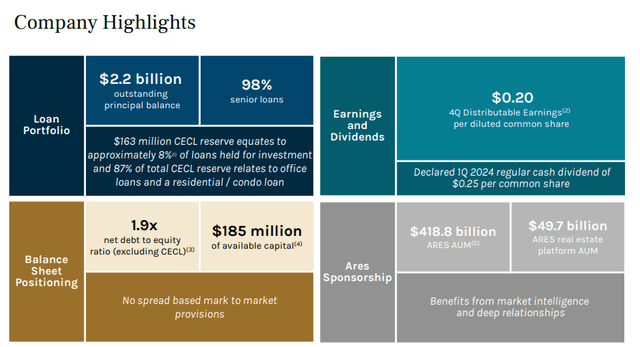

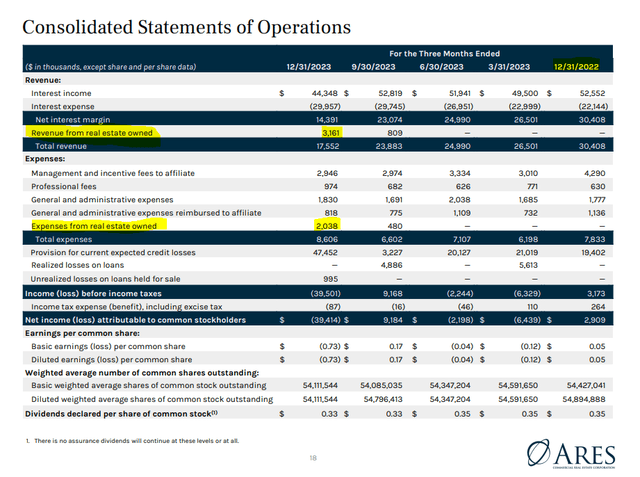

The primary slide within the investor deck tells you numerous. The distributable earnings had been simply 20 cents a share, and the lowered distribution was nonetheless 25% greater than that at 25 cents a share.

ACRE This fall-2023 Presentation

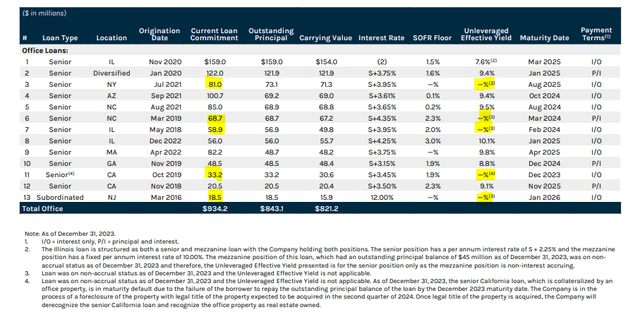

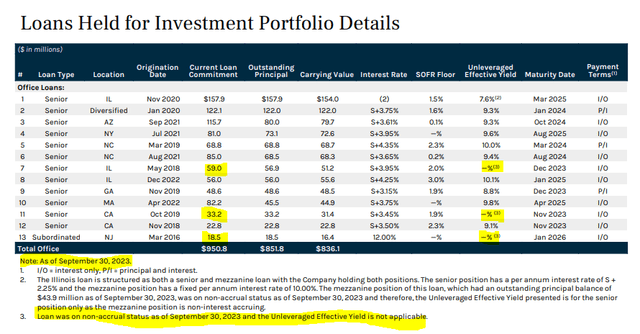

The $163 million CECL reserve sounds spectacular till you attain the truth that it’s simply 8% of loans. 4 loans went into non-accrual standing within the quarter. At first look you may assume that these 4 loans had been all for the workplace sector. In any case, you will discover 5 loans on non-accrual standing right here.

ACRE This fall-2023 Presentation

However that isn’t the case. Out of the 5 loans above, 3 had been already in non-accrual standing on September 30, 2023.

ACRE Q3-2023 Presentation

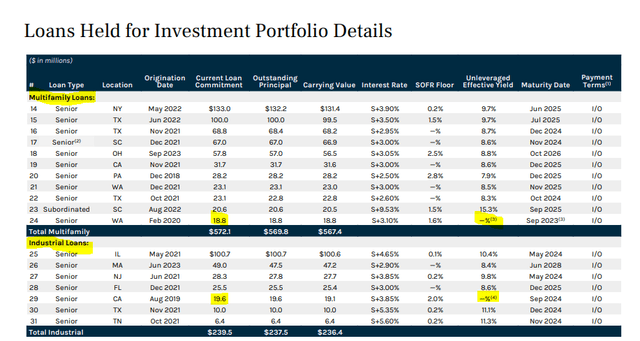

So we had two workplace loans and one mortgage every from Multifamily and Industrial segments go into non-accrual this quarter.

ACRE This fall-2023 Presentation

Our greater level is that there’s a lot extra room for issues to go unhealthy within the workplace sector. Do not assume the worst is priced in. 5 out of the 13 loans are on non-accrual standing. That itself ought to present you the mix of market stress and underwriting requirements.

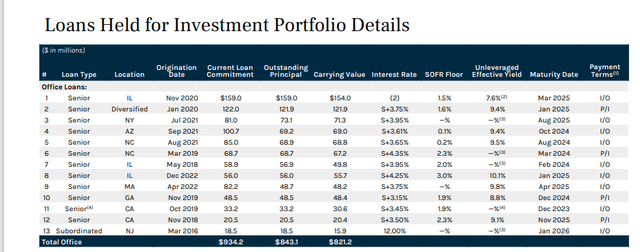

ACRE This fall-2023 Presentation

The 4 largest loans right here, that are paying as per the settlement, all mature within the subsequent 12 months. We expect the perfect case can be one default right here and the worst case can be all 4 defaulting. These numbers could sound excessive however we’re simply utilizing the present market state and never even assuming the deterioration continues. Current work exhibits about 44% of workplace loans will probably default and primarily based on ACRE’s efficiency so far, we predict they are going to do worse.

Constructing on the work of Jiang et al. (2023) we develop a framework to research the consequences of credit score danger on the solvency of U.S. banks within the rising rate of interest atmosphere. We concentrate on industrial actual property (CRE) loans that account for about quarter of property for a median financial institution and about $2.7 trillion of financial institution property within the mixture. Utilizing loan-level information we discover that after current declines in property values following greater rates of interest and adoption of hybrid working patterns about 14% of all loans and 44% of workplace loans look like in a “destructive fairness” the place their present property values are lower than the excellent mortgage balances. Moreover, round one-third of all loans and nearly all of workplace loans could encounter substantial money circulate issues and refinancing challenges.

Supply: SSRN

What Is Distributable Earnings?

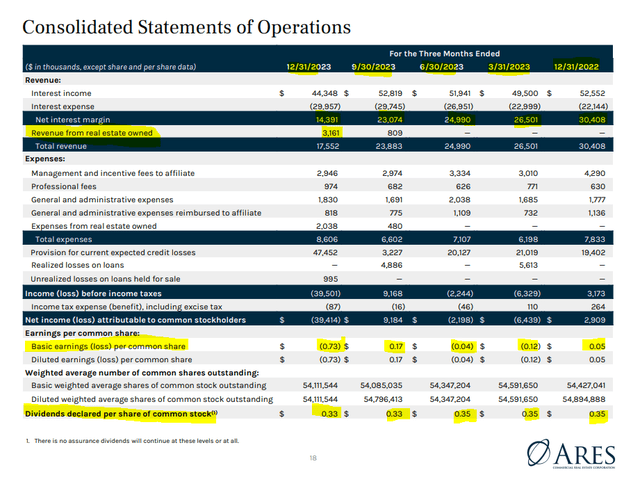

We doubt this is able to have the identical ringtone reputation because the Haddaway music, however the “Child do not harm me” half will probably be equivalent. ACRE’s buyers are struggling merely as they’ve targeted on distributable earnings and ignored the GAAP image. Sure, GAAP might be deceptive, however the skill to tell apart when it’s telling the reality and when it’s mendacity is what makes a profitable investor. Right here, GAAP was exhibiting you quarter after quarter of poor earnings, and also you ignored it. Internet curiosity margin, which is extraordinarily related whether or not or not you want GAAP, can be down 50% over 12 months.

ACRE This fall-2023 Presentation

That is the place bulls will step in with smoke and mirrors. The constructive spin? ACRE now owns actual property and is getting income from that. We’ve highlighted that portion above as effectively. So the primary bull promoting level when ACRE was $14 was that it’s nice that it doesn’t personal actual property. However now at half the worth, it’s nice that it does. Okay.

That possession income isn’t that nice both, by the best way. It comes with a whole lot of bills.

ACRE This fall-2023 Presentation

How This Shakes Out

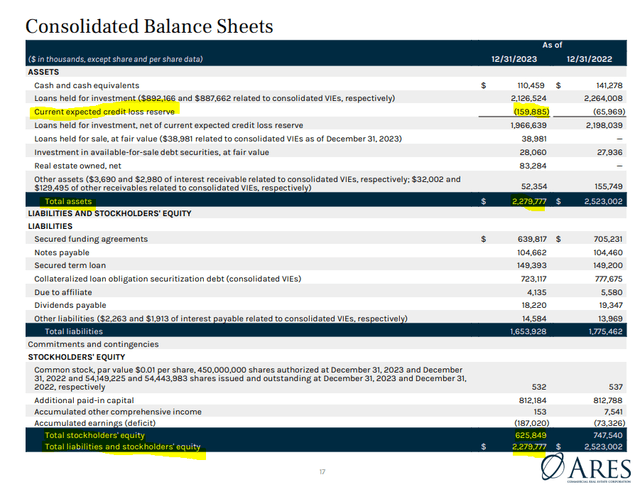

The present stability sheet remains to be means too leveraged for the stress within the workplace sector. This consists of the adjustment for the CECL reserves. $625 million of fairness is buffering $2.27 billion of property.

ACRE This fall-2023 Presentation

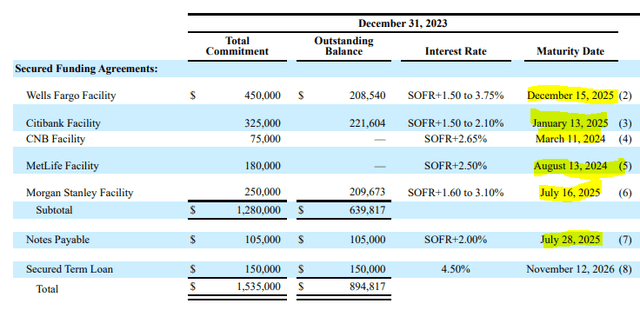

The subsequent 18 months will probably be when the troubles will probably be full catalyzed. That is 18 months, not 18 weeks, 18 days or 18 minutes after this text is revealed. So preserve time horizons in thoughts. On the similar time, a whole lot of ACRE’s debt comes due.

10-Ok

These all had been loaned at far happier instances and are available renewal, we’d anticipate a really completely different pound of flesh to be extracted.

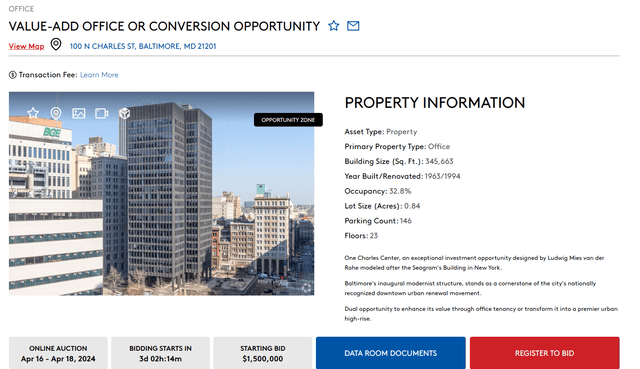

For the intrepid bulls, should you assume workplace property are low-cost and also you want to bid, right here is one for you.

Ten-X

Beginning bid is $4 per sq. foot. That’s 99% off the alternative price.

The common building price for industrial workplace buildings varies relying on the dimensions and variety of flooring. The common price is $313 per sq. foot for a single-story workplace constructing, $562 for a mid-rise and $660 for a high-rise within the U.S. A number of components trigger the worth to extend for multi-story workplaces, together with dearer constructing supplies, stricter constructing codes and better labor prices.

Supply: Huge Rentz

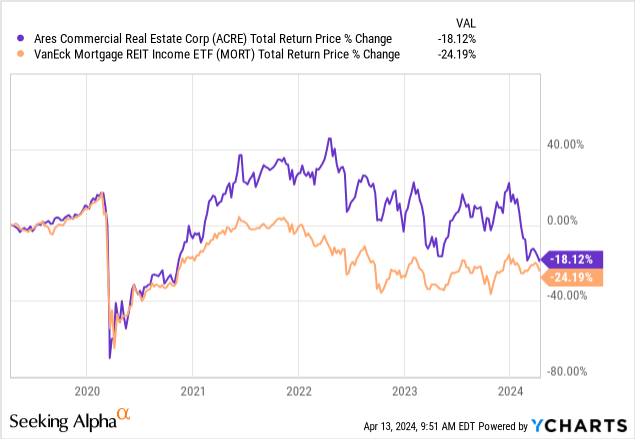

So there are some real issues on this sector, and anybody holding on to the pre-2020 mannequin probably will battle. Positive, some REITs will make it and a number of the high buildings will lose much less worth than others. We cannot all go to WFH mannequin. However there’s a cause that ACRE’s whole return together with distributions is destructive 18% during the last 5 years.

Nicely, two causes truly. The primary is that it’s a mortgage REIT and people are typically the worst performers over longer time frames. We threw in VanEck Mortgage REIT Revenue ETF (MORT) for comparability to show our level.

The second is, after all, that we imagine ACRE remains to be too uncovered to workplace and that may affect issues down the road. ACRE would nonetheless get an “Excessive” stage of hazard (50%-75%) of one other distribution minimize on our proprietary Kenny Loggins Scale.

Writer’s Scale

We proceed to charge this a Promote.

{kind=link}