Up to date on April seventeenth, 2024 by Bob Ciura

The Dividend Aristocrats are among the finest dividend shares an investor will discover. These are corporations within the S&P 500 Index, with 25+ consecutive years of dividend will increase.

We consider the Dividend Aristocrats are among the many highest-quality dividend development shares round. For that reason, we created a downloadable spreadsheet of all 68 Dividend Aristocrats, together with vital metrics equivalent to price-to-earnings ratios and dividend yields.

You’ll be able to obtain the Excel sheet of all 68 Dividend Aristocrats by clicking the hyperlink under:

Disclaimer: Certain Dividend will not be affiliated with S&P International in any approach. S&P International owns and maintains The Dividend Aristocrats Index. The data on this article and downloadable spreadsheet is predicated on Certain Dividend’s personal assessment, abstract, and evaluation of the S&P 500 Dividend Aristocrats ETF (NOBL) and different sources, and is supposed to assist particular person traders higher perceive this ETF and the index upon which it’s based mostly. Not one of the data on this article or spreadsheet is official information from S&P International. Seek the advice of S&P International for official data.

Annually, we assessment the entire Dividend Aristocrats. The following inventory within the collection is an insurance coverage dealer large, Brown & Brown Inc. (BRO). BRO won’t be a well-recognized inventory for many traders, but it surely has actually earned its place on the listing.

BRO has now elevated its dividend for 30 consecutive years. This text will focus on the corporate’s enterprise mannequin, development outlook, and whether or not we view it as a purchase as we speak.

Enterprise Overview

Brown & Brown Inc. is a number one insurance coverage brokerage agency that gives threat administration options to each people and companies, with a give attention to property & casualty insurance coverage. Brown & Brown has a notably excessive stage of insider possession.

The corporate employs about 14,500 individuals and generated about $3.6 billion in income final 12 months. It operates by way of 4 segments: Retail, Nationwide Packages, Wholesale Brokerage, and Providers.

The corporate has been diversifying its enterprise phase all through the years. Doing this enables the corporate to not be 100% depending on one enterprise phase. Thus, these segments have carried out very properly in opposition to their friends and have allowed BRO to realize “better of breed” standing in its business.

Brown & Brown’s aggressive benefit comes from its willingness to execute small and frequent acquisitions. This growth-by-acquisition technique provides the corporate an everlasting alternative to proceed rising its enterprise for the foreseeable future.

Progress Prospects

Brown & Brown has a outstanding development observe document that features a decade-long compound annual earnings development price of greater than 14%. The corporate’s e-book worth per widespread share has grown at an analogous price, increasing at ~11% per 12 months during the last ten years.

The expansion technique is each easy and sustainable. Through the years, the corporate has actively acquired smaller insurance coverage brokerage corporations and built-in them into its bigger working base.

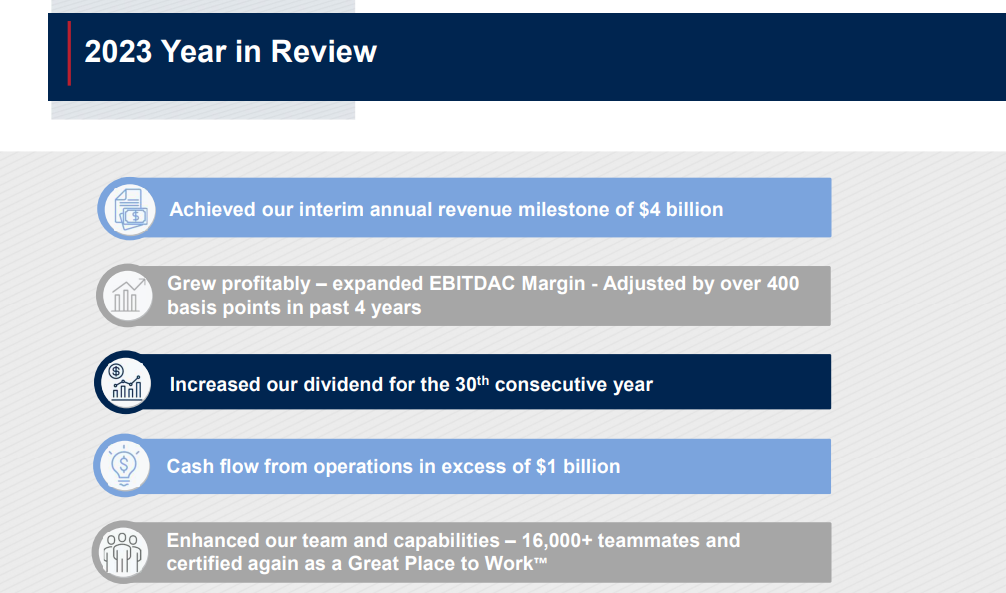

Brown & Brown posted fourth-quarter and full-year monetary outcomes on January twenty second, 2024, and outcomes have been fairly sturdy as soon as once more. The corporate beat earnings-per-share by $0.05, coming in at $0.58 per share.

Income soared 14% increased year-over-year to $1.03 billion, and beat expectations by $45 million. Commissions and costs rose by 12.4% year-over-year, whereas natural income was up 7.7%, which excludes the impression of acquisitions and divestitures.

Earnings earlier than taxes got here to $355 million, up 83% year-over-year. Earnings earlier than taxes margins rose to 34.6% from 21.5%. On an adjusted foundation, working revenue was $318 million, up 12% year-over-year. Adjusted working margin fell barely from 31.4% of income to 31.0%.

Supply: Investor Presentation

We begin 2024 with a powerful development estimate of $3.10 in earnings-per-share, as the corporate continues to see strong income development that can be driving increasing margins.

We additionally anticipate BRO to generate 9% annual earnings-per-share development over the following 5 years.

Aggressive Benefits & Recession Efficiency

Brown & Brown’s aggressive benefit comes from its willingness to execute small and frequent acquisitions. This growth-by-acquisition technique provides the corporate an everlasting alternative to proceed rising its enterprise for the foreseeable future.

BRO can be modestly recession-resistant. For instance, BRO’s aggressive benefits permit it to keep up constant profitability every year, even throughout recessions.

BRO’s earnings-per-share through the Nice Recession are under:

- 2007 earnings-per-share of $0.68

- 2008 earnings-per-share of $0.59 (13% decline)

- 2009 earnings-per-share of $0.54 (8% decline)

- 2010 earnings-per-share of $0.56 (4% improve)

Additional, through the COVID-19 pandemic, earnings grew from $1.40 per share in 2019 to $1.67 per share in 2020. This represents a rise of 19% year-over-year.

Valuation & Anticipated Returns

Based mostly on our anticipated EPS of $3.10 for 2024, BRO inventory trades for a price-to-earnings ratio of 26.1, utilizing as we speak’s inventory worth of ~$81. BRO held a mean price-to-earnings ratio of 23 over the previous 10 years.

At this time’s a number of is modestly above our honest P/E of 24, implying shares seem considerably overvalued at their present worth ranges.

If the inventory experiences a decline within the valuation a number of to our honest P/E of 24.0, annual shareholder returns could be decreased by 1.7% yearly over the following 5 years.

Fortuitously, earnings development and dividends will positively impression future returns. First, we anticipate the corporate to develop earnings-per-share by 9% per 12 months by way of 2029.

The inventory additionally has a dividend yield of 0.6%. Placing all of it collectively, a breakdown of our anticipated future returns is as follows:

- 9.0% anticipated earnings-per-share development

- 0.6% dividend yield

- -1.7% a number of contraction

On this projection, complete annualized shareholder returns might attain 7.9% by way of 2029. It is a passable anticipated price of return for this firm, however one that’s restricted by the inventory’s excessive valuation.

Ultimate Ideas

BRO has endured quite a lot of challenges over the previous decade, together with the Nice Recession of 2008-2009 and the coronavirus pandemic of 2020. And but, it continued to lift its dividend every year. Only a few corporations have this capacity, which makes this firm a uncommon dividend development inventory.

BRO has a management place in its insurance coverage business and sturdy aggressive benefits. These components have the corporate positioned for development in future years, making it extremely possible that the corporate will proceed to extend its dividend.

The corporate is a high-quality enterprise and a dividend development firm, and whereas the inventory will not be essentially overvalued, its wealthy a number of averts it from incomes a purchase score from Certain Dividend right now. Accordingly, we now have assigned the inventory a maintain score at its present worth.

Moreover, the next Certain Dividend databases comprise probably the most dependable dividend growers in our funding universe:

In case you’re on the lookout for shares with distinctive dividend traits, take into account the next Certain Dividend databases:

The foremost home inventory market indices are one other stable useful resource for locating funding concepts. Certain Dividend compiles the next inventory market databases and updates them month-to-month:

Thanks for studying this text. Please ship any suggestions, corrections, or inquiries to assist@suredividend.com.

{kind=link}