William_Potter/iStock through Getty Photos

Based in 1993, Affiliated Managers Group (NYSE:AMG) inventory presents an affordable entry level for traders that imagine in the way forward for energetic administration. The corporate advantages from its diversified property beneath administration by means of three dozen boutique funding administration companies, its strong stability sheet with cheap leverage, and instructions a protracted historical past of returning extra capital to traders by means of inventory buybacks, together with low valuation multiples.

I final coated the corporate in July 2016 and replace my evaluation on this article.

Firm Overview

Affiliated Managers Group is a worldwide asset administration agency with $673 billion in property beneath administration as of December 31, 2023. AMG companions with and sometimes takes fairness takes in boutique funding administration companies (“Associates”) that concentrate on energetic administration, and in return of asset-based administration charges paid by Associates, AMG supplies Associates with strategic, enterprise growth, operational, and capital help.

Based in 1993, and with greater than 500 methods managed by greater than 35 Associates throughout liquid options, personal markets, multi-asset, and differentiated fairness methods, AMG’s enterprise is diversified by asset class, shopper sort, and geography. The next graph reveals the composition of AMG’s property beneath administration as of December 31, 2023.

AMG Investor Relations

Basic Evaluation

The next long-term chart presents AMG’s income and internet revenue on a trailing-twelve-month foundation all through the final three a long time:

My three key takeaways from the above chart are:

- AMG’s income and internet revenue developments have proven indicators of cyclicality with materials declines throughout earlier recessions;

- Though AMG’s enterprise grew outstandingly within the three a long time by means of 2015, the corporate’s income progress has stalled and actually declined from 2016 by means of the newest interval; and

- AMG has typically achieved constructive and rising earnings, besides for 2 briefs durations in 2009 and 2019.

AMG could finance its progress by taking fairness stakes in boutique funding administration companies by issuing debt. The next graph illustrates AMG’s complete debt stability and stability sheet leverage, as measured by complete debt to property ratio, all through the corporate’s three-decade publicly traded historical past:

I notice that, though AMG’s complete debt stability has continued to extend, the corporate’s debt to asset ratio has remained comparatively unchanged all through the final decade and is at an affordable degree of 28 % in the present day.

Comparable Firm Evaluation

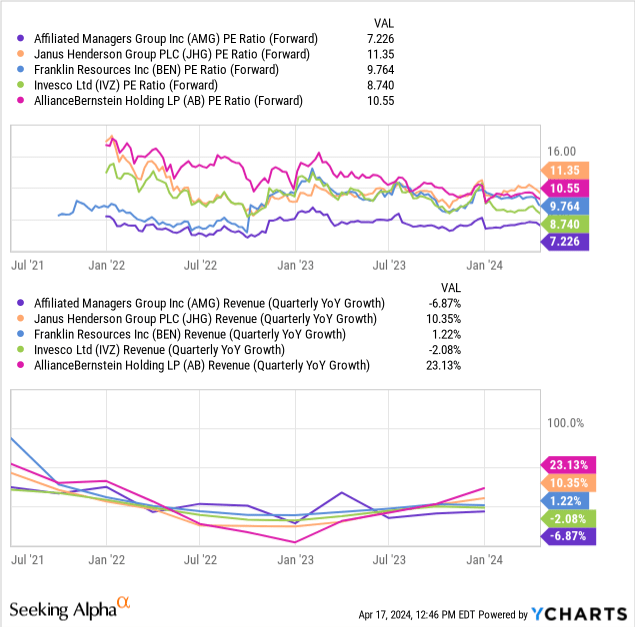

Based mostly on AMG’s enterprise and its dimension, I chosen the next firms for the comparable firm evaluation: Janus Henderson Group (JHG), Franklin Assets (BEN), Invesco (IVZ), and AllianceBernstein Holding (AB).

The next chart consists of the Peer Group’s price-to-earnings on a forward-looking foundation in addition to the businesses’ quarterly income progress on a year-over-year foundation:

I notice that AMG’s valuation a number of of seven.2x represents a 26 % low cost to the median a number of of its peer group, 9.8x. AMG may very well be buying and selling at a reduction to its peer group for plenty of causes, together with however not restricted to shifting investor preferences, issues about future progress, underlying affiliate efficiency, a slowdown in new deal exercise, debt ranges, or different causes. Though AMG has skilled declining income progress in current durations, its income progress charge has trended typically in-line with its peer group within the final three years. Additional, I notice that AMG’s stability sheet leverage represents the media of its peer group and stays at an affordable degree of 28 %, as the next graph reveals:

Lastly, I notice that AMG returns capital to traders by means of inventory buybacks, in distinction to its Peer Group which have returned capital to their traders primarily by means of dividend funds:

Subsequent, I focus on the corporate’s honest worth and assign my worth goal.

Truthful Worth and Value Goal

I imagine the AMG inventory ought to commerce at a price-to-earnings a number of close to the median of its peer group for the next causes:

- Comparable Fundamentals: AMG’s stability sheet and revenue assertion fundamentals align with these of its friends, suggesting comparable danger profile and progress potential;

- Income Stability: AMG’s asset-based administration charges derived from a various group of Associates supplies a degree of stability throughout risky market circumstances;

- Earnings Consistency: Aside from transient durations in 2009 and 2019, AMG’s observe document of constructive earnings highlights its capability to navigate difficult market circumstances; and

- Shareholder Focus: AMG demonstrates its shareholder focus by means of a comparatively excessive and constant inventory buyback yield.

Assumptions and Calculations

- I recognized a peer group primarily based on suggestions by the Searching for Alpha Premium Software and my very own expertise within the trade;

- I calculated the typical and the median of the peer group’s price-to-earnings multiples to be 9.41x and 9.76x, respectively; and

- I chosen a price-to-earnings a number of applicable for AMG, 9.6x, and utilized it to AMG’s projected earnings per share of $22.11 for 2024.

Based mostly on AMG’s valuation a number of low cost to the peer group’s median price-to-earnings ratio, I assign a BUY score with a $212 per share worth goal, which represents 33 % upside from the present worth of $159 per share.

Dangers To My Evaluation

Though BlackRock (BLK), the worldwide asset administration behemoth with $10 trillion in property beneath administration as of December 31, 2023, is primarily targeted on passive administration by means of its iShares suite of ETF merchandise, BlackRock’s super progress since 2008 has coincided with the numerous slowdown within the progress of funding administration companies targeted on energetic administration, together with AMG:

The first danger to AMG is the continued, fast progress of passive funding administration merchandise, comparable to ETFs, which has created a difficult enterprise setting for companies comparable to AMG that focuses on energetic administration. The next chart illustrates the persistent outflows that energetic administration companies general have skilled since 2007:

Morningstar

Second largest danger to AMG traders is the efficiency observe document of the Associates doubtlessly deteriorating and resulting in giant outflows, however I imagine the diversified nature of AMG’s Associates and the corporate’s property beneath administration materially mitigates this danger.

Conclusion

With its diversified property beneath administration by means of three dozen Associates, lengthy historical past of returning extra capital to its traders by means of inventory buybacks, and at the moment low valuation multiples, AMG inventory presents an affordable entry level for traders that imagine in the way forward for energetic administration. I charge the inventory BUY with a $212 per share worth goal.

{kind=link}