Up to date on April nineteenth, 2024 by Bob Ciura

Roper Applied sciences (ROP) has elevated its dividend payout for 30 consecutive years, and because of this it is among the Dividend Aristocrats.

The Dividend Aristocrats are a choose group of 68 shares within the S&P 500, with 25+ years of consecutive dividend will increase. We consider the Dividend Aristocrats are among the many greatest long-term investments that may be discovered within the inventory market.

You possibly can obtain a full listing of all Dividend Aristocrats (together with vital monetary metrics that matter) by clicking on the hyperlink beneath:

Disclaimer: Positive Dividend isn’t affiliated with S&P World in any means. S&P World owns and maintains The Dividend Aristocrats Index. The data on this article and downloadable spreadsheet is predicated on Positive Dividend’s personal evaluation, abstract, and evaluation of the S&P 500 Dividend Aristocrats ETF (NOBL) and different sources, and is supposed to assist particular person traders higher perceive this ETF and the index upon which it’s primarily based. Not one of the info on this article or spreadsheet is official knowledge from S&P World. Seek the advice of S&P World for official info.

As a way to grow to be a Dividend Aristocrat, an organization wants a powerful enterprise mannequin, sturdy aggressive benefits, and the power to face up to world recessions.

Clearly, the Dividend Aristocrats are high-quality dividend progress shares. Much more interesting is Roper’s excessive dividend progress fee. The latest improve was a ten% increase.

Even among the many Dividend Aristocrats, dividend hikes of 10% are uncommon, which makes Roper’s dividend will increase over the past decade very spectacular. This text will talk about Roper’s enterprise, progress potential, and valuation.

Enterprise Overview

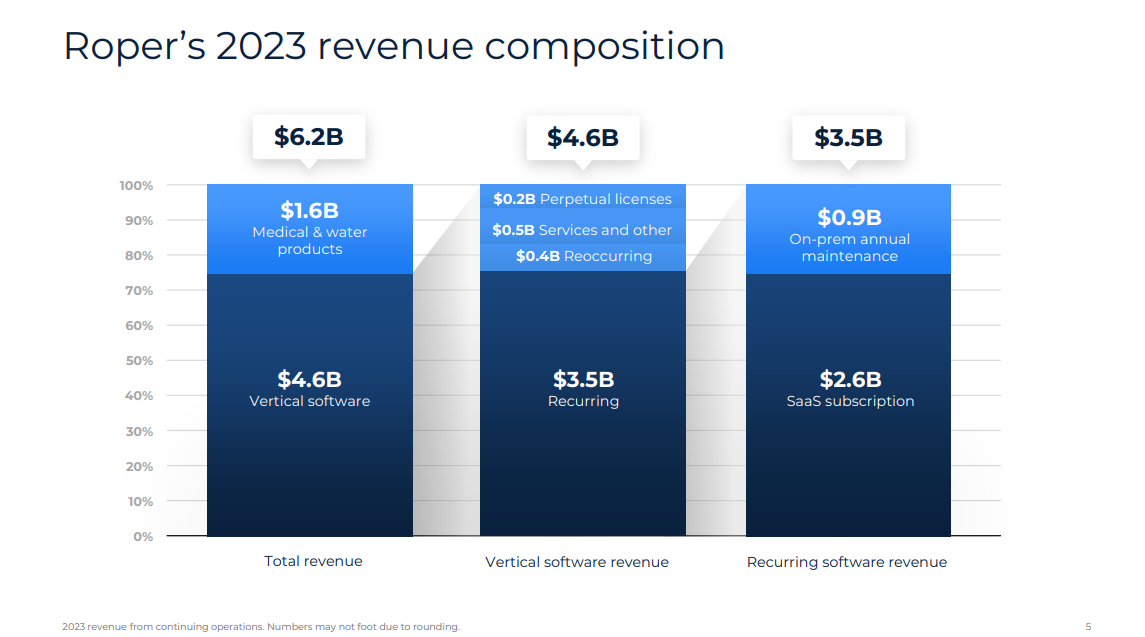

Roper designs and develops software program, together with each software-as-a-service and licensed expertise, and engineered merchandise and options. Roper has a various portfolio of services and products, which it supplies to a large number of sectors, together with healthcare, transportation, meals, power, water, and schooling.

Supply: Investor Presentation

Roper focuses on three foremost enterprise segments:

- Utility Software program

- Community Software program

- Expertise Enabled Merchandise

The Utility Software program enterprise consists of Aderant, CBORD, CliniSys, Knowledge Innocations, Deltek, Frontline, IntelliTrans, PowerPlan, Strata, and Vertafore as its foremost merchandise.

The Community Software program enterprise consists of ConstructConnect, DAT, Foundry, iPipeline, iTradeNetwork, Loadlink Applied sciences, MHA, SHP, and SoftWriters as its foremost merchandise.

Lastly, the Expertise Enabled Merchandise phase consists of CIVCO Medical Options, FMI, Inovonics, IPA, Neptune, Northern Digital, rf IDEAS, and Verathon as its foremost merchandise.

Roper has broadly benefited from the regular growth of the U.S. financial system over the previous decade. We consider the corporate can keep a optimistic progress trajectory for a few years going ahead.

Development Prospects

Roper is within the distinctive place of producing sturdy progress throughout its enterprise, even when the broader U.S. financial system faces challenges comparable to inflation and geopolitical danger.

On January thirty first, 2024, Roper reported its This autumn and full-year outcomes. On a seamless operations foundation, quarterly revenues and adjusted EPS had been $1.61 billion and $4.37, indicating a year-overyear improve of 13% and 11%, respectively.

The corporate’s momentum throughout the quarter remained sturdy, with natural progress coming in at 8%. Natural progress was as soon as once more pushed by broad-based power throughout its portfolio of niche-leading companies. For the 12 months, adjusted EPS landed at $16.71, up 17% in comparison with fiscal 2022.

Backed by Roper’s progress momentum, steadiness sheet power, and a big pipeline of high-quality acquisition alternatives, administration continues to consider Roper is properly positioned for continued double-digit money circulation progress.

Roper launched its adjusted EPS steering for FY2024, anticipating it to land between $17.85 and $18.15. We’ve got utilized the midpoint of the up to date vary in our estimate, which means a year-over-year improve of seven.7%.

Aggressive Benefits & Recession Efficiency

Over the previous a number of years, Roper pursued an asset-light enterprise mannequin, with a selected concentrate on software program and engineered services and products. The corporate adopted this technique to broaden margins, by lowering capital expenditure wants, whereas additionally producing recurring income.

This has resulted in a lot stronger money conversion over time and is prone to additional improve its money conversion ratio transferring ahead.

These elements present Roper with super aggressive benefits. Its excessive margins and operational effectivity present it with masses of cash circulation that may be invested to remain forward of the competitors.

One other aggressive benefit that Roper has is that it’s extremely diversified throughout the expertise sector. It owns ~27 unbiased companies with management positions in area of interest markets. Moreover, these finish markets are fairly diversified and supply sturdy recurring income and buyer retention.

Buyers also needs to word that previously, Roper was a cyclical enterprise. It had the capability for very sturdy progress when the financial system was increasing, but additionally struggled throughout recessions. Earnings-per-share throughout the Nice Recession are proven beneath:

- 2007 earnings-per-share of $2.68

- 2008 earnings-per-share of $3.06 (15% improve)

- 2009 earnings-per-share of $2.58 (16% decline)

- 2010 earnings-per-share of $3.34 (29% improve)

As you may see, Roper was not a extremely recession-resistant firm. Earnings-per-share declined 16% in 2009. If the financial system had been to enter a recession within the years forward, Roper may see earnings decline.

Nonetheless, Roper’s shift away from industrial companies in favor of software program companies has made it extra recession resistant because it now generates much more recurring income.

Supply: Investor Presentation

Roper additionally has an incredible dividend progress file, numbering 31 years of consecutive dividend will increase. Over the previous decade, DPS has grown yearly by a median of 13.8%.

We retain our DPS progress projection to 10%, which aligns with Roper’s newest improve and is well supported by the underlying web earnings. We anticipate Roper to develop earnings-per-share at a fee of 10% yearly by 2029.

Valuation & Anticipated Returns

Roper is a high-quality firm, with sturdy progress prospects, due to the excessive degree of demand for its expertise. Subsequently, it mustn’t come as a shock that the inventory holds a premium valuation, as shares at the moment commerce for a price-to-earnings ratio of 29.5. Its P/E a number of is barely above its common valuation over the previous 10 years.

Provided that rates of interest have risen considerably over the previous 12 months, we have now a goal price-to-earnings ratio of 26. If shares had been to revert to this goal valuation inside 5 years, annual returns can be diminished by 2.5% over this time. Potential overvaluation is a danger that traders ought to think about earlier than shopping for the inventory.

Nonetheless, this shall be offset by earnings-per-share progress (anticipated at 10% per 12 months) plus the 0.6% dividend yield, leading to whole anticipated returns of 8.1% per 12 months. This can be a passable projected fee of return for a powerful enterprise.

Last Ideas

Roper has a high-quality enterprise mannequin and 10% annual earnings-per-share progress isn’t an unreasonable assumption transferring ahead.

The inventory can also be a Dividend Aristocrat, and 10%+ annual dividend will increase are additionally attainable, due to the corporate’s excessive earnings progress fee.

Roper matches the invoice of an amazing firm, however the inventory seems to be overvalued. Whereas the inventory may nonetheless generate strong returns for shareholders, it isn’t at the moment a purchase because it doesn’t exceed our 10% annual return threshold. Roper inventory is a maintain.

Moreover, the next Positive Dividend databases comprise probably the most dependable dividend growers in our funding universe:

In case you’re searching for shares with distinctive dividend traits, think about the next Positive Dividend databases:

The key home inventory market indices are one other strong useful resource for locating funding concepts. Positive Dividend compiles the next inventory market databases and updates them month-to-month:

Thanks for studying this text. Please ship any suggestions, corrections, or inquiries to help@suredividend.com.

{kind=link}