Emanuel M Schwermer/DigitalVision by way of Getty Photos

Whereas it’s an exaggeration to argue that the wheels have come off Tesla, Inc. (NASDAQ:TSLA) the electrical automobile, or EV, pioneer, it is definitely true that the shine has come off:

Though the corporate has regained the crown of being the largest EV producer on the planet from BYD Firm Restricted (OTCPK:BYDDF) in Q1, which it had misplaced in This autumn/23, this appears like solely a reprieve to us as we argued in our article about BYD.

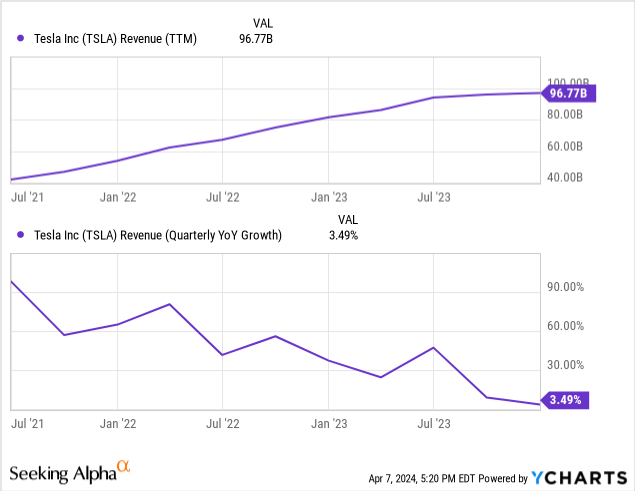

In any case, whether or not Tesla’s the largest producer or not, the steep decline in progress from 90% three years in the past to progress coming to a screeching halt after which going into reverse in Q1/24 (which is not within the graph above) with a whopping 20% income decline is not inspiring as the corporate faces numerous issues and threats:

- Market saturation by first adopters.

- Troublesome transition to mass-market merchandise.

- No new fashions.

- Worth competitors.

- The rise of Chinese language competitors.

- Geopolitical and commerce tensions.

- Gasoline economic system regulation.

- Lack of charging infrastructure.

U.S. Market saturation

There’s a marked slowdown within the adoption of EVs within the U.S. (our emphasis):

Almost 269,000 electrical autos have been offered in america within the first three months of this 12 months, in response to Kelley Blue E book. That was a 2.6 % improve from the identical interval final 12 months, however a 7.3 lower from the ultimate quarter of 2023. And amid the quarter-to-quarter slowdown within the trade, Tesla’s market share has fallen from 62 % at first of 2023 to 51 % now… Tesla gross sales fell greater than 13 % in contrast with the primary quarter final 12 months, whereas most of its rising opponents noticed double and even triple-digit progress.

Not solely is the market slowing down markedly, Tesla is shedding share, a double whammy. Different developed markets aren’t doing significantly better (March 2024 versus March 2023):

In Germany, gross sales plunged by 28.9pc in March, whereas they have been down by 41.4pc in Eire, 35.6pc in Finland, 34.4pc in Italy and 33.7pc in Sweden.

For the primary three months, EV gross sales have been nonetheless up in Europe, however solely 3.8% versus a progress of 43.3% within the first quarter of 2023.

The primary fashions of EV have been fairly expensive and brought up by a extra rich, much less price-sensitive clientele. China is by far the most important marketplace for EVs, the U.S. EV market is far smaller and even significantly smaller than the European market:

Electrek

Of all new EVs offered globally in December final 12 months, 69 % have been in China, in response to the analysis agency Rystad Power.

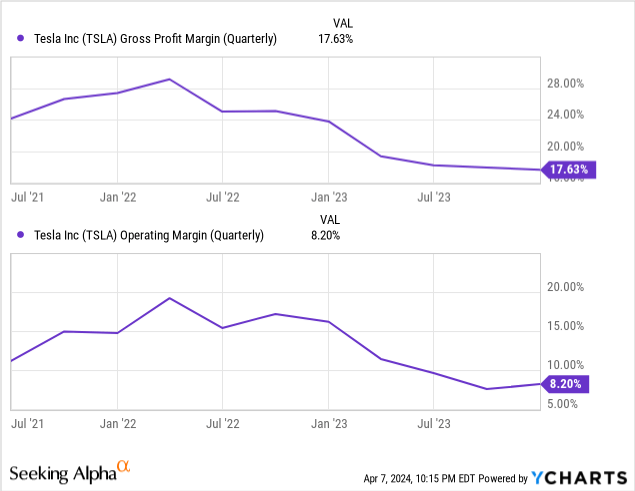

This has two fairly nasty penalties, declining progress and value competitors that led to a 25% value cuts for Tesla final 12 months. These not solely reinforce the income stoop, it additionally eats margins, which have been already on a downward slope:

This is not shocking, as extra EVs have entered the market and Tesla’s market share has declined from round 80% in 2019 to 56% final 12 months.

One would possibly wonder if Tesla is harm, particularly as most of its U.S. opponents can at the least fall again on their inner combustion engine (“ICE”) gross sales, that are worthwhile (opposite to their EV efforts).

Then again, Tesla is worthwhile with its EV manufacturing whereas we’re not conscious that any of its home opponents are, as Tesla loved an enormous first-mover benefit.

However the mixture of accelerating competitors and a marked slowdown in market progress is a fairly nasty one as effectively for Tesla, resulting in a progress slowdown (even unfavorable progress in Q1/24) and margin erosion.

Whereas the Chinese language EV market can also be slowing down (from 36% in 2023 to an estimated 25% this 12 months), it is nonetheless rising significantly sooner in comparison with the U.S. market, giving Chinese language producers some benefit, and China simply launched a 4-year 520 billion yuan ($72.3B) package deal of tax breaks.

To not point out the charging stations:

China is quickly increasing its EV charging infrastructure; as of August 2022, it accounted for 65% of worldwide public charging factors. In Might of 2022, China added 87,000 new charging stations, reaching a complete of 1.419 million stations… a January 2022 announcement revealed plans to ascertain 20 million EV charging services by 2025.

That is fairly a distinction with the U.S. (our emphasis):

Two years in the past, the U.S. authorities supplied $7.5bn to create a nationwide community of electrical automobile (EV) charging stations. So far, seven have been constructed.

That date was not way back, March 29, 2024! And what’s behind the slowdown?

the largest barrier to widespread adoption of EVs is price, which stays too excessive for many shoppers. The common electrical automotive sells for slightly below €70,000 (£59,900) within the US and about €65,000 in Europe, in response to analysis by Jato Dynamics. That compares to a typical price of simply over €30,000 in China

Transition to mass market

EV’s made up 7.6% of recent automotive gross sales within the U.S. in 2023, promoting 1.2M vehicles with Tesla taking 55% of that.

To revive market progress, EVs must develop into cheaper, however at current Tesla’s most cost-effective mannequin is the Mannequin 3, which begins at $38,990 as of April 2024.

Whereas that is so much higher than its older fashions, it is not fairly low-cost sufficient, particularly given the truth that Chinese language competitors can produce a number of fashions which are less expensive nonetheless.

As an illustration, BYD has a number of fashions that promote for much much less, like:

- The brand new Qin Plus DM-i variant is named the Glory Version, a plug-in hybrid retailing a simply over $11K.

- The Destroyer 05 is a hybrid that sells at $11K.

- The Seagull is an EV that prices $9.7K in China (the most costly model remains to be solely $12K).

- The brand new Dolphin Honor, which sells for lower than $14K.

- The ATTO 3 electrical SUV for $16.6K, which was the best-selling EV in Sweden in July 2023.

Some European firms are additionally planning to return out with cheaper fashions, like Renault with a brand new Twingo, though we’ll have to attend till 2026 for that to occur. Nevertheless it’s principally the Chinese language who’re invading the mass market section.

Chinese language aggressive benefit

As we argued way more extensively in our article on BYD, its aggressive benefit consists of a number of layers that allow it to supply these low-cost EVs (and hybrids), like producing its personal batteries, its built-in manufacturing, and benefiting from a a lot bigger and extra aggressive dwelling market with loads of authorities help.

That is all of the extra threatening as a result of Tesla is kind of depending on the Chinese language market, with about one-third of its international quantity being offered in China, the place it additionally has a plant.

Certainly, Tesla’s Q1 miss (in addition to BYD’s Q1 disappointment) would possibly very effectively have been principally the results of its gross sales in China., the place the market can also be slowing down and tormented by a value battle. What’s extra regarding is:

CEO Elon Musk seems to have backed away from the price-cuts technique this 12 months, nonetheless. Goldstein stated that is an indication he is aware of Tesla cannot win the value battle and stay worthwhile.

Too few fashions

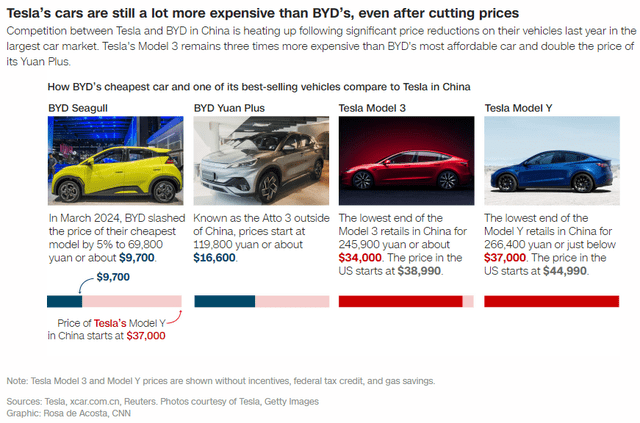

One other headwind is that Tesla has solely 4 fashions, and these are all fairly outdated. The 2 best-selling Tesla fashions, Mannequin 3 is 7 years outdated and Mannequin Y is 5 years outdated. Examine that to BYD:

CNN

Tesla will get undercut on the low finish by the Chinese language, the place Tesla would not have an providing. One may argue that this is not essentially an issue, because the low-end section tends to be a lot much less worthwhile. Nevertheless, it is the place many of the progress is.

So Tesla may do effectively to supply a product there and there have been plans to introduce a $25K Mannequin 2, however these plans appear to have been canceled, which prompted Tesla cofounder Martin Eberhard to precise issues:

We have each learn within the information, Tesla delaying or eliminating their low-end Mannequin 2 program, which is a disgrace for them, nevertheless it’s an indication that China has an opportunity to essentially unfold there

May or not it’s that, simply as they gave up on value cuts, Tesla realized it could not compete with the Chinese language within the low-end section?

However even within the increased segments, Tesla is dealing with elevated competitors, together with the Mannequin 3 from BYD’s Seal (additionally word how BYD launched 3 new EVs in a single 12 months and the way that compares with Tesla).

However Mannequin 3 is already dealing with competitors from the likes of BMW (the i4), Polestar 2, and Hyundai with its Ioniq 6. Then there may be the Xiaomi SU7, launched in March with a beginning value of $30K receiving a whopping 89K agency orders within the first 24 hours. This means a complete new dimension of competitors:

Much like the success of Huawei’s Aito M7, the disruption caused by Xiaomi EV goes past the product itself and stems from an efficient mixture of profitable advertising, branding, and to a higher extent, a longtime ecosystem, the staff stated. Thus, competing with tech veterans seems to be an uphill, however inevitable, battle for auto OEMs.

Even Tesla’s Cybertruck is getting competitors from BYD (and it is not the one one).

Whereas there’s something to say for Tesla to remain in its lane and never attempt to compete with the Chinese language head-on within the decrease segments, it’s dealing with growing competitors within the extra worthwhile increased segments as effectively, and many of the progress is within the decrease segments.

One other illustration of that’s Apple abandoning its deliberate EV, the place its Chinese language counterpart Xiaomi apparently succeeds.

So, whereas some have steered Musk might must abandon certainly one of his key 2024 methods – prioritizing market share over profitability – that technique is dealing with loads of obstacles as effectively.

Commerce Tensions

At current, at the least the U.S. market is comparatively shielded from Chinese language competitors on account of a 25% tariff on Chinese language EVs. However Tesla cannot survive on the U.S. market alone as Chinese language EVs are transferring aggressively into a number of third international locations, so Tesla is not shielded from Chinese language competitors.

And even the U.S. protect is not impermeable, BYD has plans for a plant in Mexico, which by advantage of the North American Commerce Deal would allow it to promote vehicles from that plant evading the tariff.

And the commerce tensions may very effectively escalate. EV manufacturing capability in China is effectively above what their home market can bear, and Treasury Secretary Janet Yellen has warned China that it could actually’t export its means out of overcapacity and decimate new industries like different vitality and EVs.

It would not appear possible she has met a receptive ear, and issues may very effectively escalate additional ought to Donald Trump, who threatened across-the-board tariffs on Chinese language items, develop into President once more in November (emphasis added):

By setting common baseline tariffs on a majority of international items, the previous president stated Individuals would see taxes lower as tariffs improve. His proposal additionally features a four-year plan to part out all Chinese language imports of important items, in addition to stopping China from shopping for up America and stopping the funding of US firms in China. Trump additionally stated in February that he would take into account imposing a tariff upward of 60% on all Chinese language imports if he is reelected.

That might open up Tesla to retaliatory actions and/or a Chinese language client boycott.

Elon Musk model

Some analysts argue that Musk has sullied his Tesla model, as one may argue that he rails in opposition to a perceived “liberal elite” who have been extra possible to purchase Teslas.

It is tough to measure this, however there’s something regarding. Tesla gross sales have slumped greater than different EV manufacturers within the U.S. (our emphasis):

However, upon nearer inspection, what looks as if widespread disinterest in electrical autos might mirror, largely, much less curiosity in Tesla. Some automakers, together with Audi, BMW, Mercedes, and Rivian, are reporting EV gross sales progress of greater than 50% over the previous 12 months, famous Stephanie Valdez Streaty, an analyst with Cox Automotive, in a presentation summarizing trade tendencies within the new 12 months. Ford later stated its EV gross sales have been up 86%… Between the primary quarter of 2023 and the primary quarter of 2024, US electrical automobile gross sales grew an estimated 15%, in response to a latest report by Cox Automotive. However, if you happen to miss Tesla, gross sales of different electrical autos, as a gaggle, have been up 33%.

So it does like Tesla was disproportionately hit. Whether or not this has something to do with Musk’s antics scaring sure consumers off isn’t one thing we will set up right here, nevertheless it’s not more likely to have helped.

Tradition wars

Aside from the likelihood that Musk is estranging a few of his more than likely consumers by plunging into the deep finish of the tradition wars, EVs themselves have develop into a ping pong ball within the tradition wars.

The tone concerning the slowdown of EV gross sales within the reporting of a number of the conservative press borders on the jubilant.

What’s curious is that Musk has related himself with Trump, which from a Tesla enterprise perspective is odd as a Trump authorities is liable to throw fairly a little bit of sand within the wheels of the vitality transition, ought to he get elected in November.

Trump is more likely to morph these cultural headwinds into precise coverage, as an example by reversing a lot of Biden’s IRA:

Goldman Sachs analysts have additionally argued that any discount within the variety of autos eligible for buy credit tied to the Inflation Discount Act may have an effect on between 5% and 15% of whole EV demand, whereas an outright repeal “may have an effect on 10% to 30% of demand.”

Then there may be this:

Trump has promised to roll again new automotive air pollution guidelines on the Environmental Safety Company that would require electrical autos to account for as much as two-thirds of recent vehicles offered within the US by 2032.

This might actually decelerate the adoption of EVs within the U.S., and will even bifurcate the world’s automotive market into an ICE block and an EV block, at the least till the arrival of next-generation batteries swings the financial benefit undoubtedly in direction of EVs.

How Tesla would fare in such an atmosphere is anyone’s guess, we definitely do not underestimate its capability for reinventing itself, however the atmosphere during which it operates may develop into considerably extra problematic than it already is at present.

U.S. safety

Although Tesla is shedding market share in its dwelling market as Detroit is in on the sport, it has some safety in opposition to the Chinese language within the type of a 25% import goal.

Whereas Elon Musk has been “begging” for prime commerce safety, it runs afoul of US local weather coverage, it is futile to a substantial extent because the Chinese language can construct vegetation in Mexico which in fact has recourse to the North American free commerce settlement with the U.S.

And Chinese language vegetation in Mexico would run afoul of one other purpose of the Biden administration (and presumably additionally of any incoming Trump administration) to construct up home manufacturing capability in industries of the longer term.

There are different tips potential, like conserving Chinese language vehicles out by contemplating their web connection a nationwide safety threat, it dangers making EVs dearer within the U.S. in comparison with elsewhere.

Because the expertise with the emergence of Japanese automotive producers from the Nineteen Seventies onward has proven, in the end it is higher to adapt to the competitors (which Detroit did by largely copying the Toyota manufacturing strategies).

Funds

As now we have seen above, progress has come to a screeching halt and elevated competitors and value wars have diminished margins.

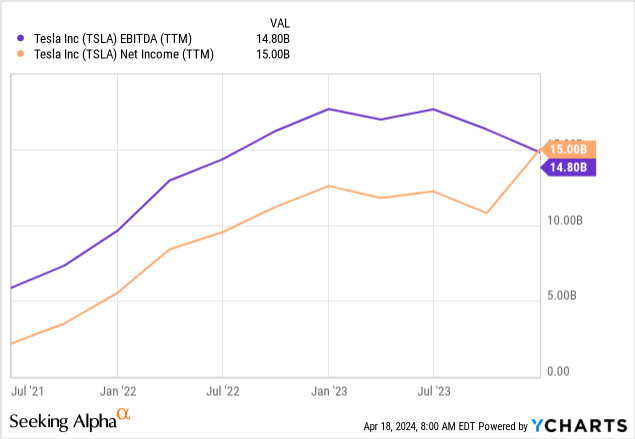

The state of affairs is severe sufficient for Musk to appreciate that he can not win a value battle with the Chinese language, so he has given up on market share and concentrates on profitability as a substitute, the place progress can also be topping out, though This autumn/23 produced a pointy revival at the least in web revenue:

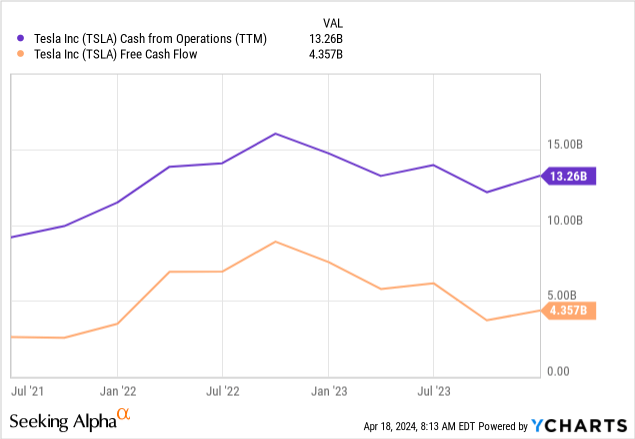

We at all times discover that money circulate normally delivers a greater image because it’s much less fungible:

However issues are sufficiently dire for Tesla to embark on a major cost-cutting program, shedding 10% of the workforce (even when on the identical time it is asking shareholders to simply accept Musk’s $56B pay package deal).

Valuation

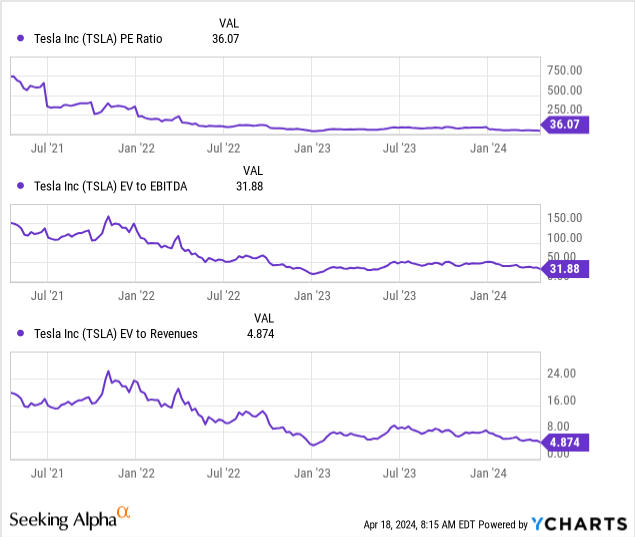

Valuation metrics have come down from what can solely be thought-about excessive heights, however these are nonetheless fairly lofty given the expansion slowdown and margin contraction.

Conclusion

The corporate is dealing with a barrage of obstacles, few of which it has a lot, if any, management over:

- No latest new fashions.

- No low-segment mannequin, the place many of the progress is.

- Disappointing progress and shedding market share.

- Rising competitors, particularly from the Chinese language.

- A value battle.

- Model issues.

- Commerce tensions with China.

Principally, the place they compete is an more and more crowded place the place progress is disappearing in massive elements and opponents gaining on Tesla’s market share.

With the delay and even cancellation of the Mannequin 2, there might be no transfer in direction of the section of the market that’s nonetheless rising, and even with such a transfer, success is way from assured given the power of the competitors, notably the Chinese language.

Administration argues that they’re “between” two progress waves, which could very effectively be true, however the subsequent progress wave will come when infrastructure has been rolled out extra totally and particularly when a brand new technology of batteries extends the attain, improves security, and reduces charging occasions.

Tesla was the principle driver of the primary wave, there are not any ensures it will likely be a predominant driver of the second wave, nevertheless it’s nonetheless valued as if it will likely be, therefore our promote score on the inventory. That second wave can also be more likely to be a number of years out.

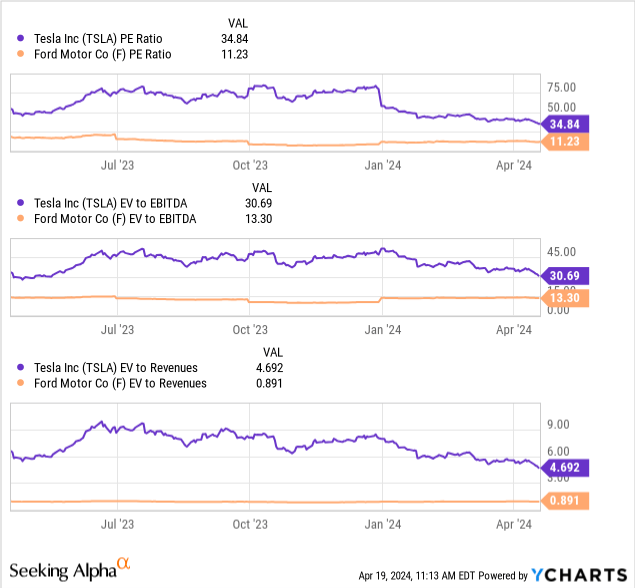

We do not see a lot purpose for Tesla to hold onto a lot of its premium valuation, and a easy comparability with Ford reveals that the draw back might be appreciable:

We do not suppose it is inconceivable for Tesla, Inc. to fall beneath $100, and we’re not inclined to purchase till it does, except one thing essentially improves. We await the Q1 earnings launch post-market on Tuesday, April twenty third.

Tesla nonetheless has some issues going for it, however that would be the topic for an additional article. For now, it is too little for us.

Editor’s Notice: This text discusses a number of securities that don’t commerce on a significant U.S. alternate. Please pay attention to the dangers related to these shares.

{kind=link}