stockcam

The current IPO of Reddit, Inc. (NYSE:RDDT) began too sizzling, and the inventory is not a lot of a discount after the current dip. The social media firm has not generated something spectacular over a protracted historical past of operations to warrant such investor pleasure. My funding thesis is Bearish on the inventory with the elevated valuation.

Scorching IPO

Reddit’s sizzling IPO was priced again on March 20. The IPO offered 22 million shares to the general public at $34 per share, with the corporate promoting 15.3 million shares and promoting stockholders dumping 6.7 million shares.

Together with the three.3 million over-allotment shares for the underwriters, Reddit will promote ~18.5 million shares and lift gross proceeds of $629 million earlier than underwriter charges.

Following the providing, the inventory soared to just about $75. Reddit has dipped again under $50 now, however the inventory remains to be $14 above the IPO value, simply over a month following the IPO.

Reddit sees the corporate as a digital metropolis, with inside communities permitting customers to attach on nearly each subject attainable. Based on the S-1, the social website customers skew older, with the everyday person not on Snapchat or Twitch and correlating with customers on Meta Platforms’ (META) Fb.

Reddit S-1

Large Quarterly Report

Reddit is about to report Q1 ’24 quarterly outcomes post-market on Might 7. For any IPO, the primary quarterly report is a giant occasion, as traders get to see up to date quarterly numbers and begin to study the steering tendencies from executives.

The latter is a giant key as a result of totally different executives supply totally different views, with some at all times over-promising and never delivering and others under-promising and consistently mountain climbing numbers all year long. It is essential for traders to know these tendencies to achieve views on the inventory motion after quarterly stories, and traders actually do not know till after the IPO stories the primary quarterly quantity.

Reddit ended 2023 with a surge in DAUs (day by day common uniques). The corporate reported a bounce from 60.4 million in Q2 ’23 to 73.1 million in This autumn ’23.

Reddit S-1

Nearly all of the expansion got here from Logged-out customers, with development from 28.3 million in Q2 ’24 (down from Q1 ’21 ranges) to 36.7 million in This autumn ’23. Naturally, the Logged-out customers have restricted worth, having come to Reddit based mostly on search outcomes or clicking on hyperlinks. These informal customers have chosen to not create an account to work together on the positioning, and the Google information is very inaccurate.

Additionally, Reddit has a portion of customers targeted on materials the place the corporate does not current adverts. CEO Steve Huffman mentioned this state of affairs with CNBC proper earlier than the IPO debut of not monetizing NSFW communities.

One other huge key to Reddit is that the corporate was created in 2005 and began promoting ads all the best way again in 2006. The corporate even began constructing their very own advert expertise in 2018.

In essence, Reddit is not a brand new or younger firm with a large upside forward. Social media chief Meta Platforms simply reported quarterly gross sales topping 27%, with steering in the direction of practically 20% development within the present quarter, so robust development is certainly nonetheless attainable.

The explanation the inventory is just too cherished is that Reddit nonetheless generates adjusted EBITDA losses and burns money regardless of happening practically 20 years of promoting ads. The corporate simply is not prepared for prime time, but the inventory market has already assigned a premium valuation.

For 2023, Reddit nonetheless produced an adjusted EBITDA lack of $69 million on income of $804 million. Revenues did develop over 20% and the EBITDA loss improved by $39 million YoY, however the social media firm nonetheless has a big loss in any case of those years.

Reddit S-1

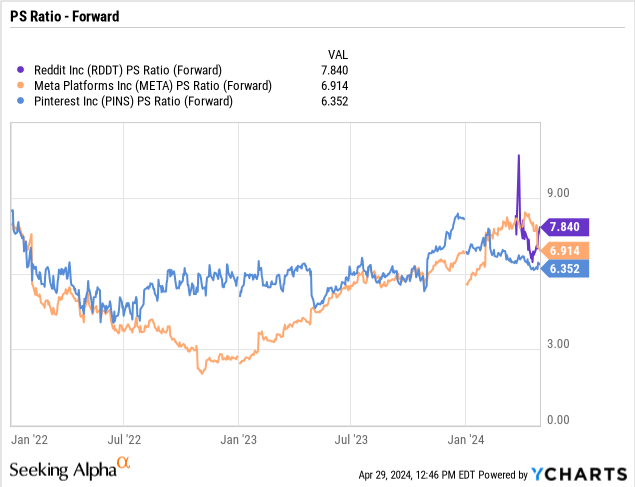

The inventory ought to have 162 million shares excellent plus one other 40 million totally diluted shares for inventory choices and RSUs after the IPO. The inventory has a market cap of $7.7 billion, with a completely diluted valuation of nearer to $9.7 billion. Reddit trades at ~7.5x the present 2024 income estimates of $985 million.

The inventory trades at an analogous a number of to Meta Platforms and Pinterest (PINS), although each shares have extra confirmed enterprise fashions and catalysts. The consensus analyst estimates do not even forecast a revenue for Reddit till 2027 whereas the opposite social media performs will throw off tons of money throughout this era. To not point out, Reddit trades near 10x gross sales when contemplating the totally diluted share counts.

Reddit is way too costly for a inventory nonetheless burning $85 million in free money move and competing with the likes of Fb for promoting {dollars}.

Takeaway

The important thing investor takeaway is that Reddit remains to be far too costly right here, buying and selling far above the IPO value. The social media firm has improved development charges not too long ago, however Reddit nonetheless has a 19-year historical past with out producing earnings.

Buyers within the IPO ought to use the present value to exit the inventory on power.

{kind=link}