Susumu Yoshioka/DigitalVision through Getty Photos

April twenty ninth ended up being a somewhat fascinating day for shareholders of steel packaging agency Crown Holdings (NYSE:CCK). After the market closed, shares jumped about 3.3% in response to administration asserting monetary outcomes protecting the primary quarter of the corporate’s 2024 fiscal 12 months. Though the agency failed to satisfy expectations when it got here to income and earnings per share, adjusted earnings per share exceeded forecasts and administration reaffirmed stable backside line development for this 12 months relative to final 12 months.

To be trustworthy, blended outcomes shouldn’t be stunning for this area. The packaging trade has at all times been subjected to some extent of volatility. In recent times, the monetary image had been fairly spectacular. This has been very true on the underside line for Crown Holdings and different firms prefer it. This volatility is probably going what has been chargeable for the corporate’s underperformance relative to the broader market. You see, again in October of 2022, I wrote a bullish article concerning the agency, with my optimism primarily based on sturdy elementary efficiency and the truth that shares had been attractively priced. I anticipated some good development from the corporate. Nonetheless, shares have seen draw back of two.9% since then. That is far worse than the 35.2% enhance seen by the broader market over the identical window of time.

Quick ahead to at present, and the image continues to be somewhat complicated. However I would not precisely name it dangerous. Volatility is sort of sure to stay the story for this identify. However whether or not or not it is smart to purchase into is a special query completely. On an absolute foundation and relative to comparable companies, Crown Holdings does appear to be buying and selling at a slight low cost. This offers me some extent of optimism transferring ahead. Alternatively, for many who cannot cope with unstable income and income, it is likely to be greatest to look elsewhere for upside.

An fascinating quarter

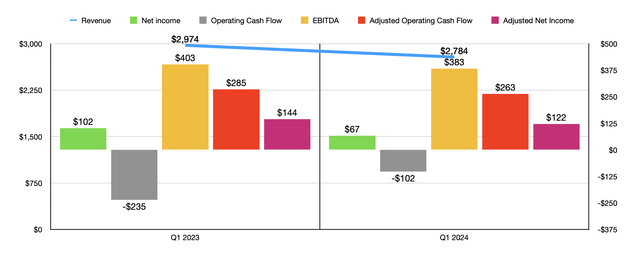

As I discussed already, after the market closed on April twenty ninth, the administration crew at Crown Holdings introduced monetary outcomes protecting the primary quarter of the 2024 fiscal 12 months. On the highest line, the image was problematic. Income of $2.78 billion got here in 6.4% decrease than the $2.97 billion generated one 12 months earlier. In truth, gross sales ended up being $150 million decrease than what analysts had been hoping for. However it would not do justice to look solely at income. And that is largely as a result of an enormous portion of the corporate’s enterprise mannequin includes passing on uncooked materials prices, which not solely will increase, but in addition decreases, to its clients.

Creator – SEC EDGAR Information

For example, in keeping with administration, the corporate noticed elevated beverage can shipments all through the Americas and European Beverage operations. The agency additionally benefited to the tune of $10 million from overseas foreign money fluctuations. All through North America, the corporate benefited from a 7% enhance in beverage shipments. In Europe, development was solely about 5%. Mixed, this helped to push international beverage shipments up 2.5% 12 months over 12 months. Nonetheless, there have been lowered volumes shipped in most different traces within the enterprise. However along with that, the corporate additionally handed on $130 million to its clients within the type of decrease materials prices. In idea, to the extent that costs are decreased due to a discount in the price of uncooked supplies, the underside line for the corporate shouldn’t be negatively impacted.

On the underside line, the image is equally sophisticated. Earnings per share really fell 12 months over 12 months, dropping from $0.85 to $0.56. This additionally meant that earnings fell wanting expectations by $0.18 per share. However on an adjusted foundation, the decline was extra modest, from $1.20 to $1.02. In truth, adjusted earnings got here in six cents per share increased than what administration thought they might. This translated to adjusted earnings of $122 million, with GAAP earnings coming in barely greater than half that at $67 million. One 12 months earlier, these figures had been $144 million and $102 million, respectively. Different profitability metrics posted declines as nicely, however to not the identical extent. Working money move really improved from detrimental $235 million to detrimental $102 million. However on an adjusted foundation, it dipped solely barely from $285 million to $263 million. In the meantime, EBITDA for the corporate fell from $403 million to $383 million.

Creator – SEC EDGAR Information

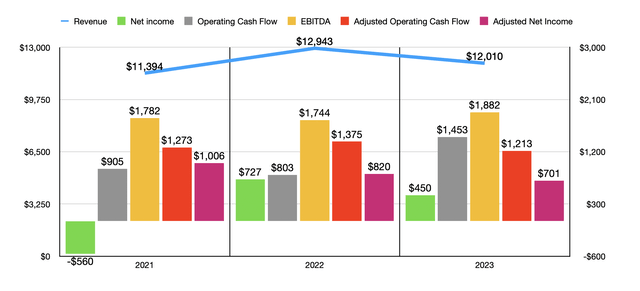

Though it is disappointing to see this sort of efficiency 12 months over 12 months, it’s price noting that current years have proven comparable levels of volatility. As you’ll be able to see within the chart above, income did drop in 2023 relative to 2022. Web income additionally fell. Nonetheless, money flows grew properly, not less than on the subject of official working money move and EBITDA. Most significantly, this monitor document exhibits you simply how unstable the corporate is from a outcomes perspective.

Regardless of these issues, administration is concentrated on bettering for the lengthy haul. As an example, the agency was in a position to announce that it simply accomplished its beverage can growth program that it began in 2019. That features plant startups in Mesquite, Nevada, and in Peterborough, UK. These investments, in addition to others, induced the corporate to incur vital bills in recent times. In 2023, for example, the corporate allotted $793 million towards capital expenditures. And prior to now three years mixed, capital expenditures totaled $2.45 billion. However with its present growth plans accomplished and no different main initiatives within the works, the agency is anticipating capital expenditures this 12 months of about $500 million. It expects an identical quantity, if not much less, in 2025. This could finally assist free money move to return in sturdy and for the corporate to make use of this to pay down the $6.33 billion in web debt that it has and/or to reward shareholders straight.

I might additionally wish to level out that, despite the fact that outcomes up to now for 2024 should not wanting nice, administration believes that adjusted earnings per share can be between $5.80 and $6.20. On the midpoint, this could translate to adjusted web income of $725 million. That is up from the $701 million in adjusted income generated in 2023. If we assume that different profitability metrics rise on the identical price, then adjusted working money move needs to be round $1.26 billion, whereas EBITDA ought to are available someplace round $1.95 billion.

Creator – SEC EDGAR Information

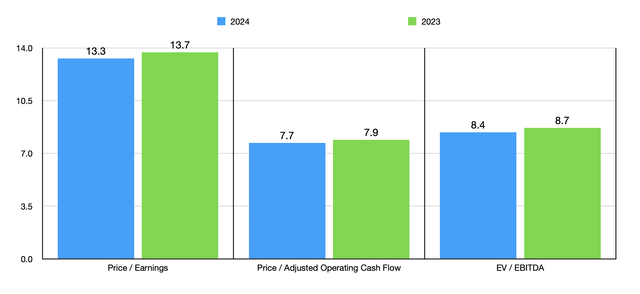

With these outcomes, I used to be in a position to worth the corporate as proven within the chart above. I additionally included a valuation that was primarily based on 2023 figures. On a worth to earnings foundation, shares do look a lot nearer to being pretty valued. However on the subject of the opposite profitability metrics, the inventory seems to be fairly reasonably priced. It is also price noting that shares are buying and selling nearer to the low finish of the spectrum relative to comparable enterprises. Within the desk under, I in contrast it with 5 comparable companies. And in every of the three circumstances, solely two of the 5 firms ended up being cheaper than it.

| Firm | Value / Earnings | Value / Working Money Circulate | EV / EBITDA |

| Crown Holdings | 13.7 | 7.9 | 8.7 |

| AptarGroup (ATR) | 34.4 | 17.0 | 15.7 |

| Berry World Group (BERY) | 12.4 | 4.3 | 8.2 |

| Silgan Holdings (SLGN) | 15.9 | 10.7 | 9.1 |

| Ball Company (BALL) | 31.6 | 12.0 | 15.3 |

| Greif (GEF) | 10.7 | 5.8 | 8.0 |

Takeaway

To be completely trustworthy with you, I got here into this text with a blended view of the agency. Normally, I’m a fan and shares are attractively priced. However the volatility may be unnerving. It is also not nice to see income and official earnings fall wanting what analysts anticipated. However the deeper you dig, the extra interesting the enterprise turns into. Whereas shares won’t be a house run by any means, administration is forecasting backside line enchancment that needs to be increased, on an adjusted foundation, than it was in 2023. The corporate is completed spending great quantities of capital on growth initiatives and that ought to assist to move to the underside line and, ideally, can be utilized to cut back debt. And relative to comparable enterprises, shares look to be barely towards the low finish of the spectrum. In all, the nice right here outweighs the dangerous simply sufficient for me to reiterate the ‘purchase’ ranking I assigned the corporate again in October of 2022. However I do perceive why those that don’t love volatility may select to look elsewhere for upside.

{kind=link}