JHVEPhoto

Roku, Inc. (NASDAQ:ROKU) has continued to disappoint its traders because the headwinds of elevated gross sales and advertising spending for Roku’s system section probably led to a reversal on ROKU inventory’s preliminary post-earning surge. Accordingly, Roku posted its first-quarter earnings launch final week, surpassing Wall Avenue estimates. Roku headed into its Q1 earnings with relative pessimism, as ROKU patrons did not defend the $60 stage in early April. Because of this, ROKU additionally felt the influence of the broad market pullback in April, as traders reassessed the ROKU’s progress premium. I upgraded ROKU to Purchase in mid-February 2024. Nevertheless, that thesis has not panned out, because the market appropriately anticipated extra intense profitability progress inflection challenges for Roku in 2024.

Whereas Roku patrons had demonstrated an intent to defend the $55 stage as Roku posted its first-quarter scorecard, shopping for momentum rapidly dissipated. Traders assessed the potential influence of elevated spending “resulting in a slight moderation in adjusted EBITDA relative to the primary half of the 12 months.”

Accordingly, Roku delivered Q1 income progress of 19% YoY, beating Wall Avenue projections. The expansion momentum was broad-based, pushed by a 19% income uptick in Roku’s Gadget and Platform segments, respectively. Nevertheless, Roku’s Gadget section suffered a adverse gross margin of virtually -5%, though it improved from This fall’s -13% metric. As well as, Roku emphasised its confidence in a “optimistic development” in Gadget margins progress trajectory “with anticipation of price construction enchancment over time.”

Subsequently, given the mounting challenges within the media and leisure scene, it ought to have been construed as a fairly stable report. Google’s (GOOGL) current Q1 earnings confirmed that YouTube has additionally outperformed analysts’ estimates, suggesting a buoyant market. Subsequently, it appeared like ROKU was well-positioned to rebound from its collapse from its February 2024 highs. Nevertheless, the market’s issues about elevated spending affecting Roku’s anticipated profitability inflection aren’t welcomed and are justified.

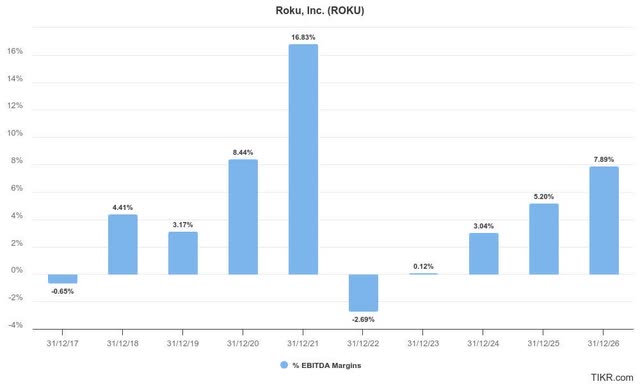

Roku adjusted EBITDA margins development and estimates (TIKR)

As seen above, Roku has did not display how Roku’s market management within the ad-supported video house has led to a sustainable profitability drive. The post-pandemic surge proved to be a bubble, as Roku’s adjusted EBITDA margins fell into adverse territory in FY2022.

Because of this, I imagine the market is further cautious about elevated spending, suggesting Roku may face a tougher-than-expected advert market than anticipated. YouTube TV’s skill to drive positive factors within the subscription house should not have hampered the Roku platform’s ad-supported progress momentum. That was demonstrated in Q1 as Roku surpassed Wall Avenue’s estimates.

Nevertheless, YouTube TV is gaining valuable actual property in viewers’ houses. Gaining extra eyeballs and engagement hours may bolster YouTube’s “enchantment to advertisers throughout upfront TV advert negotiations.” As well as, it may additionally strengthen YouTube’s “skill to offer insights into viewers’ preferences throughout varied content material.” Because of this, I imagine the shortcoming of Roku to translate its market management into predictable and sustainable profitability progress inflection will proceed to weigh on investor sentiments. Given the teachings discovered in 2021/22, I imagine the market is pricing in a lot greater execution dangers to mirror elevated spending issues and their doable influence on Roku’s margins.

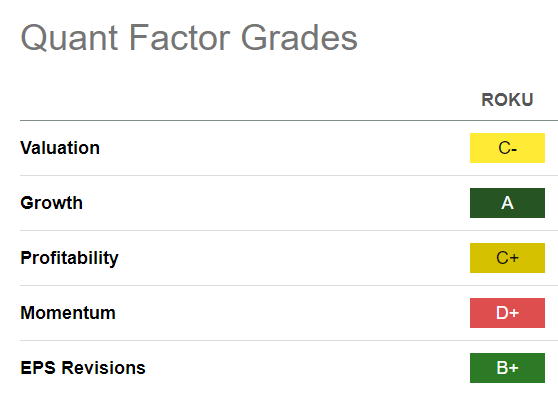

ROKU Quant Grades (Searching for Alpha)

With Roku not paying dividends, ROKU traders should depend on progress traders to drive shopping for momentum. Nevertheless, ROKU’s uninspiring “D+” momentum grade suggests progress traders have probably rotated towards extra enticing performs within the AI house, as prospects for near-term monetization in AI appear sooner than anticipated.

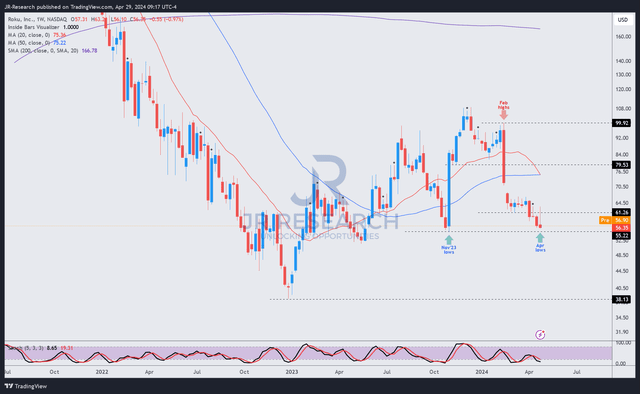

Nevertheless, may ROKU be near peak pessimism, because it plunged deep right into a bear market, down almost 50% from its December highs at ROKU’s lows final week?

ROKU value chart (weekly, medium-term) (TradingView)

Sadly, ROKU’s upward bias was invalidated when ROKU patrons did not underpin a constructive consolidation zone above the $60 stage. As soon as that stage was taken out decisively by intense promoting in April, I am not stunned that ROKU’s $55 stage may very well be inside attain, as additional promoting strain may power a re-test of ROKU’s November 2023 lows.

Because of this, ROKU has almost made a spherical journey since bottoming out in late 2023. Whereas extra sturdy bullish sentiments may encourage me to retain my Purchase thesis, I’ve but to evaluate such optimism.

Subsequently, I imagine the stakes have modified for Roku as traders grapple with the doable influence on Roku’s profitability within the second half. Whereas Roku remains to be anticipated to scale and achieve working leverage by way of 2025, ROKU is not priced at a reduction. Subsequently, traders will probably demand nothing lower than sturdy execution with out unanticipated adverse surprises throughout this era as investor sentiments stay unsure.

Consequently, I assessed the danger/reward on ROKU as much less enticing, behooving me to return to the sidelines.

Ranking: Downgrade to Maintain.

Essential notice: Traders are reminded to do their due diligence and never depend on the knowledge offered as monetary recommendation. Take into account this text as supplementing your required analysis. Please all the time apply unbiased considering. Notice that the ranking shouldn’t be supposed to time a particular entry/exit on the level of writing until in any other case specified.

I Need To Hear From You

Have constructive commentary to enhance our thesis? Noticed a important hole in our view? Noticed one thing essential that we didn’t? Agree or disagree? Remark beneath with the purpose of serving to everybody locally to study higher!

{kind=link}