Scott Olson

Extra Than Simply A Enjoyable Get Collectively

I’ve typically referred to the Berkshire Hathaway (NYSE:BRK.A) (NYSE:BRK.B) annual conferences as a enjoyable time for shareholders to get collectively and store however not essentially obtain new details about the corporate within the marathon Q&A session. The 2024 assembly was completely different in that regard. With the passing of vice chair and Warren Buffett’s greatest good friend Charlie Munger, the stage was occupied by Warren and Greg Abel, the long run CEO and non-insurance vice chair. Insurance coverage vice chair Ajit Jain was additionally current for the morning session. With Warren himself recognizing the constraints to his tenure and capabilities and Greg on deck to take over, we acquired extra readability than ever earlier than about how issues at Berkshire will change sooner or later.

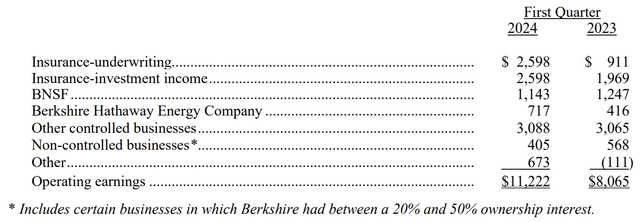

Previous to the assembly, Berkshire launched Q1 2024 outcomes. On an general firm foundation, they have been wonderful, with working revenue of $11.2 billion, up 39% from Q1 2023. At $5.20 per B share equal, the outcomes beat analyst estimates for the quarter by $0.29, though neither Warren nor most Berkshire shareholders give attention to that metric.

Berkshire Hathaway

The drivers of this end result needs to be acquainted to those that comply with Berkshire carefully or learn my quarterly articles on the corporate. Insurance coverage had robust underwriting efficiency, helped by premium raises and lack of main catastrophic losses within the quarter. BNSF railway continues to lag its friends. Berkshire Hathaway Power had an OK quarter, which beat final 12 months primarily as a result of no new prices have been taken for the PacifiCorp wildfires, though the issue is certainly not but behind them. Different companies have been in line, with manufacturing surprisingly robust and Service and Retail beginning to present indicators of client weak spot.

Whereas I normally wish to give attention to the working firms in my evaluation, lots of the outcomes we noticed in Q1 are much like current quarters. Fairly than rehash them, I’ll begin with a overview of Berkshire’s funding portfolio and capital allocation, the place there have been a number of new headlines popping out of the Q1 earnings and annual assembly. I’ll then contact on the companies briefly, specializing in discussions from the assembly. Lastly, I’ll replace my valuation mannequin. Final quarter, I rated Berkshire a Maintain, resulting from valuation. This was name, with the inventory down just a little greater than 2% since then. E book worth has come up almost 2%, whereas my estimate of intrinsic worth is nearly unchanged. The marginally wider low cost to honest worth, together with optimistic modifications seemingly beneath Greg Abel’s future management deserve an improve to Purchase.

Funding Portfolio

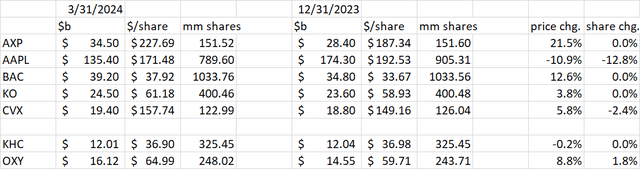

Berkshire’s greatest transfer up to now quarter was revealed earlier than the assembly, the place we noticed from the 10-Q that the corporate offered about 116 million shares of Apple (AAPL), or 12.8% of its place. This accounted for almost the entire $20 billion of inventory gross sales within the quarter. Amongst Berkshire’s prime 5 holdings, the one different gross sales have been a continued trimming of Chevron (CVX) on the similar time including to Occidental (OXY), though Chevron stays the bigger holding of the 2 vitality firms.

Creator Spreadsheet

Discussing the Apple sale throughout the assembly, Warren let his views on common market valuation and macro situations come out a bit, an more and more uncommon prevalence. He said that he “didn’t thoughts in any respect” elevating money within the present market surroundings. He additionally did not thoughts paying 21% company tax on the capital achieve as a result of he anticipated the tax charge to be greater sooner or later. In direction of the top of the assembly, Warren talked about his fear in regards to the US authorities fiscal deficit, suggesting it’s not sustainable in the long run.

A smaller sale in Q1, however not beforehand reported, was the exit from Paramount (PARA) at a loss. Warren took “100%” accountability for this commerce. It was not executed by Berkshire’s funding managers Todd Combs and Ted Weschler. Warren was an enormous admirer of Tom Murphy of ABC Capital Cities, which for my part gave him some false confidence that he understood the media enterprise. As we speak’s surroundings with twine chopping and fickle streaming clients who churn from platform to platform is far more tough than Tom Murphy’s world of 30 years in the past.

The shareholder assembly had a big share of questioners from exterior the US, a number of of whom requested Warren about Berkshire’s curiosity investing of their residence nation. Warren’s responses recommend that he lacks the curiosity and vitality to pursue international alternatives. The Japanese buying and selling firms have been an exception, for my part as a result of they have been a basic worth funding – low-cost, with excessive free money circulation and return on fairness. Warren was diplomatic to a Chinese language investor, though it’s clear from his previous actions like promoting Taiwan Semiconductor (TSM) and trimming BYD (BYD) that Charlie was the larger China bull of the 2. Relating to India, Warren acknowledged “there should be a number of alternatives” however didn’t really feel he had an edge to pursue them. He said “extra energetic administration” would possibly pursue these alternatives sooner or later. Contemplating Warren’s feedback about Greg Abel’s vitality degree in comparison with his, it is a good signal that Berkshire would possibly widen its funding universe beneath the subsequent administration. With a lot international curiosity in Berkshire, as evidenced by the variety of non-US questioners on the assembly, it’s clear that the corporate enjoys a lot goodwill exterior the US and might be a much bigger participant in the event that they need to.

That brings us to a different piece of recent info from the assembly, that Warren’s view on accountability for Berkshire’s future funding administration has advanced. He now believes the CEO (Greg) needs to be answerable for capital allocation. The Ted and Todd experiment appears to be ending. After praising them within the early days of their time at Berkshire, we now hear nothing from Warren about them, aside from Ted’s administration of Geico, the place he seems to be making some progress.

It in the end stays a query for Greg and the board to resolve how Berkshire will handle its funding portfolio sooner or later, however we may even see additional simplification of the portfolio with continued trimming of small positions and a wider territory for “elephant hunts”.

Capital Administration

The money raised within the Apple and Paramount gross sales virtually matches the expansion in Berkshire’s money and T-Invoice place, up $19 billion sequentially to $182.3 billion. The money now exceeds the insurance coverage float legal responsibility, which declined $1 billion sequentially to $168 billion. Warren said that Berkshire “solely swings at pitches we like” and expects the money hoard to develop above $200 billion this 12 months. This isn’t a horrible selection at T-Invoice charges of 5.5%, however Warren famous he would nonetheless keep the money hoard if rates of interest declined. Sooner or later it turns into worth damaging to carry that a lot money, particularly in an inflationary surroundings. The prospect of Berkshire widening its funding alternative set beneath future administration is a optimistic. Additionally, throughout the lunch break, board member Ron Olson famous on CNBC that the board is “not ruling out” a dividend after Warren’s tenure. Whereas the tax inefficiency of a dividend detracts from shareholder worth, so does holding money incomes an rate of interest lower than inflation whereas the corporate pays tax on the curiosity anyway.

Berkshire generated $6.17 billion of free money circulation in Q1, an enchancment from $4.98 billion in Q1 2023. Working money elevated $1.87 billion, whereas capex additionally elevated $0.68 billion. Berkshire additionally raised money by promoting or redeeming at maturity $6.6 billion from its bond portfolio. The corporate used this money by shopping for again $2.6 billion value of Berkshire inventory, $2.7 billion in new inventory purchases, $2.6 billion on the ultimate tranche of Pilot, and paying off about $4.6 billion of debt.

The share buybacks in Q1 have been at a barely decrease tempo than FY 2023. If annualized, they characterize 1.2% of Berkshire’s market cap. To this point in Q2, buybacks have been minimal, at simply 454 A share equivalents, or 0.03% of market cap. It’s notable that from December by March, the buybacks have been within the type of A shares solely. As mentioned throughout the assembly, simply earlier than and after the lunch break, Berkshire is shopping for blocks of A shares from long-time shareholders who’re then making massive donations for philanthropic functions.

Working Companies

As I discussed at the beginning, lots of the working developments in Q1 have been much like the previous a number of quarters, so I refer you to my earlier articles for extra particulars. Essentially the most attention-grabbing factor out of the shareholder assembly about administration of the working companies is that Warren not often takes calls from working managers anymore. These now go straight to Greg or Ajit. Additionally, in distinction to Warren’s former boasts of “laziness” in relation to addressing efficiency points within the companies, he famous that Greg is extra prone to deal with working managers “coasting”. That is one other optimistic for the way forward for Berkshire. We solely acquired one query about BNSF within the assembly, which yielded barely extra particulars on the railroad, however nonetheless not sufficient. Greg famous that following the availability chain disruptions of 2022, BNSF was sluggish to trim prices consistent with altering demand. These price chopping efforts are underway, although the low demand progress can also be an issue that was not mentioned. Trying on the different three US-based Class 1 railroads, CSX (CSX) and Union Pacific (UNP) had a lot much less of a income decline than BNSF and Norfolk Southern (NSC). With regards to profitability, BNSF declined lower than the 2 japanese railroads, however misplaced floor to its western peer Union Pacific.

Creator Spreadsheet

At Berkshire Hathaway Power, operations proceed to be overshadowed by litigation over wildfires in Oregon with plaintiffs in search of an enormous payout:

As of March 31, 2024, quantities sought within the complaints and calls for filed in Oregon and in sure calls for in California approximated $7 billion, excluding any doubling or trebling of damages included within the complaints and people settled.

Once more, I strongly encourage score Notice 23 of the 10-Q for the entire new developments in these instances, which Berkshire plans to contest vigorously.

Through the assembly, Warren and Greg made clear that it’s unsustainable for governments to carry utilities 100% accountable for hearth injury and anticipate them to proceed working of their jurisdiction.

Valuation

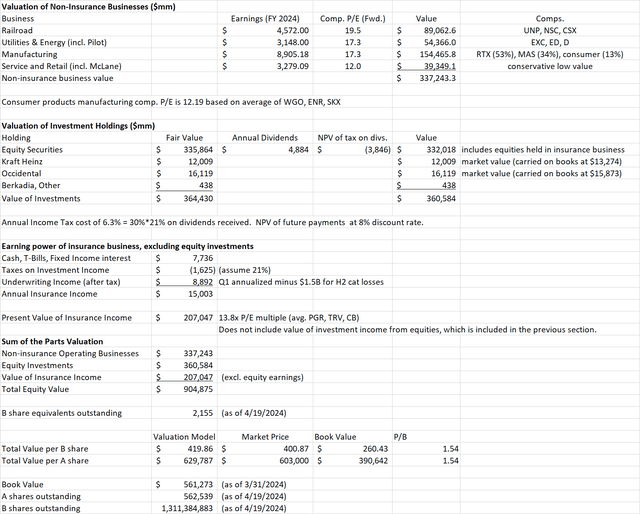

My common sum of the elements mannequin has been up to date. I’m now utilizing annualized Q1 outcomes as estimates for FY 2024 phase earnings, nonetheless I’ve subtracted $1.5 billion from the annualized insurance coverage underwriting revenue to account for giant catastrophic losses like hurricanes within the second half of the 12 months. (There have been zero cat losses to date this 12 months. There have been about $1 billion in 2023 and $2 billion every in 2021 and 2022.) Within the non-insurance companies, I acknowledge that annualizing the Q1 outcomes could also be conservative, however given the issues at BNSF and BHE, I believe this strategy is warranted.

Creator Spreadsheet

Whereas the worth of the non-insurance enterprise has come down and the worth of the insurance coverage enterprise has come up, there was virtually no change within the general valuation. This got here out to $419.86 per B share, in comparison with $419.17 final quarter.

Taking a look at worth/e book ratio, the slight enhance in e book worth since final quarter mixed with the slight drop in share worth has taken P/B all the way down to 1.54. That is again beneath the 1.6 threshold the place I take into account the inventory richly valued.

Conclusion

Maybe the passing of Charlie had centered Warren extra on making ready for the way forward for Berkshire, however this 12 months’s annual assembly offered extra perception than common about what traders can anticipate. Greg Abel will probably be a extra energetic supervisor than Warren has been, taking extra accountability for funding administration than beforehand thought. Greg could even enterprise extra into worldwide funding alternatives to offer Berkshire a greater probability to deploy the still-ballooning money hoard. Greg can also be taking a extra energetic function in managing the working companies. We’re progressively seeing extra candor about issues at BHE and BNSF however fixing them might be a multi-year effort.

Berkshire share worth has declined barely over the previous quarter, whereas my estimate of intrinsic worth has said the identical and e book worth has elevated barely. This is sufficient to nudge Berkshire inventory again into Purchase territory, together with the prospects of extra engaged higher administration sooner or later.

{kind=link}