Urupong/iStock through Getty Photos

As earnings season continues in full swing, volatility is at a year-to-date excessive as shares react sharply to earnings information. Sadly, whereas many massive caps have succeeded at successful again buyers’ belief this quarter, many small caps have faltered dramatically.

Sprout Social (NASDAQ:SPT) is on this bucket. The social media administration software program platform dropped greater than 40% after reporting Q1 outcomes. These outcomes have been accompanied, no much less, by a significant discount to current-year steering in addition to information of a CEO transition.

Upgrading Sprout Social to impartial; the bull and bear instances now steadiness out

I final wrote a bearish be aware on Sprout Social in February, when the inventory was buying and selling nearer to $65 per share. I had downgraded the inventory on the time based mostly on slowing progress fundamentals and an exceedingly costly valuation. Now, with slower progress having materialized in Sprout Social’s newest forecast and its valuation having already taken a significant beating, I am extra sanguine on the corporate’s prospects via the rest of the yr and am upgrading Sprout Social again to impartial.

At present share costs, I do see each positives and negatives for this firm. After all, many dangers that I used to be involved about once I was bearish nonetheless stay:

- Firms are slicing again on gross sales and advertising and marketing spend, and social media managers are on the chopping block. Firms are slashing their gross sales and advertising and marketing budgets – each for promoting spend in addition to the G&A headcount that helps it. Whereas social media administration as a core firm operate will proceed to see secular tailwinds, we’ll possible see retrenchment as corporations tighten their belts.

- Lack of execution chops in enterprise gross sales. A part of what made Sprout Social minimize its steering this quarter was that it acknowledged being unprepared for enterprise shopping for cycles, even supposing it is now predominantly an enterprise gross sales firm. Execution missteps might additional hamper progress charges.

- DIY competitors. Sprout Social’s instruments are helpful however not groundbreaking. Managing social media posts and operating analytics on marketing campaign efficiency may be completed with in-house instruments, or with extra general-purpose opponents like HubSpot (HUBS).

On the identical time, nevertheless, there are positives to notice:

- Massive >$50 billion TAM with secular tailwinds. Increasingly more promoting spend is shifting away from conventional codecs and into social media. Having a social media technique is actually a should in right now’s enterprise local weather.

- Excessive margin recurring income. Almost 100% of Sprout Social’s income base is SaaS, with its prospects paying recurring charges to make use of Sprout Social’s publish schedule, monitoring, and analytics instruments. This income stream additionally comes at very excessive gross margins, giving Sprout Social the system for a worthwhile software program enterprise as soon as it reaches scale.

Steering minimize and slowing progress

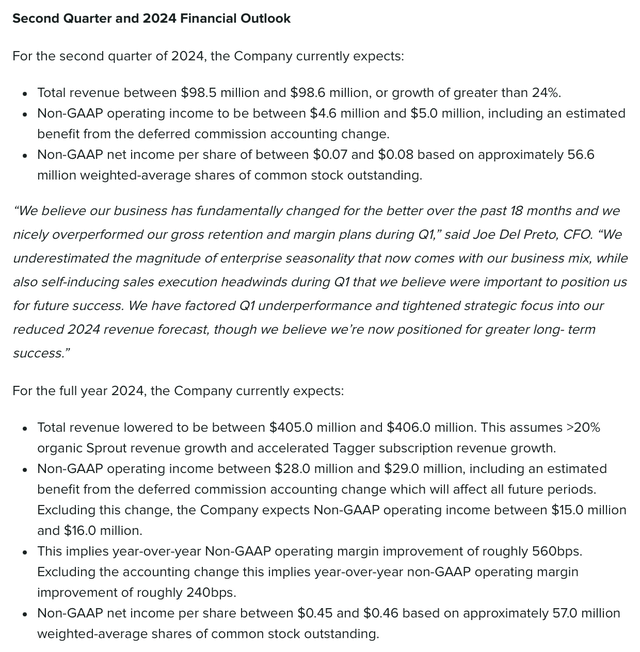

Let’s now handle the elephant within the room of why Sprout Social tanked so dramatically after earnings. The corporate tapered down its steering forecast for the yr to $405-$406 million in income, or simply 22% y/y progress on the midpoint:

Sprout Social outlook (Sprout Social Q1 earnings launch)

Its earlier outlook, in the meantime, had referred to as for $425.3-$425.5 million in income, or 27% y/y progress.

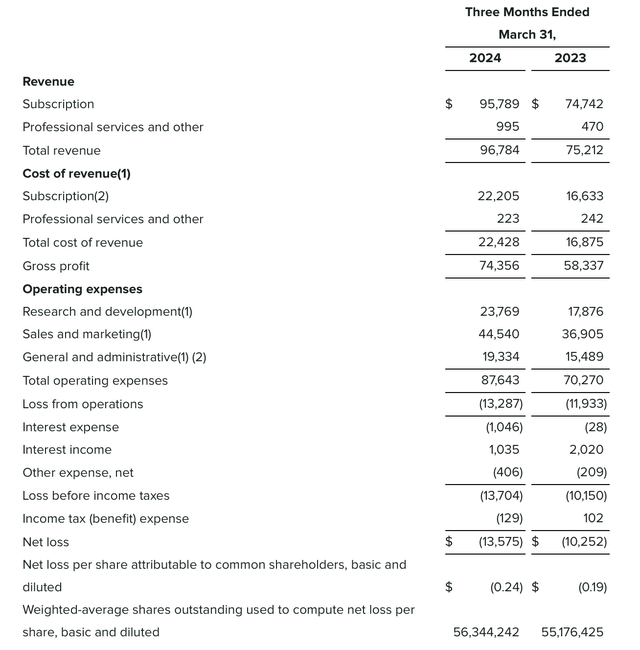

On high of the deep steering minimize, we have already began to see massive deceleration in Sprout Social’s outcomes. Income within the first quarter grew 29% y/y to $96.8 million, which missed Wall Road’s expectations of $97.3 million, in addition to decelerating 5 factors sequentially versus 34% y/y progress in This autumn.

Sprout Social Q1 outcomes (Sprout Social Q1 earnings launch)

Worse but: whereas many corporations have reported slowing progress, most have completed so out of macro pressures or different exogenous circumstances. Sprout Social, nevertheless, famous that it was ill-equipped to deal with its personal rising shift to an enterprise shopping for base. Per new CEO Ryan Barretto’s remarks on the Q1 earnings name:

We had a powerful quarter on many dimensions, however finally didn’t meet our income targets. After a report again half of 2023, the place nearly all of our focus was deeply weighted on closing offers versus creating new pipeline, we walked into 2024 with a special enterprise. We’re now enterprise-heavy and the linearity of our enterprise has modified materially, which impacts our income recognition and planning.

Our months, quarters and years are actually extra closely weighted to conventional enterprise shopping for cycles. We underestimated the magnitude of this shift and the shortly altering dynamics in our buyer combine. On high of this, we made a number of vital strategic selections heading into Q1, equivalent to constructing new vertical gross sales groups, accelerating promotions in our midmarket and enterprise groups, adjusting our account protection mannequin and prioritizing Tagger enablement for all of our customer-facing groups.

We thought we may handle these modifications with out disruption, however they collectively set us again. I consider every of those strikes assist our long-term technique and higher positions us for the longer term, however within the short-term there have been execution headwinds that have been self-induced. Though Q1 web new income added was lower than Q1 of final yr and never the place we anticipated it to be, there was loads of vital studying, progress and momentum popping out of this course of. I personal this and totally anticipate us to be a lot better going ahead.”

Barretto’s elevation to the CEO publish, from his prior function as President and head of gross sales, is a mirrored image of the corporate’s want to handle these operational challenges.

Nonetheless, nevertheless, there may be hope. The corporate famous that it grew its certified pipeline by 37% in Q1. Additionally it is transitioning its gross sales groups away from smaller, much less profitable accounts to organize to deal with extra enterprise deal move.

Profitability, as well as, is one other plus. Professional forma working revenue greater than tripled to $6.0 million within the quarter, representing a 6% professional forma working margin, from simply 2% within the year-ago quarter.

Valuation and key takeaways

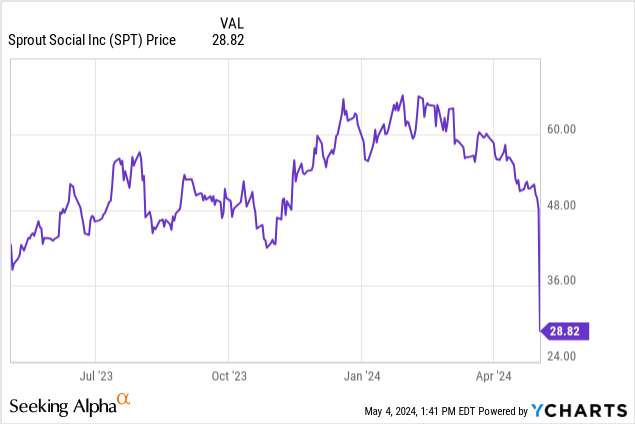

Amid the earnings fiasco, Sprout Social has additionally fallen to a way more palatable valuation. At present share costs close to $29, the corporate trades at a market cap of $1.63 billion. After we web off the $94.2 million of money and $45.0 million of debt on the corporate’s most up-to-date steadiness sheet, Sprout Social’s ensuing enterprise worth is $1.58 billion.

In opposition to the corporate’s newest $405-$406 million steering outlook for the yr, the inventory trades at simply 3.9x EV/FY24 income – when earlier this yr, it modified arms at a >8x ahead income a number of.

I would say with decrease expectations for Sprout Social, we now have a a lot safer entry alternative into this inventory. I would look forward to earnings volatility to settle, after which leap in with a small trial place.

{kind=link}