The draw back shock in US inflation paved the best way for extra positive factors in Wall Avenue in a single day (DJIA +0.25%; S&P 500 +0.74%; Nasdaq +1.15%), because the S&P 500 and Nasdaq discovered a brand new excessive since April 2022 and January 2022 respectively. Indication of market aid was mirrored with an 8.7% plunge within the S&P 500 VIX, with the index widening the hole beneath its key 20 degree and holding a risk-on surroundings in place.

Promising inflation progress within the US was displayed within the 3% learn for the headline client value index (CPI) year-on-year versus the three.1% anticipated. Extra importantly, the core studying got here in at its lowest degree since December 2021, with a 4.8% print coming in beneath the 5% forecast (earlier 5.3%). This marked the primary draw back shock in US core inflation in seven months. Month-on-month, each headline and core inflation got here in at 0.2% (0.3% anticipated).

Virtually all of the CPI parts noticed a moderation in year-on-year value progress in comparison with June 2022, extra notably with power and used vehicles costs. The one exception is in shelter costs, however on condition that the Fed is putting much less consideration on it as a result of element’s lagging nature, its persistent displaying didn’t convey a lot concern.

Total, the lower-than-expected learn in US inflation means that the tightening cycle from the Fed so far are having its desired impact in moderating pricing pressures. Fee expectations stay well-anchored for one final 25 basis-point (bp) hike from the Federal Reserve (Fed) this month and the case has strengthened for a chronic pause in tightening thereafter.

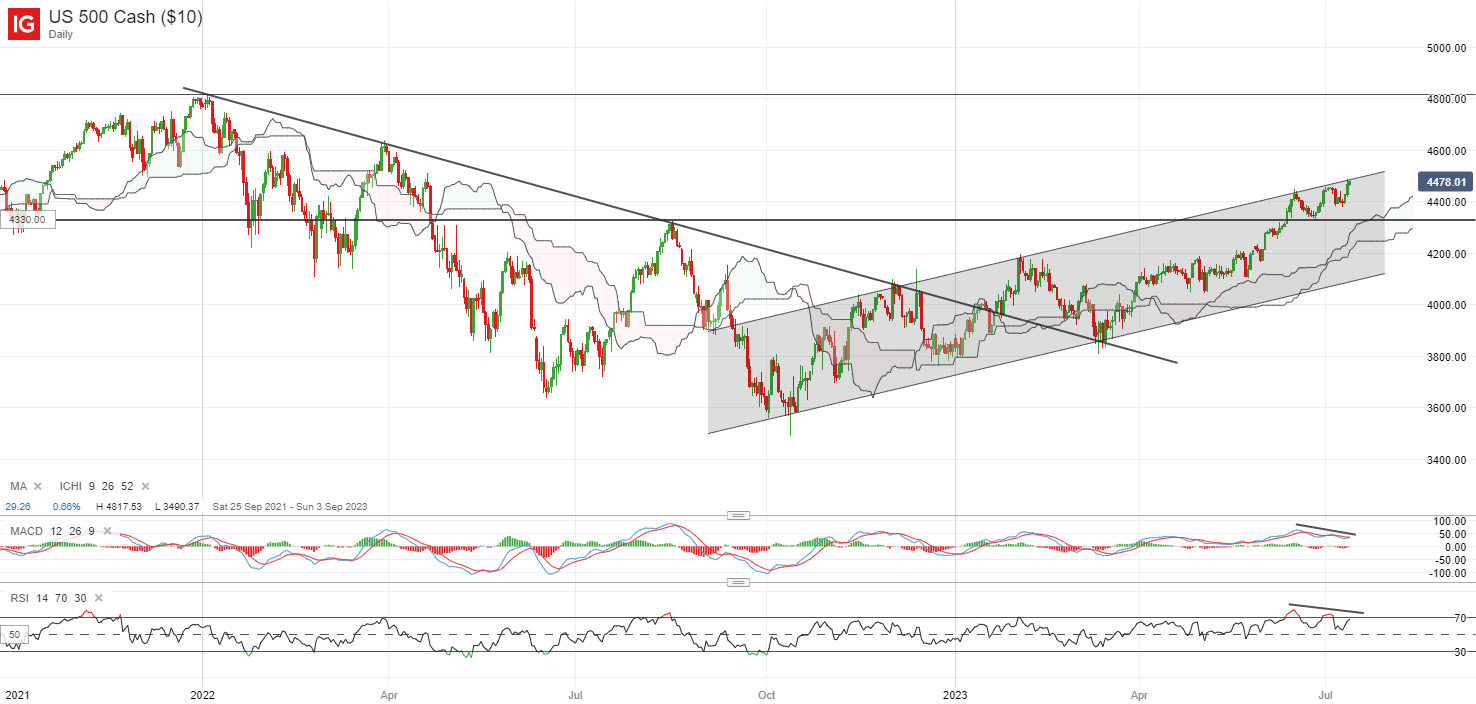

The S&P 500 is again to retest a key channel trendline resistance as soon as extra, with the formation of a brand new increased excessive in a single day reiterating its prevailing upward pattern. The chance is that any flip decrease at present cut-off date may nonetheless put a decrease excessive on its day by day Relative Power Index (RSI), with the bearish divergence pointing to some moderation in upward momentum. That mentioned, the broad pattern stays upward-bias, with any draw back doubtlessly leaving the 4,330 degree on look ahead to near-term assist.

Supply: IG charts

Asia Open

Asian shares look set for a optimistic open, with Nikkei +0.61%, ASX +1.32% and KOSPI +0.78% on the time of writing, coming off the again of abating inflation fears within the US. The Nasdaq Golden Dragon China Index is up 3.4% in a single day. Financial knowledge this morning noticed a draw back shock in New Zealand’s manufacturing actions from its Efficiency of Manufacturing Index (PMI) (47.5 versus 49.8 consensus), which validates its central financial institution’s choice to revert to a price pause yesterday on increased financial dangers.

The day forward will depart China’s commerce knowledge in focus to offer additional gauge of financial circumstances on the planet’s second largest economic system. Nonetheless-weak exterior demand is predicted to pull its year-on-year exports additional into contractionary territory at -9.5% versus the earlier 7.5%. However, imports are anticipated to contract to a lesser extent at -4% versus the earlier -4.5%, however it will likely be unlikely to offer a lot conviction for a transparent restoration in place. The general weak displaying in commerce actions, in step with the latest subdued inflation knowledge, should reinforce hopes for extra to be carried out.

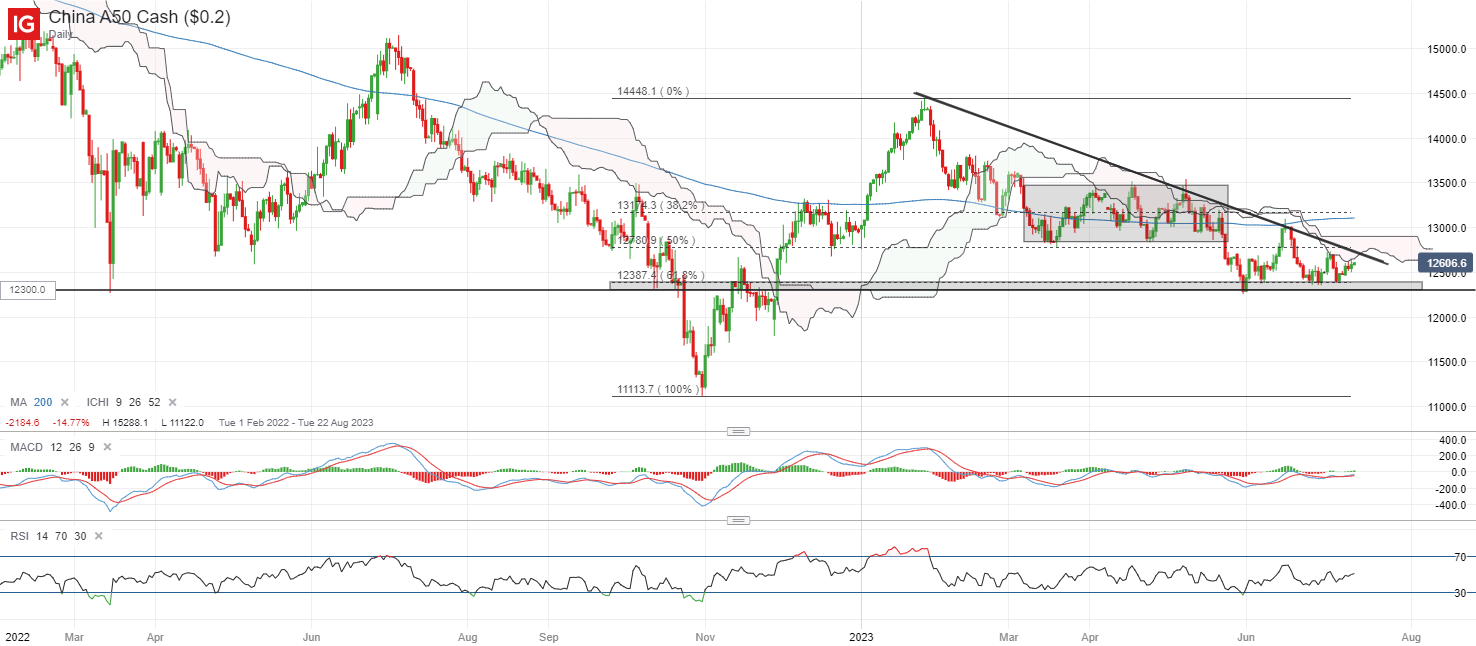

Up to now, the China A50 index has been buying and selling inside a descending triangle sample since November final yr, with the bottom doubtlessly shaped on the 12,300-12,375 vary. With the index inching nearer in the direction of the triangle apex, a key choice could should be made, the place the downward trendline resistance will problem patrons whereas the triangle base assist will function assist for sellers to beat. Any breakdown of the 12,300 degree to a brand new decrease low may reinforce its prevailing downward pattern and doubtlessly depart its November 2022 backside on look ahead to a retest.

Supply: IG charts

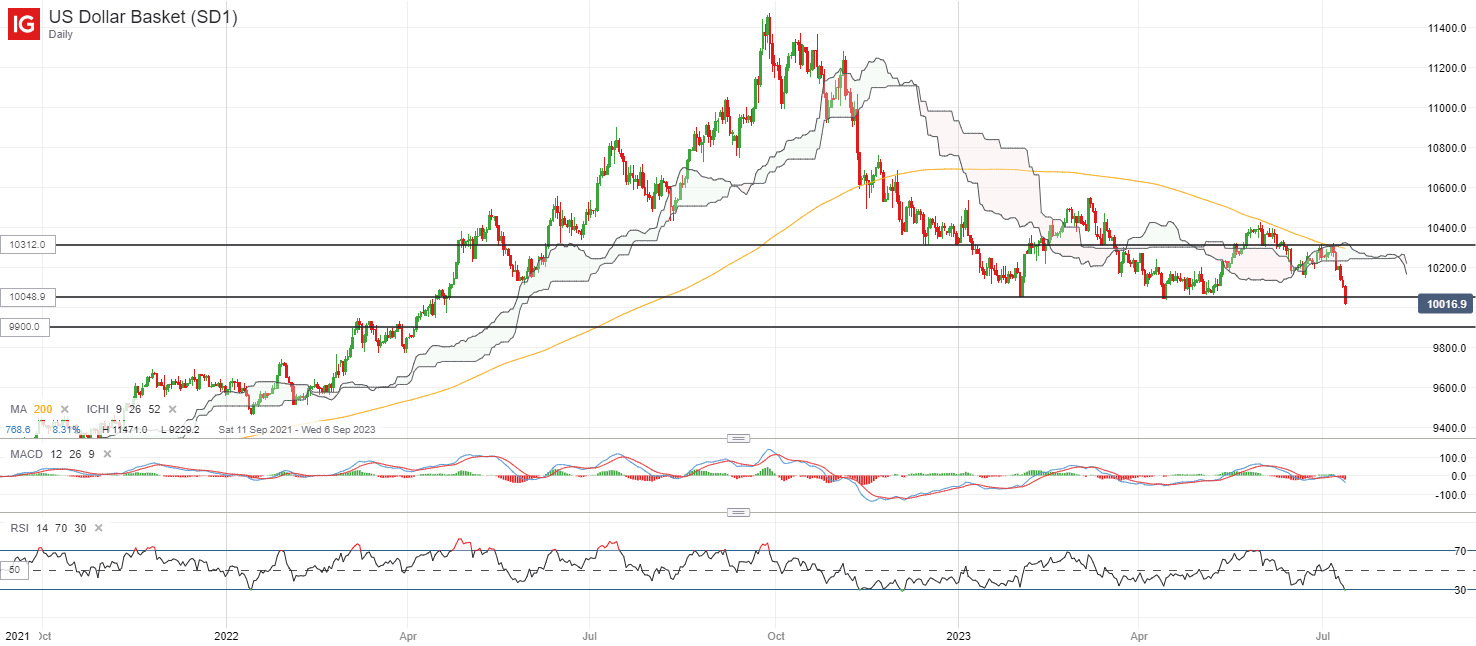

On the watchlist: US greenback index plunged to a brand new 14-month low

US Treasury yields reacted sharply to the draw back within the aftermath of the lower-than-expected US inflation learn, which dragged the US greenback index to its lowest degree since April 2022. On the technical finish, its transferring common convergence divergence (MACD) has reversed decrease on the day by day chart after failing to cross above the important thing zero line this week, whereas the RSI was additionally dragged additional beneath the important thing 50 degree, each reinforcing bearish momentum in place.

After trying to stabilise and type a base since February this yr, the breakdown to a brand new decrease low appears to strengthen the case for a continuation of the broader downward pattern. The 100.50 degree will now flip right into a earlier support-turned-resistance degree to beat, whereas additional draw back could depart the 99.00 degree on watch subsequent.

Supply: IG charts

Wednesday: DJIA +0.25%; S&P 500 +0.74%; Nasdaq +1.15%, DAX +1.47%, FTSE +1.83%

Article written by IG Strategist Jun Rong Yeap

{kind=link}