bluejayphoto

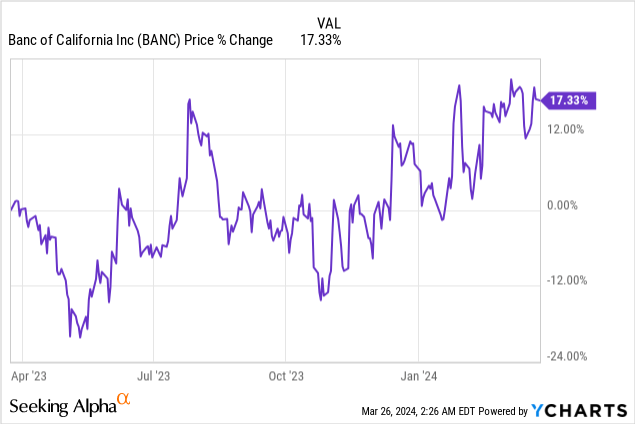

Banc of California (NYSE:BANC) makes a horny worthwhile place for financial institution buyers as shares present a horny 3% dividend yield and the regional lender retains promoting for a horny low cost to its long run common P/B ratio. Banc of California owns a well-performing core mortgage portfolio with a really sturdy asset high quality profile and the financial institution has upside revaluation potential associated to an enchancment in its web curiosity margin. With shares persevering with to commerce properly under e-book worth, I imagine Banc of California is a promising wager on an upside revaluation in 2024.

Earlier ranking

I rated shares of Banc of California, in December 2023, a purchase because of what I believed was a really smart transaction relating to the property of PacWest Bancorp, the struggling regional financial institution that was pushed to the brink after SVB needed to be rescued final yr. Though Banc of California didn’t elevate its dividend as I projected in Q1’24, the financial institution faces numerous catalysts for earnings development this yr, particularly because it pertains to the discount of high-cost borrowings. Now that the regional lender has closed the acquisition of PacWest Bancorp, BANC has a possibility to develop its web curiosity margin and additional shrink its stability sheet.

Properly-performing core mortgage portfolio with low NPLs

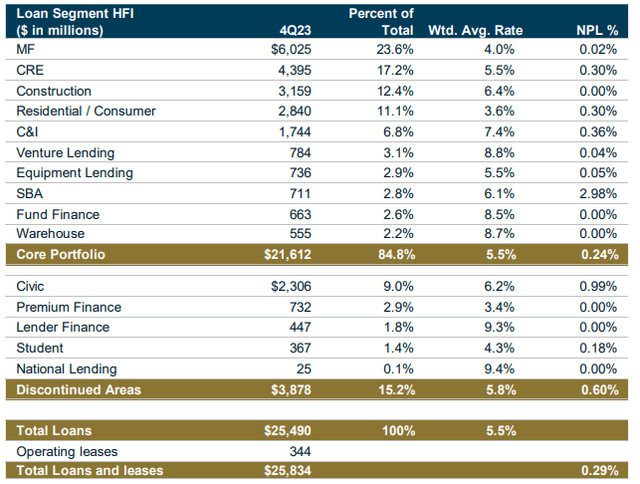

Banc of California is now the fourth-largest deposit franchise within the state of California with complete deposits of $30.4B. The core worth offered by an funding in Banc of California is its mortgage portfolio which has a really low share of non-performing loans in it. Nearly all of investments in Banc of California’s portfolio are, following the acquisition of PacWest Bancorp, multi-family and business RE loans which collectively represented $10.4B (41% of complete loans). The common share of non-performing mortgage stood at solely 0.24% (non-weighted) on the finish of FY 2023. Banc of California had $4.4B of its loans invested within the CRE market which represented 17.2% of investments. Whereas this share could appear excessive, solely 25% of CRE loans had been made within the workplace class ($1.1B) and no workplace mortgage was delinquent as of This fall’23.

Banc of California

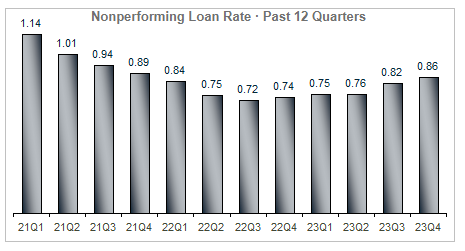

Banc of California’s asset high quality, as measured by the NPL ratio, can be considerably higher than that of the U.S. banking business as an entire. The standard of property held on banks’ stability sheet did deteriorate a bit since Q3’22, however the business as an entire isn’t coping with a big non-performing mortgage points.

Bankregdata.com

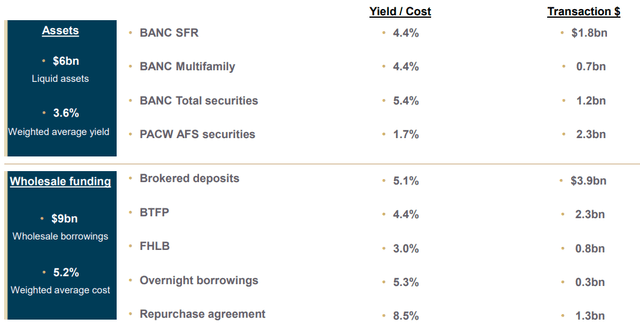

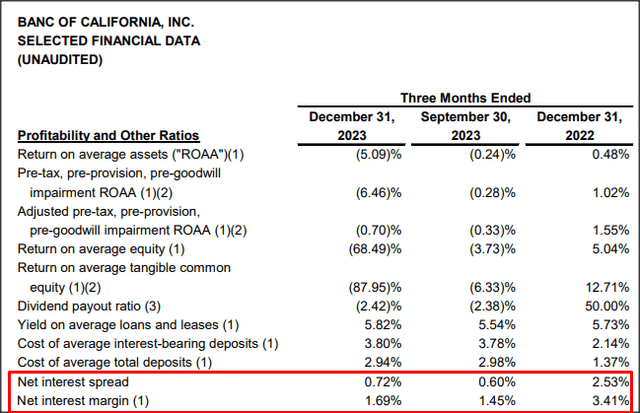

After the closing of the PacWest Bancorp transaction, Banc of California has engaged in numerous transactions to cut back the scale of its stability sheet. The California-based lender offered $6.0B of its property (together with securities) and diminished its high-cost wholesale borrowings by $9.0B (with a median value of 5.2%)… which is about to have a constructive impression on the regional lenders’ web curiosity margin in 2024. In This fall’23, Banc of California diminished its borrowings by $3.4B quarter over quarter to $2.9B.

Banc of California

The largest take-away from the financial institution’s fourth-quarter earnings sheet was the discount in high-cost quick time period borrowings, and BANC reported a better web curiosity margin because of this. Banc of California achieved a web curiosity margin of 1.69% within the fourth-quarter, displaying a rise of 0.24 PP quarter over quarter. The regional lender didn’t present any steerage for its web curiosity margin, however the discount of high-cost debt would have a constructive impact on the financial institution’s NIM. Banc of California might proceed to repay high-cost borrowings in FY 2024, of which there have been $2.9B as of This fall’23, and thereby generate a constructive NIM catalyst which might additionally assist shares revalue larger. This is able to clearly make a whole lot of sense and may very well be an earnings development catalyst for BANC this yr. The financial institution’s progress when it comes to eradicating high-cost funding sources in addition to BANC’s web curiosity margins are two areas that I imagine are value monitoring.

Banc of California

Banc of California’s valuation and repricing potential

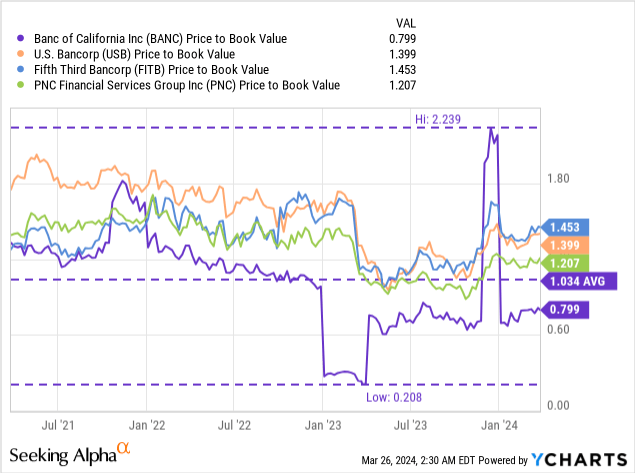

Apart from the well-performing mortgage portfolio and potential for NIM enlargement associated to discount of high-cost debt, one more reason to think about Banc of California pertains to the financial institution’s low valuation based mostly off of e-book worth. Traditionally, Banc of California has traded at a a lot decrease price-to-book ratio than its rivals within the regional banking market, largely as a result of the financial institution is concentrated in California which is thought for its scorching business actual property market.

At the moment, shares of Banc of California are valued at a P/B ratio of 0.80X which compares to a lot larger P/B ratios for its extra diversified rivals. Fifth Third Bancorp (FITB), U.S. Bancorp (USB) in addition to PNC Monetary Providers (PNC) all commerce at premiums to e-book worth because of their broader working footprints.

Banc of California is concentrated in California which is thought for its scorching actual property market and buyers have been anxious about CRE publicity of regional lenders, particularly these with investments in California and New York, which possible explains the bigger low cost to e-book worth.

Banc of California additionally trades properly under its 3-year common P/B ratio of 1.03X. For my part, Banc of California might simply commerce at e-book worth given its sturdy mortgage portfolio and better historic valuation ratio. A 1.0X P/B ratio calculates to a good worth of $17.12 which means 17% upside revaluation potential. My truthful worth estimate has not modified since my final protection of the lender and it’s usually tied to the financial institution’s e-book worth. So except there’s a main change in e-book worth, my truthful worth calculation shouldn’t be considerably affected going ahead.

Traders get to gather a pleasant 2.7% yield

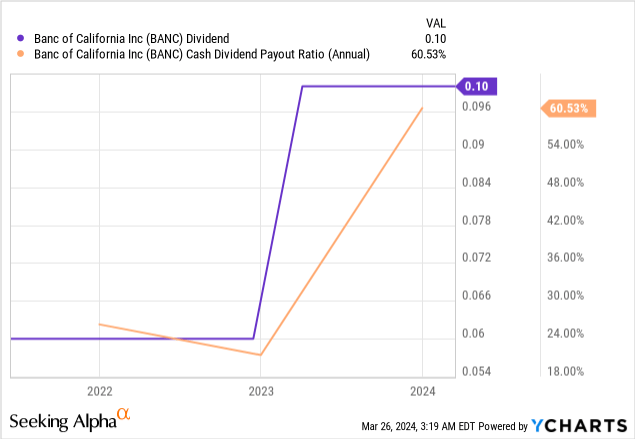

Banc of California pays a quarterly dividend of $0.10 per-share which means a dividend yield of two.7%. The dividend can be well-covered by the financial institution’s earnings with a money dividend payout ratio of 60%. I did anticipate the financial institution to develop its dividend in Q1’24 which sadly didn’t materialize. The explanation for that is possible the latest integration of PacWest Bancorp into the financial institution’s operations.

Dangers with Banc of California

A failure to shrink the financial institution’s stability sheet might lead to a scenario wherein the financial institution’s NIM enlargement might not materialize. The largest danger for Banc of California is a reset of the federal fund fee, for my part, which means rising NIM margins dangers for the financial institution simply at a time when it’s shrinking its stability sheet to spice up its NIM.

Remaining ideas

Banc of California is dealing with numerous earnings catalysts in FY 2024 which embrace the shrinking of its stability sheet and the discount in high-cost borrowings. The Federal Reserve can be set to pivot when it comes to the federal fund fee (which poses headwinds to the financial institution’s web curiosity margin), however I imagine the deep low cost to e-book worth is wholly undeserved given the top quality of the mortgage portfolio, and will reverse over time. Traders are getting paid an honest 3% dividend till a share worth revaluation happens, so I imagine the danger profile for Banc of California general remains to be very favorable!

{kind=link}