ugurhan

By Warren Patterson

The chance of disruption to Center Jap provide grows

Whereas worth motion within the oil market has been considerably shocking following Iran’s assault on Israel, the danger of tensions within the Center East impacting oil provide is definitely rising.

The shortage of worth energy following Iran’s latest assault is essentially as a result of a big threat premium already having been priced into the market. ICE Brent rallied from slightly greater than US$86/bbl initially of April to over US$90/bbl in anticipation that Iran would reply to Israel’s suspected airstrike on its embassy in Syria. Secondly, the market can also be in limbo, ready to see how Israel responds to the latest assault. The longer the market waits for Israel’s response, the extra possible the danger premium begins to fade.

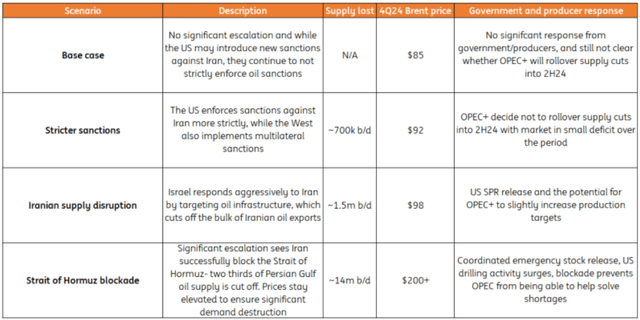

Dangers to grease provide due to the ongoing stress within the Center East are at their highest since October final yr. Any additional escalation would solely convey the oil market nearer to precise provide losses. We consider there are three key provide dangers dealing with the oil market on account of present tensions. These embody stricter enforcement of oil sanctions towards Iran, Israel retaliating by concentrating on Iranian vitality infrastructure, and the worst-case situation – that important escalation ultimately sees Iran making an attempt to dam or disrupt oil flows by means of the Strait of Hormuz.

Potential situations and what these may imply for oil provide & costs

ING Analysis

Stricter sanctions enforcement

Israel’s allies are pushing for a diplomatic response to Iran’s assault, though it might seem that Israel is a probably extra aggressive method.

The US and Europe are probably imposing stricter sanctions towards Iran following the assault. The US already has oil sanctions in place towards Iran.

The problem is that the US has not strongly enforced these sanctions since Russia’s invasion of Ukraine, given issues over oil provide and better costs. Because of this, the Iranian oil provide has grown from a mean of slightly over 2.5m b/d in 2022 to shut to three.2m b/d in March 2024. If the US have been to correctly implement sanctions, it might go away round 700k b/d of provide in danger.

There may be potential for additional provide losses as a result of sanctions. Legislators within the US are contemplating a invoice known as the Iran-China Power Sanctions Act, which might try and crack down on Iranian oil flows to China. There may be additionally scope for the EU and different allies to agree on multilateral sanctions, which might solely make it tougher to maneuver Iranian oil.

Whereas new sanctions is likely to be launched, the important thing query is whether or not these sanctions will probably be extra strictly enforced. There will probably be issues over the potential affect provide losses may have on oil costs, and the Biden administration wouldn’t need to see greater oil costs and pump costs within the lead-up to US elections later within the yr.

If we have been to see stricter enforcement of sanctions, this isn’t one thing that may change into instantly obvious to the oil market. It’s going to take time for it to change into noticeable in tanker monitoring knowledge.

Shedding within the area of 700k b/d of Iranian oil provide can be sufficient to push the oil market right into a small deficit over the second half of the yr, which might suggest ICE Brent averaging US$92/bbl in 4Q24 versus our present forecast of US$85/bbl for the ultimate quarter of the yr. That is below the idea that OPEC+ decides towards rolling over provide cuts into the second half of the yr.

Iranian provide disruptions

With it nonetheless unknown how Israel will reply to Iran’s assault, we can not totally rule out the potential for Israel to focus on Iranian vitality infrastructure. Iran is a crucial oil producer, with it being the fourth-largest OPEC member, pumping shut to three.2m b/d. Any concentrating on of Iranian vitality would possible present a lift to grease costs.

We consider the probability of Israel concentrating on vitality infrastructure is quite small. This may not go down properly with allies, given the affect it might have on oil costs.

If we assume that the majority of Iranian oil exports are halted, we may see Brent common slightly below US$100/bbl in 4Q24.

Iranian escalation and the Strait of Hormuz

The worst-case situation for the oil market can be if we noticed escalation to an extent the place Iran makes an attempt to impose a blockade by means of the Strait of Hormuz. The Strait of Hormuz is an important chokepoint globally for oil commerce. Slightly over 20m b/d of oil flows by means of the Strait, with exports from key producers Saudi Arabia, Iraq, Iran, the UAE, Kuwait and Qatar.

We consider the probability of a blockade is low, given firstly, it might be tough to impose, secondly, it might not be in Iran’s personal curiosity, and at last, it might possible see a powerful world response. Nevertheless, it’s nonetheless value exploring the affect.

The potential affect would dwarf the disruptions we now have seen within the Purple Sea in latest months, given the amount of oil that flows by means of the Strait and in addition as a result of the truth that there isn’t a different route for the majority of those oil exports. As we talked about in a word earlier within the yr, Saudi Arabia does have 5m b/d of pipeline capability, which might enable crude to be carried to the Purple Sea and exported from there, whereas the UAE has a pipeline with capability of 1.5m/b/d which might enable for the export of oil from the Gulf of Oman, so avoiding the Strait. This nonetheless leaves roughly 14m b/d of oil provide in danger within the occasion of a blockade.

This may result in a major worth shock the place we may see Brent break above US$200/bbl by the top of the yr, given the numerous drawdown we’d see in world shares. Costs would want to stay elevated to make sure important and fast demand destruction, and any provide response from different producers would take time.

How may provide losses be handled?

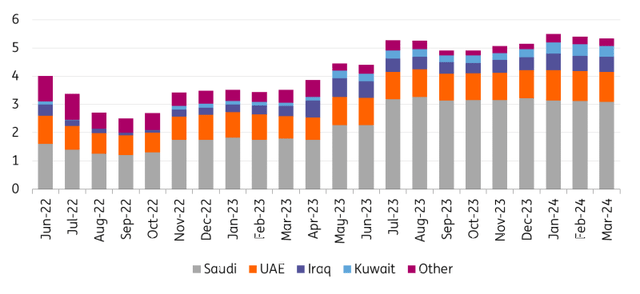

The power of the market to reply to any potential provide disruption would rely upon the severity of any provide cuts. Provided that OPEC is sitting on greater than 5m b/d of spare manufacturing capability, which means that the market ought to be well-placed to reply to most provide hits. It will largely rely upon the willingness of OPEC to extend provide. The group will possible change into more and more involved about potential demand destruction if costs transfer too excessive, sustainably above $100/bbl.

OPEC spare capability would have the ability to assist the worldwide market within the case of stricter sanctions towards Iran or any important provide disruption from Iran. The place this spare manufacturing capability doesn’t assist, is that if there was a blockade of the Strait of Hormuz – the majority of spare capability sits inside the Persian Gulf. Saudi Arabia, the UAE, Iraq and Kuwait maintain 95% of whole OPEC spare capability.

Any important provide shocks would additionally possible result in a coordinated world launch of shares from emergency reserves. Whereas the US has drawn down considerably on its strategic petroleum reserve (SPR) since Russia’s invasion of Ukraine, the SPR nonetheless stands at greater than 360m barrels, leaving it with the choice to faucet into this.

Considerably greater costs would additionally guarantee there’s a clear incentive for producers elsewhere to extend drilling exercise. Whereas US producers can be the quickest to reply, it might nonetheless take a number of months for elevated drilling exercise to feed by means of to greater oil provide.

The important thing takeaway is that the oil market from a provide perspective ought to have the ability to cope comparatively properly with any disruptions/losses to Iranian provide. The place it turns into more and more tougher for the market is that if Persian Gulf provides are misplaced as a result of a blockade of the Strait of Hormuz.

OPEC has loads of spare capability, however 95% of it sits within the Persian Gulf (m b/d)

IEA, ING Analysis

Content material Disclaimer

This publication has been ready by ING solely for info functions no matter a selected person’s means, monetary scenario or funding goals. The knowledge doesn’t represent funding advice, and neither is it funding, authorized or tax recommendation or a proposal or solicitation to buy or promote any monetary instrument. Learn extra

Authentic Submit

{kind=link}