J Studios

Introduction

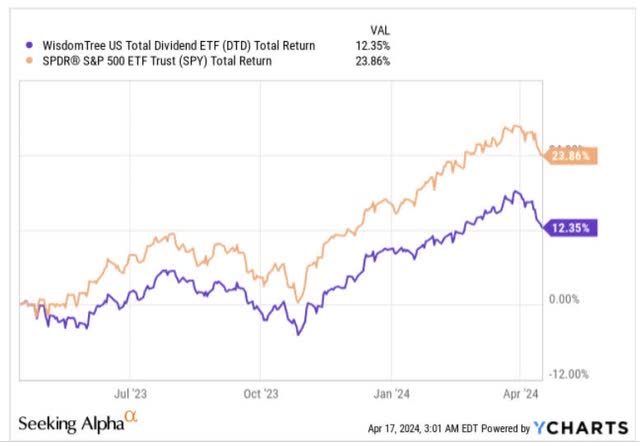

The WisdomTree Whole US Dividend ETF (NYSEARCA:DTD), a $1.16bn sized product that seeks to cowl over 800 all-cap dividend-paying shares from the US, has not been in dazzling type over the previous yr. For context, during the last 12 months, it has managed to generate a little bit over ~12% returns, which is roughly solely half as a lot as what the important thing benchmark has delivered.

YCharts

Trying forward, we aren’t totally satisfied there will be a shift on this narrative. Nonetheless, listed below are just a few explanation why we aren’t notably enthusiastic about DTD.

A Few Causes Why We’re Not Moved by DTD

This isn’t a criticism per se, however do observe that DTD solely focuses on US shares (together with REITs), and would not think about ADRs (American Depository Receipts), or GDRs (International Depository Receipts). Additionally, the intention right here is to not simply randomly select dividend-paying shares throughout totally different market-cap spectrums (though the majority of the portfolio is tilted in direction of large and large-caps, which collectively account for 70% of the whole portfolio), however to additionally incorporate some elementary and momentum screeners earlier than developing with the eventual portfolio.

DTD’s shares are ultimately dividend-weighted each December (primarily a operate of the projected money dividend that will probably be paid by each inventory, relative to the mixture money dividends of all of the constituents), however earlier than that takes place, potential shares additionally want to realize a sure composite danger issue rating.

This danger issue rating is equally-weighted between high quality and momentum, the place the latter takes under consideration metrics equivalent to ROE, and ROA readings, gross revenue over property, and money circulation over property. We stay unconvinced if the latter two metrics are acceptable sufficient to determine high quality amongst monetary shares, as these firms usually are not overly incentivized to both generate excessive gross earnings or generate and park a whole lot of idle money relative to their asset base.

The opposite level to notice is that the momentum issue appears at risk-adjusted returns over 6 and 12 months, and this might imply, there is a good probability you find yourself with some overextended and dear shares which have already loved their time within the solar.

In truth, do observe that DTD’s ahead valuations usually are not too compelling, with Morningstar information pointing to a P/E of over 17x. In distinction, should you have a look at the valuations of the most well-liked US dividend ETF round – the Schwab U.S. Dividend Fairness ETF (SCHD), with $53bn in AUM, it may be purchased at a less expensive P/E of 13.8x.

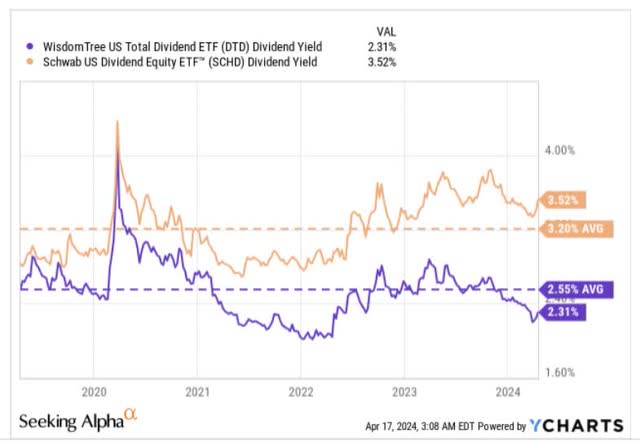

SCHD additionally trumps DTD in a whole lot of different features. Firstly, it’s much more economical, and could be accessed at an expense ratio of simply 0.06%; that’s over 4x decrease than what DTD prices at 0.28%. Since these are dividend-themed merchandise, you are additionally hoping for some compelling earnings yield figures, however observe that DTD’s present yield of two.3%, is not only decrease than its personal 5-year common of two.55%, but in addition round 130bps decrease than what SCHD provides (observe that SCHD additionally yields a determine that’s round 30bps higher than its 5-year common), dampening the lengthy case even additional.

YCharts

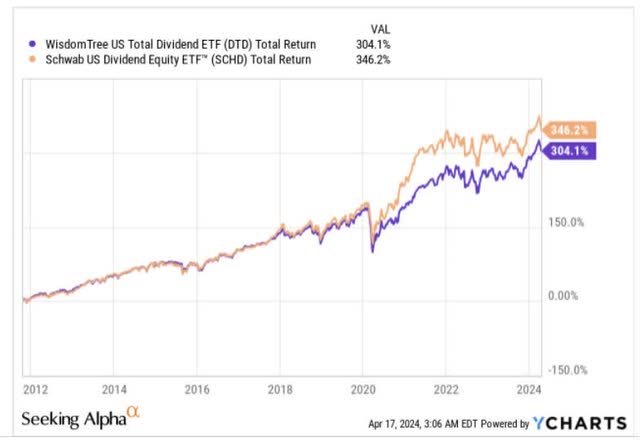

Then, once we evaluate the efficiency of those two merchandise since SCHD got here to the market (SCHD obtained listed round 5 years after DTD), it makes us surprise even additional if that is one of the best decide on this house.

Firstly, on a complete return foundation, we are able to see that DTD has lagged SCHD for the reason that latter got here to the market.

YCharts

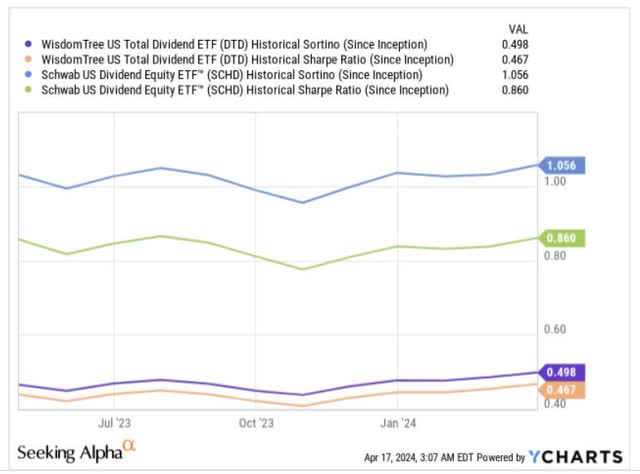

It is not simply the variability within the whole returns that is value noting. Even from a risk-adjusted return perspective, DTD comes throughout because the weaker possibility. The picture beneath gives some context on how successfully these two merchandise have sought to generate extra returns (returns over the risk-free charge), when coping with their very own commonplace deviations and draw back deviations. The Sharpe ratio measures the surplus return potential in mild of the whole danger taken, and right here DTD’s studying is just not even half pretty much as good as SCHD’s. The Sortino ratio gauges the standard of returns when solely draw back deviation is worried, and right here the hole between the 2 merchandise is lesser, however nonetheless SCHD comes out on high.

YCharts

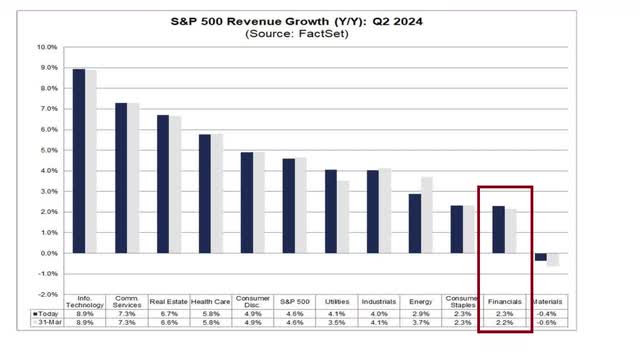

Additionally observe that DTD’s high sector publicity is in direction of the monetary sector, and we do not really feel prospects right here look too shiny, notably so far as the distributions are involved. At this stage of the cycle, we’re seeing a spike in charge-offs, which can immediate banks to put aside extra funds for provisioning. The online curiosity earnings (NII) trajectory too appears to be declining as greater deposit prices begin making their presence felt. Within the present quarter, do not count on any fireworks on the topline as banks are poised to ship one of many lowest topline prospects (round 2% topline development), which is healthier than solely the supplies sector.

FactSet

Crucially, it appears just like the Basel III endgame framework might also trigger banks to not be overly beneficiant with their dividend distributions going ahead.

Closing Ideas – Technical Issues

The developments on DTD’s weekly chart additionally recommend that now wouldn’t be a good time to purchase this product. Firstly, observe that the R:R is just not nice because the ETF is now a great distance from its upward-sloping assist (crimson line). Secondly, we have simply seen the 22-week intermediate trendline (black line) give manner, adopted by some fairly sizeable crimson candles, handing the initiative to the bears. The following check will probably be to see how DTD fares because it approaches and trades across the $64-$65 ranges, which had beforehand served as a key pivot level in Jan 2022, April 2022, July 2023, and Dec 2023/Jan 2024.

Investing

{kind=link}