Torsten Asmus/iStock by way of Getty Photographs

First Quarter Market Dialogue

The narrative available in the market has gone from discuss of a ‘laborious touchdown’ (deep recession) to a ‘tender touchdown’ (gentle recession) and now probably ‘no touchdown’ (no recession) in any respect. Add to that buyers’ hope the financial system might get a lift from decrease Federal Reserve coverage charges, federal infrastructure spending, and/or productiveness will increase pushed by AI know-how, and it’s no shock that danger aversion appeared to evaporate within the first quarter.

Reduction {that a} recession is perhaps averted and pleasure for potential financial re-acceleration pushed the S&P 500 Index up 10.56% within the first three months of the yr, whereas the Russell Midcap® Index rose 8.6%.

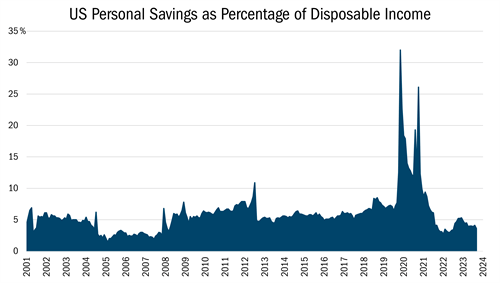

After all, this pleasure overlooks the appreciable prices and time that can be required to realize speculated future AI-related productiveness advantages. It additionally belies cracks within the basis of the financial system that shouldn’t be ignored. Within the aftermath of the worldwide pandemic, for instance, households have drained down their extra financial savings, with private financial savings as a proportion of disposable earnings now at traditionally low ranges (see chart beneath).

| Supply: Bloomberg, Month-to-month Knowledge from 6/1/2001 to 2/29/2024. This chart represents US Private Financial savings as Proportion of Disposable Revenue. All indices are unmanaged. It’s not doable to take a position straight in an index. Previous efficiency doesn’t assure future outcomes. |

Shoppers aren’t simply saving much less, they’re borrowing extra too. Auto loans, borrowing towards 401(okay)s, and bank card balances are all on the rise, as are delinquencies on repaying that debt. Shoppers shouldn’t be the one concern. Greater than $2 trillion of economic actual property debt is ready to mature between now and the top of 2028, suggesting the potential for rising defaults in that house but distressed business property gross sales stay muted.

We aren’t fully satisfied of the ‘no touchdown’ narrative that’s dominating the markets. Nevertheless, we additionally perceive it’s one doable final result on a spectrum of many eventualities. We can not enable these macro inquiries to drive our resolution making as a result of the solutions are unknowable, and the fairness market is a discounting mechanism. As such, our job is to allocate capital in direction of essentially the most engaging alternatives within the midcap worth universe whereas managing danger by sound portfolio development.

Attribution Evaluation

The Mid Cap Worth (MUTF:HRMDX) (MUTF:HNMDX) portfolio gained roughly 5.7% within the first quarter, lagging the Russell Midcap® Worth Index, which was up 8.2%. Many of the underperformance was pushed by a low hit price on our inventory choice in Financials and Industrials, the place our Technique trailed benchmark constituents.

Our underperformance was pushed by the securities we maintain and by the ‘alternative value’ of not proudly owning sure different shares throughout the midcap universe. The latter headwind was notably noticeable in Financials, the place securities that seem misplaced within the Russell Midcap® Worth Index together with Coinbase International, Inc. (COIN), Robinhood Markets, Inc. (HOOD), Block, Inc. (SQ), and SoFi Applied sciences Inc. (SOFI) make up greater than 6% of the sector.

Within the first quarter, cryptocurrency-related shares Coinbase and Robinhood noticed their shares surge greater than 50% as the worth of digital tokens jumped. Our dedication to attractively priced, well-run corporations with robust fundamentals—guided by our 10 Ideas of Worth Investing™—prevents us from proudly owning these companies, and we’re fairly snug with this positioning. We consider that our efforts are higher spent figuring out undervalued shares of financially robust companies, even when it takes time for the markets to see their true worth.

Relating to companies we owned that had been detrimental to efficiency, First American Monetary Company (FAF) within the Financials sector and J.B. Hunt Transportation Companies, Inc. (JBHT) within the Industrial sector had been detractors to total efficiency. Each are industry-leading cyclical companies at the moment working by the weak level of their enterprise cycles, together with title insurance coverage within the case of FAF and freight transportation within the case of JBHT. Our thesis for proudly owning each stays unchanged.

Portfolio Exercise

We assemble our portfolio for the long run with a balanced and bottom-up strategy. Overlaying our 10 Ideas of Worth Investing™, we implement a two-bucket technique by looking for to personal each high-quality corporations buying and selling at first rate bargains (“high quality worth”) and deeply discounted corporations which have produced poor financial returns over time (“deep worth”). We do that as a result of these two types inside worth investing are inclined to alternate market management, simply as development and worth methods usually take turns outperforming.

Immediately’s financial backdrop affords a superb illustration of how the two-bucket strategy may be helpful. Whereas we’re skeptical that buyers’ expectations of a ‘no touchdown’ situation will unfold exactly as anticipated, we can also’t say for sure that typical knowledge is mistaken. If the market continues in a ‘danger on’ mode, deep worth securities might have an outsized profit. Alternatively, if the financial system is weaker than present market expectations, capital is prone to favor high quality worth traits together with excessive returns on capital, strong free money circulate, and pricing energy. That stated, we query whether or not the market can pay any worth for these attributes, which regularly appeared to be the case within the pre-2022 rate of interest atmosphere.

The next are two examples of recent holdings within the high quality worth class and one instance of a detractor within the deep worth bucket:

Industrials

Donaldson Firm Inc. (DCI), a filtration producer with greater than a century of expertise in air, lubricant, hydraulic, and gasoline filtration purposes, is a brand new place this quarter.

DCI, an instance of a inventory in our high quality worth bucket, sometimes trades at a premium to its friends, a sign of the market’s appreciation for its economically resilient revenues and excessive revenue margins. Nevertheless, the corporate has confronted margin headwinds recently, partially owing to heavy upfront funding in its fast-growing life sciences section. Furthermore, a number of of DCI’s cyclical finish markets, together with agricultural, mining, and development gear, have been underneath strain as decrease gear utilization has translated into fewer filter replacements.

We predict buyers have already included the life sciences working losses within the firm’s valuation, however we consider the section will finally be accretive to income development and margins. If life sciences working margin approaches the company common of round 15% over the subsequent two years, that might translate to a 10-15% raise in complete earnings energy. For context, this section’s working margin exceeded 20% previous to the present funding section.

Buyers don’t sometimes gravitate to industrials when the ISM Manufacturing Buying Managers Index is declining, as was the case from late 2021 by late 2023. Donaldson, nonetheless, has traditionally outperformed in eventualities when industrial exercise weakens owing to a income base that’s largely consumable. This makes Donaldson a superb instance of a inventory that might carry out properly on a relative foundation if the financial system slips right into a recession whereas offering important upside potential if the financial system continues to develop.

DCI is buying and selling at parity as we speak, implying that the market is already pricing in additional earnings strain whereas we anticipate the life sciences operational enchancment to assist buffer potential revenue danger within the firm’s cyclical finish markets.

Shopper Staples

One other new place is The Hershey Firm (HSY), the main chocolate confectionary firm in North America with a rising presence in salty snacks and non-chocolate confections.

The maker of such widespread manufacturers as Hershey’s, Reese’s, Cadbury, and Jolly Rancher has traditionally traded at a premium to its client staples friends. However in an atmosphere the place client funds are burdened and enter prices are climbing, that premium has disappeared. The inventory is down 35% from its 2023 peak attributable to quantity headwinds and margin pressures caused by rising costs.

We consider Hershey merely must display to buyers that these headwinds are cyclical and momentary in nature, whereas as soon as once more showcasing its skill to stability superior profitability with modest development and steady market share. Cocoa costs, a key enter for HSY, have seen a virtually unprecedented worth spike on provide disruptions in West Africa (the place the vast majority of international provide originates). Whereas we can not predict when cocoa costs deflate, we’re assured HSY and its largest opponents can be gradual to reverse worth will increase required to recoup the enter value squeeze. Encouragingly, after being hampered by provide chain constraints within the post-COVID-19 atmosphere, HSY has a better innovation slate and extra capability in place to develop within the coming years. The inventory, in the meantime, now trades close to historic lows relative to different blue chip client staples, the buyer staples sector as an entire, and the broad market.

Healthcare

Perrigo Firm PLC (PRGO) is an current deep worth holding that has slumped recently, however we’re inspired by the self-help progress.

Shares of the buyer well being firm, with private-label manufacturers spanning allergy and ache aid to digestive well being merchandise, fell in response to information that the associated fee to remediate its toddler formulation vegetation will run larger than anticipated. Final September, the Meals and Drug Administration up to date {industry} tips for the company’s strategy to inspections and compliance for toddler formulation manufacturing. This included extra frequent cleansing of producing amenities, leading to a slowdown in manufacturing.

Whereas the inventory reacted to the disappointing toddler formulation replace (which impacts 12% of firm gross sales), we took away notable positives from PRGO’s earnings replace together with clear indicators of progress on market share, margins, and free money circulate era. Extra just lately, shares have recovered after the CEO appeared at an {industry} convention and reported faster-than-expected progress made on toddler formulation remediation. Ongoing progress on the problem ought to assist refocus buyers on the constructive developments underway.

A part of PRGO’s self-help technique consists of making its U.S. operation look extra like its enterprise in the UK, the place larger priced variations of the identical molecule are manufactured/offered by PRGO’s current footprint (analogous to a “good/higher/greatest” product providing typically deployed by retailers). In a really asset-efficient method, these newer merchandise may be offered at 2 to 2.5 instances the gross margin of a store-branded drug.

Perrigo can be within the means of eliminating unproductive product traces, as greater than 1,500 inventory maintaining models drive simply 1% of working revenue. The inventory is having fun with appreciable insider shopping for and is attractively priced at simply 12 instances earnings.

Outlook

In the long term, our stock-picking success hinges on avoiding short-term hypothesis and staying true to 10 Ideas of Worth Investing™, which calls for that we stick to well-run corporations possessing robust stability sheets which are additionally buying and selling at engaging valuations. We stay targeted on what we are able to management, together with 1) investing in high quality worth companies that we expect are buying and selling at an acceptable low cost to their intrinsic worth whereas avoiding people who lack valuation help; 2) holding an equal-to-overweight place within the high quality worth class whereas sustaining satisfactory illustration within the deep worth bucket; and three) buying deep worth companies solely after figuring out a self-help catalyst that we consider can unlock worth with execution. Over durations measured in years not quarters, this technique has served us properly.

Colin McWey, Vice President and Portfolio Supervisor

Will Nasgovitz, CEO and Portfolio Supervisor

Troy McGlone, Vice President and Portfolio Supervisor

Fund Returns (3/31/2024)

| Since Inception (%) | 20-12 months (%) | 15-12 months (%) | 10-12 months (%) | 5-12 months (%) | 3-12 months (%) | 1-12 months (%) | YTD* (%) | QTD* (%) | |

|---|---|---|---|---|---|---|---|---|---|

| Mid Cap Worth Investor Class | 9.72 | – | – | – | 11.99 | 8.73 | 16.22 | 5.66 | 5.66 |

| Mid Cap Worth Institutional Class | 10.00 | – | – | – | 12.25 | 9.01 | 16.55 | 5.70 | 5.70 |

| Russell Midcap® Worth | 8.41 | – | – | – | 9.94 | 6.80 | 20.40 | 8.23 | 8.23 |

*Not annualized Supply: FactSet Analysis Programs Inc., Russell®, and Heartland Advisors, Inc. The inception date for the Mid Cap Worth Fund is 10/31/2014 for the investor and institutional class. |

©2024 Heartland Advisors Within the prospectus dated 5/1/2023, the Web Fund Working Bills for the investor and institutional courses of the Mid Cap Worth Fund are 1.10% and 0.85%, respectively. The Advisor has contractually agreed to waive its administration charges and/or reimburse bills of the Fund to make sure that Web Fund Working Bills for the Fund don’t exceed 1.10% of the Fund’s common internet belongings for the investor class shares and 0.85% for the institutional class shares, by no less than 4/5/2025, and topic thereafter to annual reapproval of the settlement by the Board of Administrators. With out such waiver and/or reimbursements, the Gross Fund Working Bills can be 1.16% for the investor class shares and 1.04% for the institutional class shares. Previous efficiency doesn’t assure future outcomes. Efficiency represents previous efficiency; present returns could also be decrease or larger. Efficiency for institutional class shares previous to their preliminary providing is predicated on the efficiency of investor class shares. The funding return and principal worth will fluctuate in order that an investor’s shares, when redeemed, could also be value roughly than the unique value. All returns replicate reinvested dividends and capital positive factors distributions, however don’t replicate the deduction of taxes that an investor would pay on distributions or redemptions. Topic to sure exceptions, shares of a Fund redeemed or exchanged inside 10 days of buy are topic to a 2% redemption payment. Efficiency doesn’t replicate this payment, which if deducted would scale back a person’s return. To acquire efficiency by the newest month finish, name 800-432-7856 or go to Worth Investing Supervisor Worth Mutual Funds | Heartland Advisors. An investor ought to think about the Funds’ funding aims, dangers, and prices and bills fastidiously earlier than investing or sending cash. This and different vital info could also be discovered within the Funds’ prospectus. To acquire a prospectus, please name 800-432-7856 or go to Worth Investing Supervisor Worth Mutual Funds | Heartland Advisors. Please learn the prospectus fastidiously earlier than investing. As of 9/30/2023, First American Monetary (FAF), NOV Inc. (NOV), Spectrum Manufacturers Holdings (SPB), represented 2.51%, 4.86%, and 1.59% of the Mid Cap Worth Fund’s internet belongings, respectively. Statements relating to securities are usually not suggestions to purchase or promote. Portfolio holdings are topic to vary. Present and future portfolio holdings are topic to danger. The Mid Cap Worth Fund invests in a smaller variety of shares (usually 40 to 60) than the common mutual fund. The efficiency of those holdings usually will improve the volatility of the Fund’s returns. The Fund additionally invests in mid–sized corporations on a price foundation. Mid-sized securities usually are extra unstable and fewer liquid than these of bigger corporations. Worth investments are topic to the chance that their intrinsic worth is probably not acknowledged by the broad market. The Mid Cap Worth Fund seeks long-term capital appreciation and modest present earnings. The above people are registered representatives of ALPS Distributors, Inc. The Heartland Funds are distributed by ALPS Distributors, Inc. The statements and opinions expressed on this article are these of the presenter(s). Any dialogue of investments and funding methods represents the presenters’ views as of the date created and are topic to vary with out discover. The opinions expressed are for common info solely and are usually not meant to offer particular recommendation or suggestions for any particular person. The precise securities mentioned, that are meant for instance the advisor’s funding type, don’t characterize all the securities bought, offered, or beneficial by the advisor for shopper accounts, and the reader mustn’t assume that an funding in these securities was or can be worthwhile sooner or later. Sure safety valuations and ahead estimates are based mostly on Heartland Advisors’ calculations. Any forecasts might not show to be true. Financial predictions are based mostly on estimates and are topic to vary. There is no such thing as a assure {that a} specific funding technique can be profitable. Sector and Business classifications are sourced from GICS®.The International Business Classification Customary (GICS®) is the unique mental property of MSCI Inc. (MSCI) and S&P International Market Intelligence (“S&P”). Neither MSCI, S&P, their associates, nor any of their third social gathering suppliers (“GICS Events”) makes any representations or warranties, categorical or implied, with respect to GICS or the outcomes to be obtained by the use thereof, and expressly disclaim all warranties, together with warranties of accuracy, completeness, merchantability and health for a specific objective. The GICS Events shall not have any legal responsibility for any direct, oblique, particular, punitive, consequential or some other damages (together with misplaced earnings) even when notified of such damages. Heartland Advisors defines market cap ranges by the next indices: micro-cap by the Russell Microcap®, small-cap by the Russell 2000®, mid-cap by the Russell Midcap®, large-cap by the Russell Prime 200®. Due to ongoing market volatility, efficiency could also be topic to substantial short-term modifications. Dividends are usually not assured and an organization’s future skill to pay dividends could also be restricted. An organization at the moment paying dividends might stop paying dividends at any time. There is no such thing as a assurance that dividend-paying shares will mitigate volatility. CFA® is a registered trademark owned by the CFA Institute. Russell Funding Group is the supply and proprietor of the logos, service marks and copyrights associated to the Russell Indices. Russell® is a trademark of the Frank Russell Funding Group. Knowledge sourced from FactSet: Copyright 2024 FactSet Analysis Programs Inc., FactSet Fundamentals. All rights reserved. Heartland’s investing glossary gives definitions for a number of phrases used on this web page. |

Unique Put up

Editor’s Notice: The abstract bullets for this text had been chosen by In search of Alpha editors.

Editor’s Notice: This text discusses a number of securities that don’t commerce on a significant U.S. trade. Please pay attention to the dangers related to these shares.

{kind=link}